Lately everyone has been sharing their thoughts on the yield curve with me. Unsolicited. PMs, academics, floor traders -even some of my nefarious journalist contacts.

The general breakdown of these opinions seems to suggest that the more sophisticated your understanding of finance or impressive your credentials, the more likely you are to arrive at a thesis (with complex academic underpinnings naturally) that could support a sustained period at a range close to present levels. Mere mortals tend to expect the curve to moderate sooner and faster, and tend to expect absolute yield to rise more significantly.

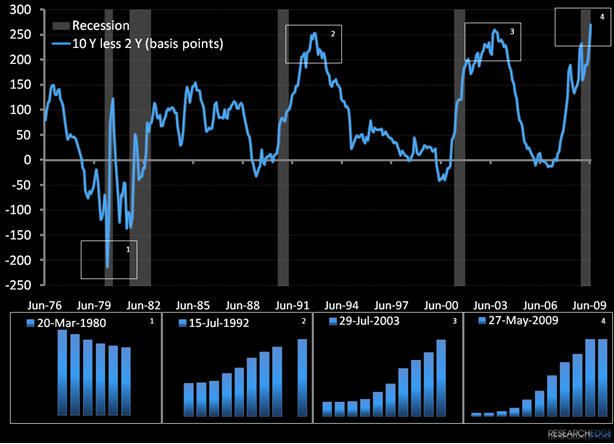

As Keith noted in his morning note today, the Treasury Department sponsored limbo contest on the short end of the curve has literally left depositors bending over backwards to help fatten margins for lending institutions with the spread between the 2 year and the 10 year above 270 basis points the curve is at its steepest point in living memory. I drew the chart below to illustrate the current spread in context. The outlying points since 1976 focused on are the spikes in 1992 and 2003 as the flow of cheap money that Chairman Greenspan let loose to combat recession drove spreads north of 250 basis points; while the monster backwardation in early 1980 marks the height of Paul Volcker's assault on double digit inflation.

The obvious initial conclusion that anyone would draw from this picture visually is that mean reversion should have a moderating impact on the slope of the curve. Additionally, any casual observer could reasonably surmise that with nowhere for short term yields to go but up and with the debt to GDP ratio of the US balance sheet continuing to balloon, the fundamental catalyst for this reversion is both clear and present. The spread between short term treasuries and the target rate has diverged for sustained periods in the past (as well as jumping wildly in the volatile 1982-83 market) so indications from the Fed that rate policy will not change in the near term do not negate these presumptions.

As always, the moment of confirmation for the peak will arrive well after it has passed. Until then you can continue to feel free to share your view with me.

Andrew Barber

Director