TODAY’S S&P 500 SET-UP – September 5, 2013

As we look at today's setup for the S&P 500, the range is 25 points or 0.61% downside to 1643 and 0.90% upside to 1668.

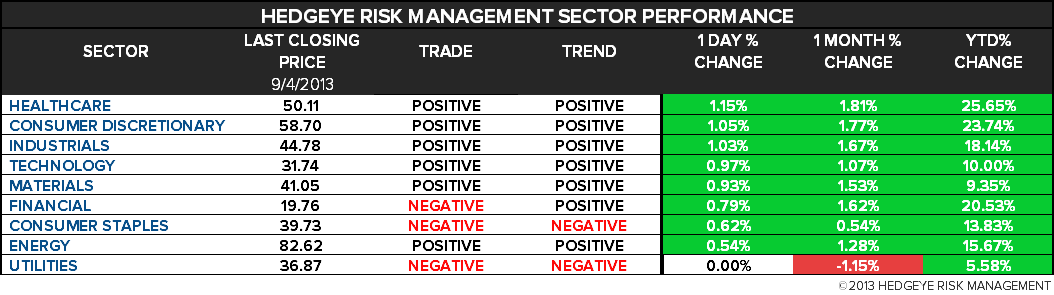

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.45 from 2.43

- VIX closed at 15.88 1 day percent change of -4.39%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: Bank of England seen maintaining bank rate of 0.5%

- 7:30am: Challenger Job Cuts Y/y, Aug. (prior 2.3%)

- 7:30am: RBC Consumer Outlook Index, Sept. (prior 49.4)

- 7:45am: ECB seen maintaining benchmark rates at 0.5%

- 8:15am: ADP Employment Change, Aug., est. 180k (prior 200k)

- 8:30am: ECB’s Draghi holds news conference

- 8:30am: Nonfarm Productivity, 2Q final, est. 1.6% (pr 0.9%)

- 8:30am: Init Jobless Claims, Aug. 31, est. 330k (pr 331k)

- 9am: Fed’s Kocherlakota speaks in La Crosse, Wis.

- 9:45am: Bloomberg Consumer Comfort, Sept. 1

- 10am: Factory Orders, July, est. -3.4% (prior 1.5%)

- 10am: ISM Non-Manufacturing, Aug., est. 55 (prior 56)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: DoE energy inventories

- 11am: U.S. to announce plans for sale of 3Y notes, 10Y notes, 30Y bonds

- 1:30pm: Fed’s Fisher speaks in economy in Dallas

GOVERNMENT:

- G-20 Leaders Summit begins in St. Petersburg, Russia

- 2pm: Members of Congress receive classfied briefing on Syria

WHAT TO WATCH:

- Microsoft wins jury trial over Google patent licensing tactics

- Aug. U.S. Retail Sales Seen Hurt by Delayed School Shopping

- SKF to buy Kaydon for $1.25b to expand U.S. business

- Mail.ru sells rest of its Facebook stake for $525m

- Sprint raises $6.5b in biggest junk sale since 2008

- Otsuka Holdings offers to buy Astex for up to $886m

- Fed’s Kocherlakota says U.S. economy needs more accommodation

- LinkedIn boosts offering to $1.2b after share rally

- Liberty Media’s Malone said to plan for succession: NY Post

- G-20 draft calls for more job training, infrastructure spending

- Dominion bids $1.6m for offshore Virginia wind project

- Nasdaq, SIP outline proposed actions after Aug. 22 glitch

- Kuroda says Japan can roll out stimulus if needed after tax rise

- Samsung $299 Galaxy Gear tests consumer smartwatch demand

- Focus Media owners seek up to $500m dividend recap: Reuters

EARNINGS:

- Conn’s (CONN) 7am, $0.60

- Cooper Cos (COO) 4:01pm, $1.72

- Finisar (FNSR) 4pm, $0.31

- Infoblox (BLOX) 4:05pm, $0.09

- Jos A Bank Clothiers (JOSB) 6am, $0.52

- Quiksilver (ZQK) 4pm, $0.04

- Smith & Wesson (SWHC) 4:05pm, $0.36

- VeriFone Systems (PAY) 4:01pm, $0.20

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Rises From One-Week Low as Senate Panel Backs Syria Strike

- Steel Rallying With Chinese Builders Beating Mills: Commodities

- Tin Heads for Four-Month High on Concern About Limited Supply

- Sugar Surplus Shrinks on Quickening Demand in China to Indonesia

- Rubber Advances on Thai Farmer Protests, U.S. Car Sales Gains

- Rebar Futures Drop to Lowest in a Month as Premium Lures Sellers

- Palm Oil Climbs as Crude-Price Gain Increases Appeal of Biofuel

- Gold Rises as Investors Seek Haven Amid Syrian Strike Debate

- Gold Imports to China From Hong Kong Climb on Physical Demand

- Libya Propels Sweet African Oil Toward 2011 High: Energy Markets

- Oil Puts at 18-Month Low as U.S. Prepares Syria Strike: Options

- Iron Ore Supply of Up to 830 Million Tons May Be Added by 2020

- Asia Fuel Oil Viscosity Spread at Two-Month High: Oil Products

- World Food Prices Fell Fourth Month in August on Cheaper Grains

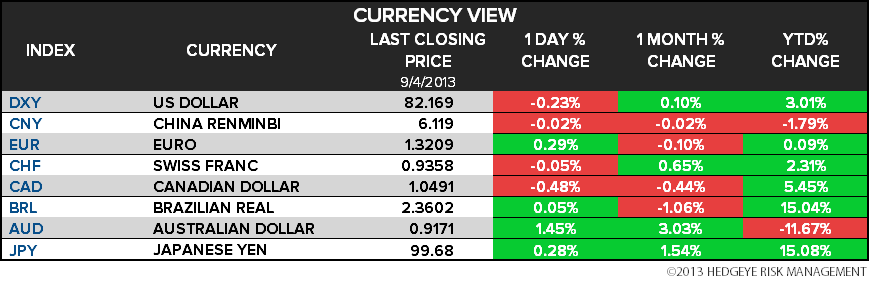

CURRENCIES

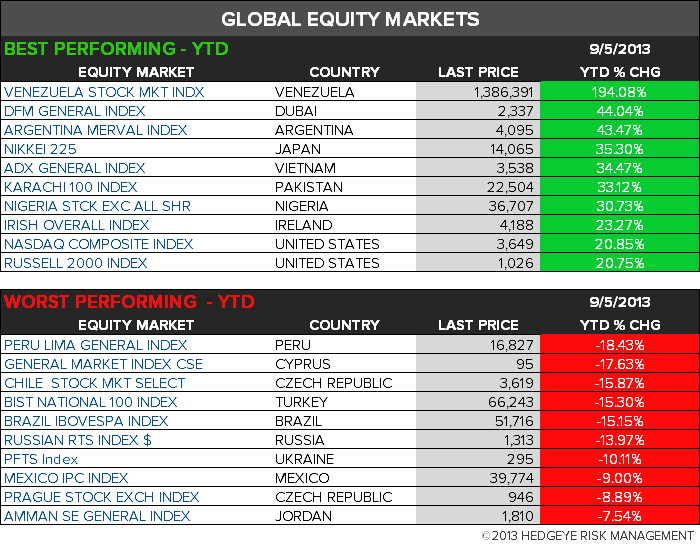

GLOBAL PERFORMANCE

EUROPEAN MARKETS

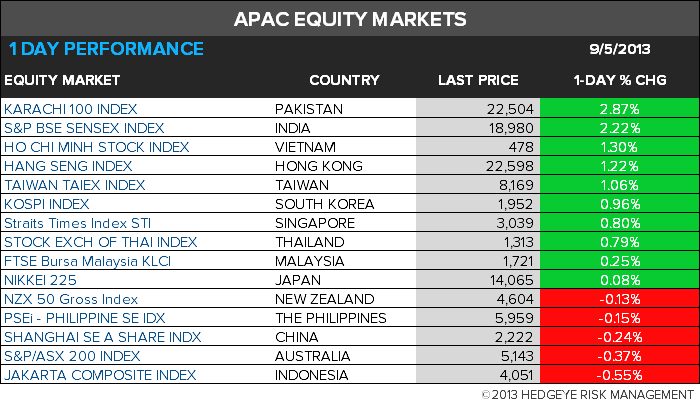

ASIAN MARKETS

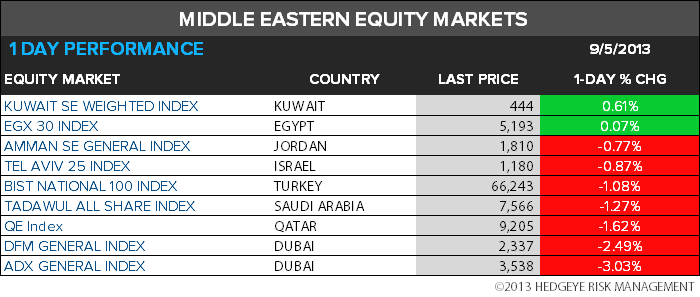

MIDDLE EAST

The Hedgeye Macro Team