After a long steep climb, the MPEL engine may be slowing down.

We're still positive on Macau so it’s difficult to be negative on MPEL. However, MPEL’s recent share losses in the Junket segment are a little disconcerting and could continue. Moreover, MPEL’s Mass share could be at risk as Sands Cotai Central begins its push into Premium Mass next year. So while not negative, it’s probably safe to say we've pushed MPEL to the bottom half of attractive Macau operators, behind LVS, MGM, and Galaxy.

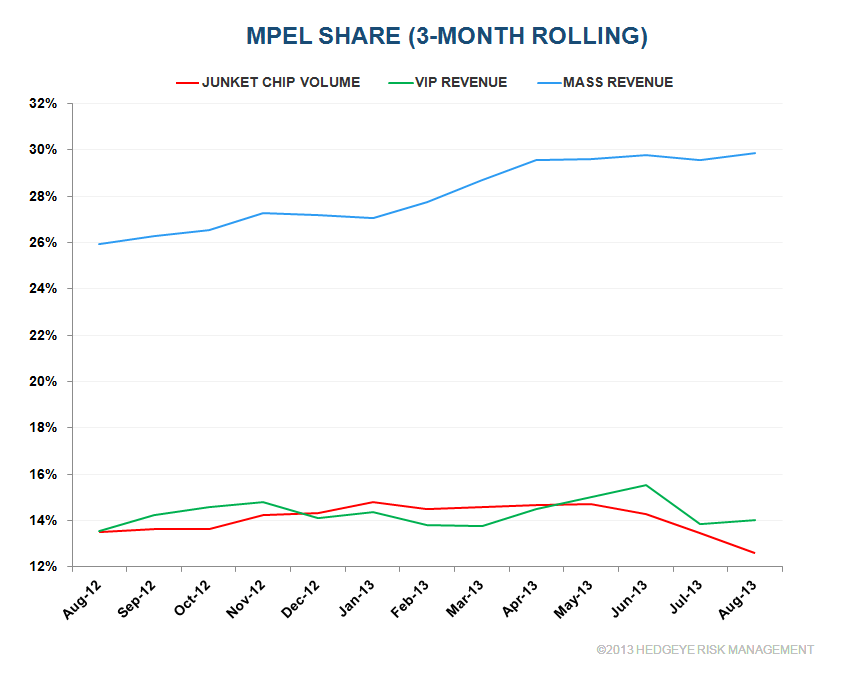

As seen in the following chart, MPEL’s 3 month average Rolling Chip share has fallen almost 200bps from its May high. We do think it is possible that some of the drop could be conversion of Junket players to Direct VIP and Premium Mass. Indeed, MPEL’s Mass share has held up well and VIP Revenue share (which includes Direct Play) has dropped 160bps - less than its Junket volume decline.

However, our research indicates that competitive forces are probably playing a bigger role. From the next chart, it appears that Galaxy, SJM and Wynn have gained the most share since May. Galaxy recently moved 12 Junket tables from the Grand Waldo to the much more alluring Galaxy Macau. We’re pretty sure Galaxy was able to attract at least one new junket. Galaxy may also be offering a more attractive junket credit package. We know SJM added a few new junkets this year as did Wynn.

In the future, LVS could be the market share gainer MPEL should fear, not only in Premium Mass but also in VIP. With conservative COO David Sisk out of the picture, look for more aggression on the Junket side in terms of credit and commission advancement packages. We already know that Sands Cotai Central will be opening new Premium Mass facilities which should grow the market but also take share from the Cotai Premium Mass leader, MPEL’s City of Dreams.

If Macau keeps growing in the mid to high teens rate, all the Macau stocks should do well. Our view is that after a long and strong run, a few fundamental risks could derail MPEL’s momentum. Other Macau stocks such as LVS look more protected, and thus attractive, at this point.