This note was originally published at 8am on August 21, 2013 for Hedgeye subscribers.

“Before I went to jail, I was active in politics as a member of South Africa’s leading organization – and I was generally busy from 7 A.M. to midnight. I never had time to sit and think.”

-Nelson Mandela

Former South African Prime Minister Nelson Mandela had more time to sit and think then most of us will ever get. He served 27 years in prison, first on Robben Island, and later in Pollsmoor Prison and Victor Verster Prison after being convicted of sabotage and conspiracy to overthrow the South African government.

I’ve recently been reading Mandela’s biography and after reading about how he spent his nights in a damp concrete cell of 8 feet by 7 feet and his days breaking rocks into gravel, I’m not sure I would wish this type of “thinking time” on my worst enemy. But, thinking time is important for all us, and I will be taking some thinking time myself as my first two week vacation of the last decade looms in the next couple of weeks.

In a book we have cited many times, “Thinking, Fast and Slow”, Nobel laureate Daniel Kahneman describes two modes of thought. The first is System 1, which is fast, instinctive, and emotional. The second is System 2 and is slower, more deliberative, and more logical. The main purpose of his book is to describe the dichotomy between these two kinds of thought.

To illustrate how the two different systems work, answer this before you go on:

A hockey stick and puck cost $1.10 together.

If the stick costs $1.00 more than the puck, what does the puck cost?

If you are like most people, even the highly numerical, it is likely that the price of $0.10 popped into your head. The correct answer of course is that stick cost $1.05 and the puck cost $0.05, so thus the stick cost $1.00 more than the puck.

In a day and age when we are inundated with more stimuli and decision making opportunities than ever before, it is becoming even more critical to take some Thinking Time to maintain the deep logic of System 2. The fact of the matter is, the self-induced dopamine loops of constant texting, tweeting, googling and emailing diminish our performance. (Well, at least that’s how I’m justifying my vacation to my colleagues :) )

Back to the global macro grind . . .

I’m going to take this concept of short term versus long term thinking and apply it to the current battleground stock of the day, J.C. Penney (JCP). Recently Pershing Square’s Bill Ackman all but admitted defeated in his attempt to turn around the retailer as he resigned from the board of JCP and received permission for Pershing Square to sell the more than 15% of the stock it owns. This is short term capitulation.

At the same time, a number of other hedge funds have been taking sizeable positions at the stock has declined, including Kyle Bass, Soros Fund Management and Perry Capital. Bass, as reported by Bloomberg is actually buying the debt. These are long term investment positions.

Before I dig into the stock a little more, I wanted to let you know that our Retail Sectorhead Brian McGough will be doing a deep dive on the stock on August 27th at 1pm. (Ping sales@hedgeye.com for details.) As many of you know, Brian was in early in recommending investors short and/or sell the stock when Ackman got involved. He then tried to call the turn around and added the stock to our Best Ideas list, but ultimately removed the name at about the current price level on March 14th as there was little evidence of a turnaround and his view was that JCP was dead money (which it was).

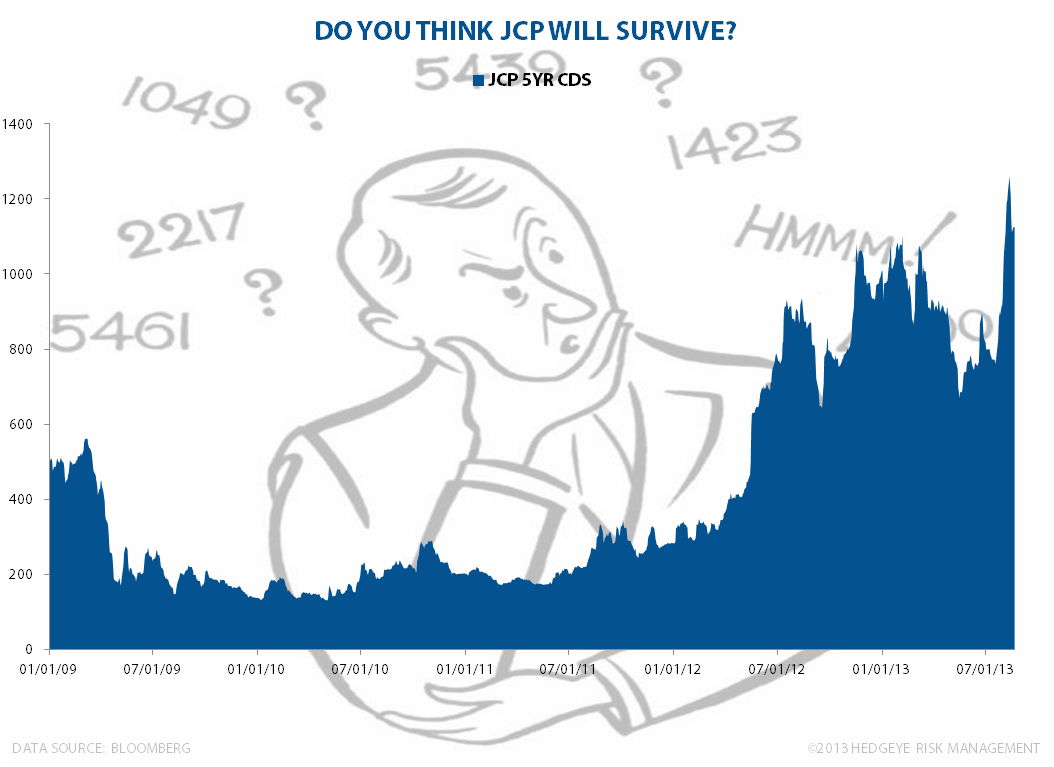

The Chart of the Day today is a chart of JCP credit default swaps that shows that while a bankruptcy isn’t a foregone conclusion, there is certainly risk as investors are willing to pay a meaningful premium to insure JCP debt. Interestingly, while JCP debt has declined versus its peer group over the last couple years, it is not yet at extreme levels.

As examples, per Bloomberg and Forbes, the J.C. Penney 5.65% notes due 2020, yesterday traded up two points, at 73.5. While the long-tenor 6.375% bonds due 2036 traded up half a point, at 69.5, for a net gain of 3.5 points week over week. In the loan market, J.C. Penney’s covenant-lite term loan due 2018 (L+500, 1% LIBOR floor) were slightly firmer, recently quoted at 96.5/97. As a reference, the $2.25 billion loan was issued at 99.5 in May.

As McGough noted yesterday, “the fact that JCP hit the liquidity levels it guided toward at quarter-end is notable. Add on the fact that capex next year is guided to be down as far as $300mm, and the liquidity picture looks less pressured. We’d argue that these two factors are the sole reasons why the stock was up today. Why?

Let’s stress test the model. We quarter-ized our model for the next three years using the following assumptions a) JCP reaches 2012 sales per square foot levels in 2015, with a gradual comp lift throughout, b) the company generates 37% gross margins – a level we think there is no structural reason it can’t hit again relatively quickly (we know we'll get pushback on that -- but will happily entertain the debate), EBIT margins don’t turn positive until 2016, c) capex increases by $50mm each year, d) working capital patterns are similar to what we saw before 2012.

In tracking the cumulative liquidity for the next three years, there are two periods where it definitely gets dicey for JCP (the worst is 3Q15 -- in two years) – close enough such that it will likely need to find some asset sales that are not already tied to the GS secured debt offering. But even without assuming a miraculous turn at the company, we don’t get to a big liquidity event.”

So, if there is no major liquidity event for the next three years, there is decent runway for the company to turnaround and the shorter term debt, at the very least, looks reasonably safe. But what do you think?

Next Thursday at 1pm, we’ll introduce some new information and dig into more of our thoughts. If the turnaround actually happens, based on historical margin levels, JCP equity is a really cheap option at these levels.

Our immediate-term Risk Ranges are now:

UST10yr 2.71-2.94%

SPX 1642-1674

Nikkei 13,301-13956

USD 80.80-81.94

Brent 108.78-110.32

Gold 1324-1392

Keep your head up and stick on the ice,

Daryl G. Jones

Thinker-in-Chief