Friday's Jobs number looms as delinquency data shows that the pain continues

As it stands today, we have zero exposure to US equities in our asset allocation model. In particular we have aggressively sold off our exposure to consumer discretionary in the vortex of the recent MEGA squeeze.

After a good, solid start to June and with the S&P at 930, we have been harping on the theme that "less bad" is different from "good." We are data driven and, as such, need to see the "good" in the dominant story to cement a bullish conviction. We are not seeing "good" yet.

Today's, payroll report estimates that another 532,000 workers lost jobs in May. More than consensus thinking! This continues to cause trouble for the consumer lending markets, from mortgages to credit cards and everything in between.

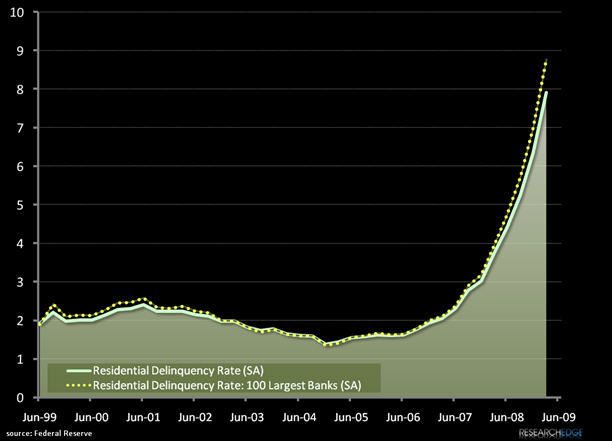

About 12% of mortgage loans were delinquent or in the foreclosure process during 1Q09, according to data released by MBA last week, while Federal Reserve estimates put the number at almost 9% on a broader measure of residential real estate loans. These levels represent the highest recorded, exceeding the levels reached in the early 1970's and follow broad trends in consumer credit, with rising delinquencies in categories like credit cards and car loans showing no clear signs of abating.

The majority of the foreclosure problems remain concentrated in four states: California, Nevada, Arizona and Florida, where home prices spiked the highest and are now in freefall. According to MBA, these four states alone accounted for 56% of the increase in foreclosure starts. Anecdotal reports from brokers in those markets report that sales trends appear to have bottomed but are not getting measurably better.

Clearly the housing picture is better than it was in January, but with seasonal inflections, the Obama taxpayer credit for first time home buyers and historically low interest rates any resilience here should be no surprise.

Our zero exposure to US equities is a big statement! Friday's employment report should be less constructive than the last two - which were bullish catalysts for us as we looked for signals that the rate of job losses was compressing. Now that our 1H thesis has become consensus and the seeds of optimism have begun to nurture loftier expectations, a signal of anything less than a strong signal of leveling in payroll declines seems poised to strike fear into the hearts of hopeful bulls.

Howard Penney

Managing Director

Andrew Barber

Director