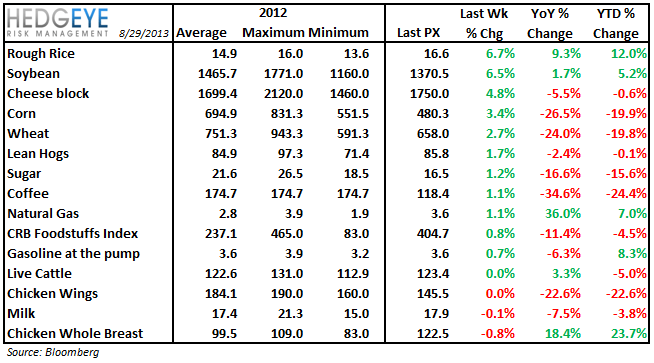

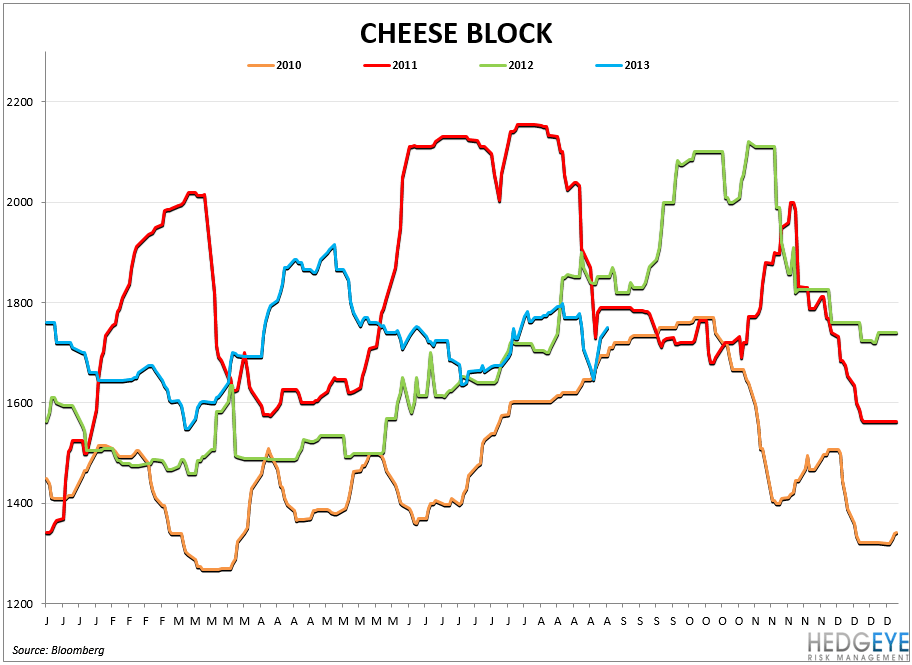

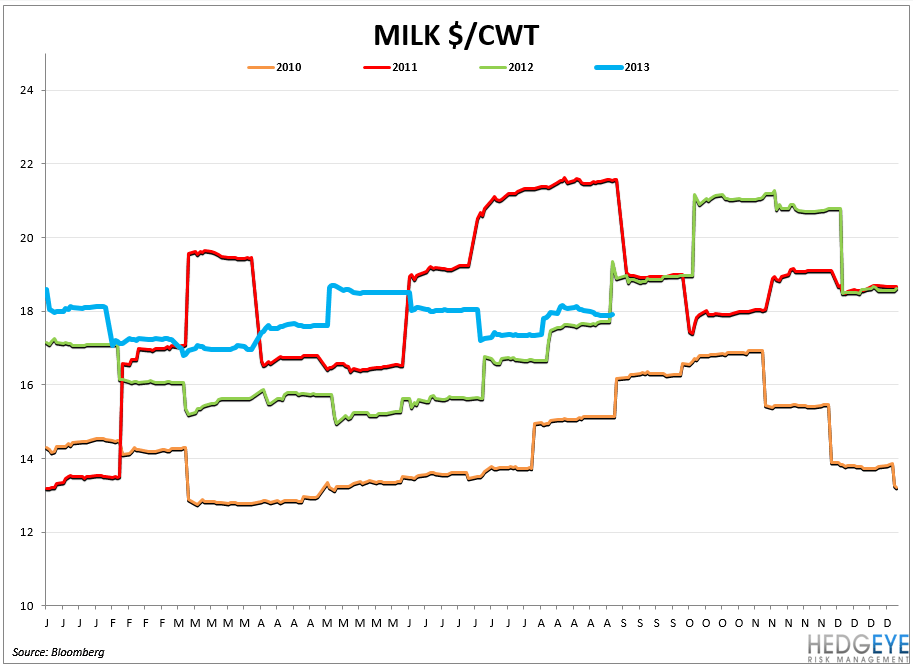

The charts below illustrate some of the important commodity trends for the restaurant industry.

Notable Trends:

- Coffee prices have been trending down YTD and should continue to be a tailwind for SBUX, DNKN, GMCR, THI, KKD and other coffee retailers for the remainder of the year.

- Gasoline prices are trending up YTD and we would caution that any sustained increase could have a significant impact on discretionary spending.

- Chicken wings are down -22.6% YTD and we expect this trend to reverse for the remainder of the year as football season approaches and MCD prepares to rollout Mighty Wings nationwide on September 9.

- Corn and wheat prices both moved higher this week, but remain down -26.5% and -24.0% YoY, respectively, and barring a major reversal, should continue to provide retailers, restaurants and consumers with lower food costs than a year ago.

Howard Penney

Managing Director