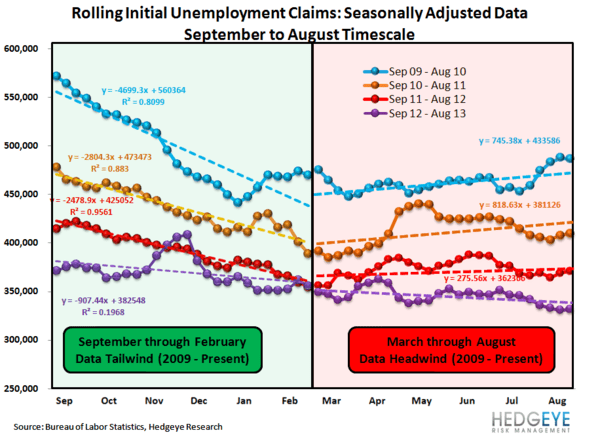

Positive labor market trends continue to defy both the fiscal drag and negative seasonal headwind which is nearing (what should be) peak negative impact into September.

Non-seasonally adjusted claims printed another new cycle low, and lowest print since September 2007, at 277K. The YoY rate of improvement accelerated 110bps sequentially to -11.2% while the 4-wk rolling average of claims registered its fastest rate of improvement YTD at -10.6%. Headline, seasonally adjusted claims declined 6K WoW to 331K with the 4-wk rolling average increasing a modest 0.75K.

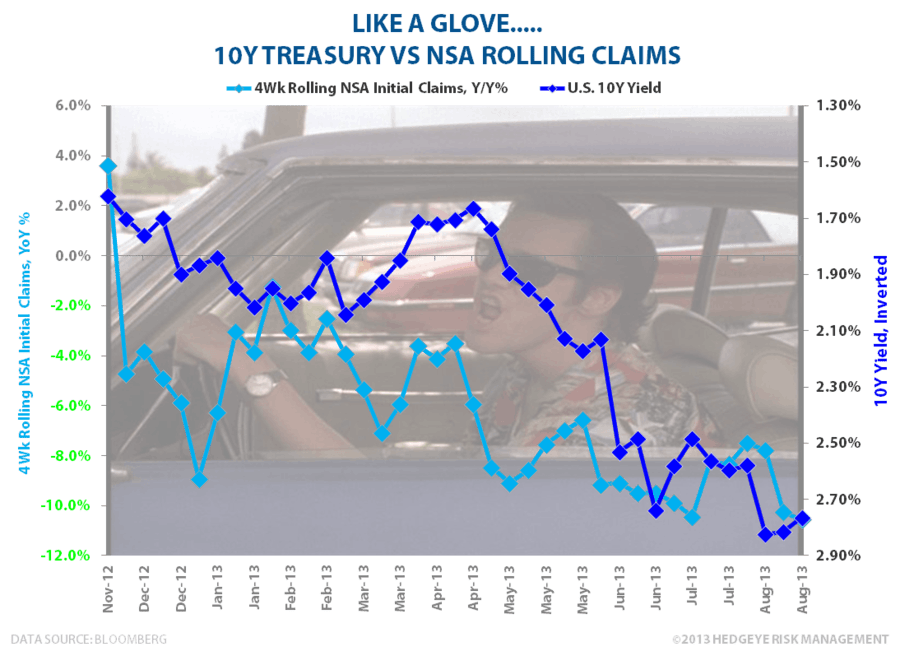

The relationship between NSA claims and 10Y yields since the market/growth inflection in November 2012 has been stark as #RatesRising has continued to reflect the underlying strength and positive growth implications embedded in a strengthening labor market.

As Josh Steiner and our Financials team highlighted earlier today:

The bottom line takeaway here is that the labor market is, in fact, stronger than most think and financials that are positively levered to ongoing improvement in labor conditions should continue to outperform. Moreover, given the growing shadow of uncertainty painting the recent tape, we'd look to this data series more than any other as a green light for buying weakness.

Meanwhile, the 1st revision to GDP was positive but largely optical as the aggregate upward revision stemmed principally from a positive revision to net exports. Consumption was essentially unchanged while the modest, positive revision to investment and modest, negative revision to government expenditure was largely a wash. A summary review of the preliminary 2Q13 estimate along with the impact of the 1st revision vs. the advanced estimate below.

Source: Hedgeye Financials

Christian B. Drake

Senior Analyst