“What they lacked was a science of disorder and randomness.”

-George Gilder

Gilder could have been writing about adults making life decisions inasmuch as he was alluding to both Keynesian and Hayekian policy makers who still don’t get the core chaos theory concept of non-linearity. If you don’t know what I am talking about, have kids.

Both life and market risks are grounded in uncertainty. You can take whatever precautions you want; you can be as proactively prepared as you think you can be – but it’s always the surprise of new information that drives decision making.

You cannot learn how to embrace uncertainty in a textbook. You have to learn this game by playing it. Since disorder and randomness typify markets, your risk management process should attempt to absorb that dynamism.

Back to the Global Macro Grind…

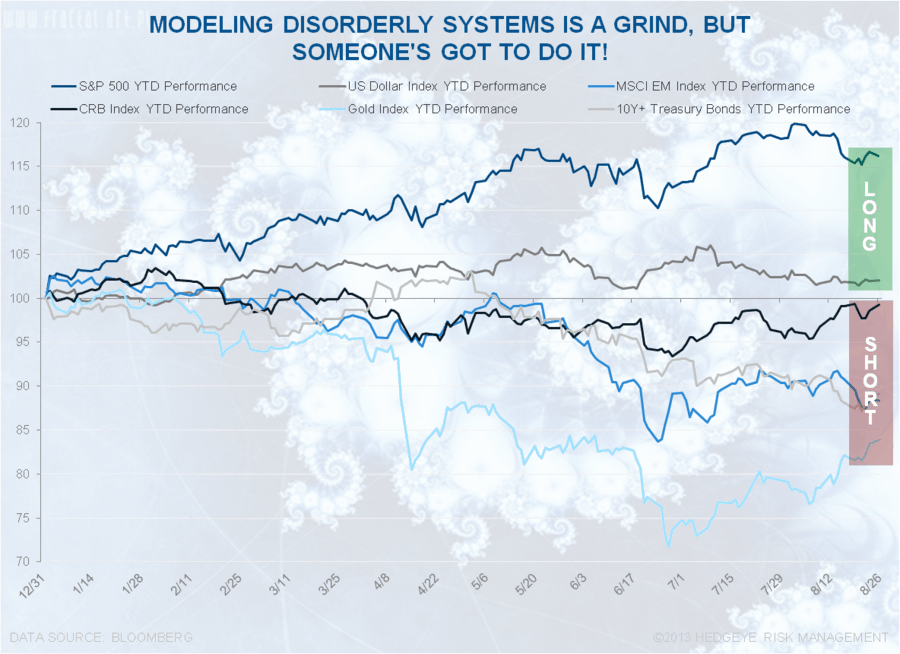

Three big macro things have really changed in the last 3 months:

- Bond Yields in the USA, Germany, and the UK have been rising alongside their respective stock markets #surprise

- Growth Stocks (Low Dividend Yield, High EPS Growth, High Short Interest) have been crushing Slow-Growth Stocks

- Asian Emerging Market stocks have been dramatically underperforming US Growth Stocks

That sounds a little disorderly, no?

If you are bullish on “growth” doesn’t your local pie chart “diversification” manufacturer have you buying “Emerging Markets”? Or are they re-positioning that bad asset allocation decision to you now as something that looks “cheap.” #ThesisDrift

In Hedgeye-Jedi speak, “cheap” gets cheaper when:

A) Country Inflation (or costs in the case of a company) Accelerates

B) Real (inflation adjusted) Growth Slows

Back-test it with Apple (AAPL) and you’ll get my point. It doesn’t matter how “good” a company is if it’s about to see:

A) Revenue Growth Slow (versus peak)

B) Margins Compress (versus peak)

When you get A + B, you get multiple compression.

Conversely, in our proprietary GIP Model (Growth, Inflation, Policy), when a country:

A) Sees Growth go from slowing to stabilizing to accelerating … and

B) Is the recipient of inflation slowing via currency appreciation…

You get equity market multiple expansion. Look at the chart of any raging “growth” stock that is USA centric (SBUX, TSLA, DDD, NFLX, OPEN, SODA, etc.) and you’ll get what I mean.

Simple, right? Even a hockey player can do it.

Yes, in hindsight, most things macro are easier to see looking backwards. It’s in observing the chaotic system of colliding global macro market trends (where Growth and Inflation patterns develop) that you get an edge. It’s a grind.

Let’s go back to explaining why the aforementioned point #3 (#AsianContagion) has come to be. What’s happening this morning was as obvious in June as it is today:

- Indonesia’s Rupiah continues to crash; down big this morning -4.3% (for a currency, that is a lot!)

- India’s Rupee continues to crash as well, down another -1.9% this morning

As a country’s currency gets crushed, #InflationAccelerates and #GrowthSlows – then you get:

- Indonesia’s stock market down another -4% overnight (down -15% for the month-to-date)

- India’s stocks market down another -3.1% overnight (-11.5% since July 23rd)

Sure, it may seem disorderly and random that Asian “growth” markets can dislocate from US domestic growth stocks. It may appear random to the Macro Tourist who doesn’t stare at the matrix of currency and correlation risk like we do all day too.

But the other big point about disorder and randomness embedded in chaos theory is that there is a deep simplicity to it all, in hindsight.

Our immediate-term Risk Ranges are now as follows (we have 12 Big Macro risk ranges in our Daily Trading Range product now too):

UST 10yr Yield 2.71-2.93%

SPX 1

EEM 32.07-38.99

VIX 13.03-15.44

USD 80.93-81.80

Copper 3.30-3.39

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer