Starbucks (SBUX)

Starbucks has been on the Hedgeye Real Time Alerts list since 4/21/09, when we added it as a LONG.

SBUX continues to be the best run company that we follow and the long-term TAIL seems unlimited. Impressive FY3Q13 results only enhance this view. Despite the stock trading at the high end of its historical consensus forward earnings and cash flow multiples, we believe there is more upside in store. The three bullish factors we remain focused on include rapid unit growth in China, expansion into new segments of the global food and beverage industry and a commodity tailwind that we anticipate will continue well into FY15.

At 15.1x EV/EBITDA, SBUX is trading significantly above its QSR peer group at 12.4x EV/EBITDA, but we believe this premium is warranted. Sentiment on the street is high, and this, along with the development of La Boulange are two of our main concerns. While we can argue that the street is not bullish enough on SBUX, we cannot brand La Boulange a success just yet.

The Cheesecake Factory (CAKE)

We added CAKE to the Hedgeye Best Ideas list on 2/11/13 as a LONG.

Despite reporting disappointing 2Q13 results, the underlying fundamentals of the company remain strong. We expect 3Q13 to be a challenging quarter for all casual dining companies and CAKE is no exception, as the company faces slowing industry trends and a tough comp. However, we believe sales will rebound strongly in 4Q13 and carry on into 2014.

At 8.7x EV/EBITA, CAKE is valued in line with its Casual Dining peer group trading at an 8.8x multiple. While short interest is currently 11.09% of the float, we believe the international story is underappreciated by the street. International locations have exceeded expectations and management plans to open another three Middle East stores this year. For each Middle Eastern restaurant that is open for a full-year, we expect $0.01 in incremental annual earnings per share.

Panera Bread (PNRA)

We added PNRA to the Hedgeye Best Ideas list on 4/5/13 as a SHORT.

Reflected in 2Q13 results, PNRA is facing a bevy of issues. The company’s position as a healthy QSR option that is relatively free of competitors is gradually changing. An increasing number of Casual Dining chains are now offering lower price points and other QSR chains are upgrading their menus. These menu upgrades include items that are being competitively marketed as healthy eating options and are cheaper than PNRA’s core offering. This means one thing for PNRA: more competition.

But this isn’t the only issue that PNRA is facing. The company has admitted to having numerous and varying operational issues, ranging from a lack of kitchen equipment to a lack of seating. Capacity issues have dampened lunch time transactions and management has struggled to drive peak hour throughput. Therefore, we believe the labor line favorability the company has seen lately will wane, as PNRA will have to invest increased labor in some of its cafes in 2H13.

The aforementioned issues are manifesting themselves in the components of comparable sales growth as PNRA traffic trends have shown weakness lately. At 9.8x EV/EBITDA, the stock currently trades at a discount to its QSR peer group at a 12.4x EV/EBITDA. We believe this discount is justified and expect PNRA to have another rough outing in 3Q13.

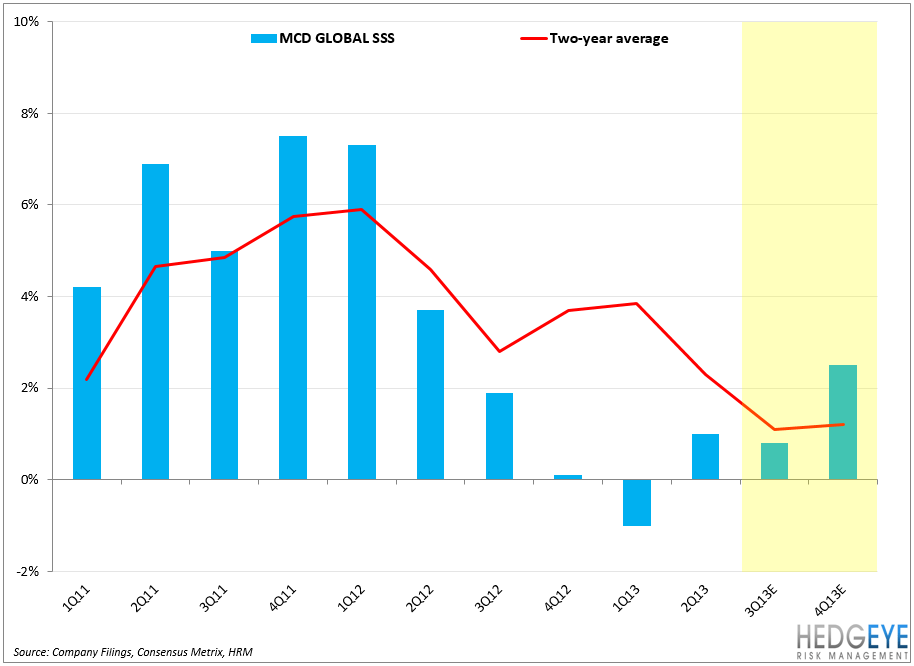

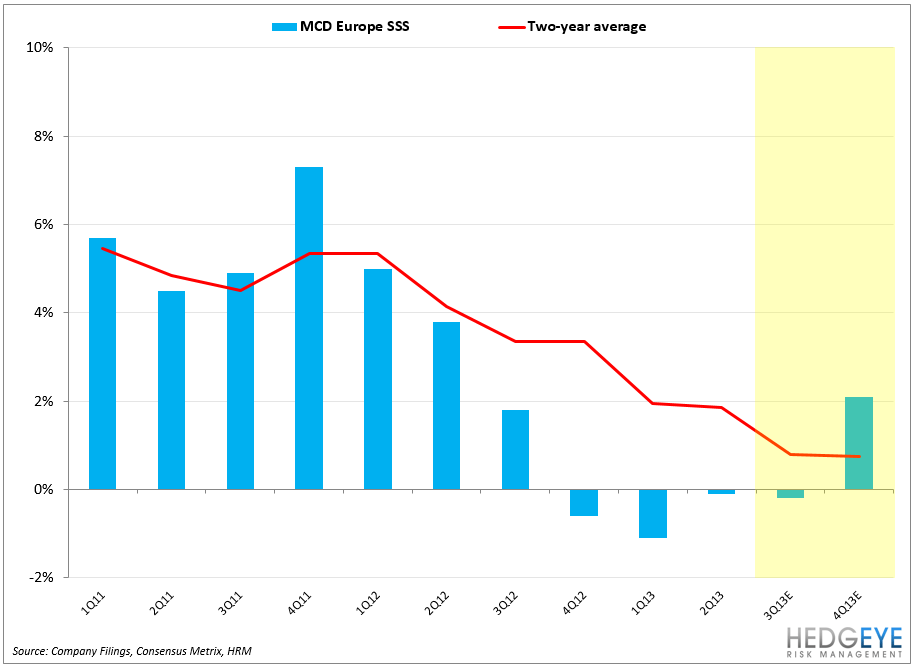

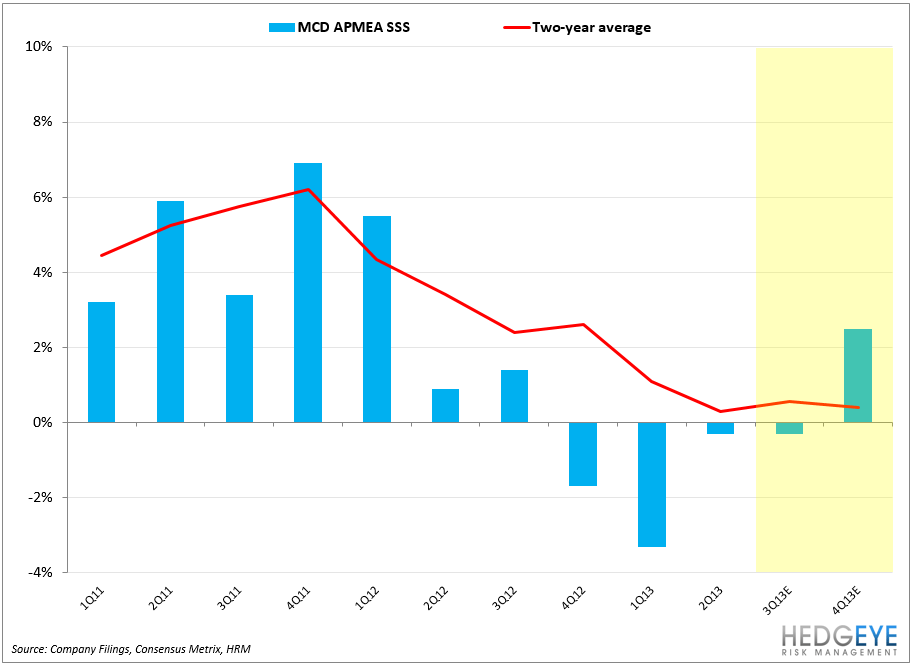

McDonald’s (MCD)

We added MCD to the Hedgeye Best Ideas list on 4.25 as a SHORT.

July sales numbers recently reported by MCD confirm that the company continues to struggles amidst a difficult macro and increasingly difficult competitive environment. The company has a lot of work to do in order to improve its operational performance and we fail to see any indication that this will transpire soon. We previously laid out our thoughts on the path management must take in order to generate sustainable revenue and operating growth in our note titled, “MCD – Difficult Decisions Looming?”

Management’s Plan to Win strategy has proven stale, as new products are not working and operational throughput issues persist. We believe MCD’s attempts to diversify away from core competencies have, to some degree, brought about these issues. In addition to operational problems, the company faces three near-term issues: flat-to-declining markets, a lack of pricing flexibility and increasing competition. To touch on the latter, companies like Wendy’s, Chipotle and even Taco Bell have been pressuring McDonald’s sales as they have been able to successfully do what McDonald’s has not: appeal to Millenials. As the competitive landscape continues to change, MCD must figure out how to appeal to this cohort.

Short interest is only 0.92% of the float and at 10x EV/EBITDA, MCD is trading significantly below its QSR peer group at 12.4x EV/EBITDA. We believe the aforementioned operational and near-term issues validate this discount.

Howard Penney

Managing Director