TODAY’S S&P 500 SET-UP – August 22, 2013

As we look at today's setup for the S&P 500, the range is 38 points or 0.72% downside to 1631 and 1.59% upside to 1669.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.55 from 2.53

- VIX closed at 15.94 1 day percent change of 6.91%

MACRO DATA POINTS (Bloomberg Estimates):

- Kansas City Fed Jackson Hole Economic Summit, thr. Aug. 24

- 8:30am: Init Jobless Claims, Aug. 17, est. 330k (pr. 320k)

- 8:58am: Markit U.S. PMI Prelim., Aug., est. 54.2 (pr. 53.2)

- 9am: House Price Index M/m, June, est. 0.6% (prior 0.7%)

- 9:45am: Bloomberg Economic Expectations, Aug. (prior -5)

- 10am: Leading Eco. Indicators, July, est. 0.5% (prior 0.0%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Kansas City Fed Manufacturing, Aug., est. 6 (prior 6)

- 11am: Fed to buy $1.25b-$1.75b notes in 2036-2043 sector

- 11am: U.S. to announce sizes of 2Y, 5Y, 7Y notes

- 1pm: U.S. to sell $16b 5Y TIPS in reopening

- 2pm: Fed’s Fisher speaks in Orlando, Fla.

GOVERNMENT:

- President Obama speaks on improving value of higher education for middle class during bus tour through N.Y. and Penn.

- 11am: Airlines for America qtrly briefing on U.S. passenger airlines’ YTD financial, operational results, performance

- 2pm: Chairman of Joint Chiefs of Staff Gen. Martin Dempsey briefs foreign media on U.S. national security strategy

- 4pm: Treasury Sec. Jack Lew speaks to Commonwealth Club of Calif.

WHAT TO WATCH:

- FBI said to hunt for criminal acts in JPMorgan energy inquiry

- Wells Fargo said to eliminate 2,300 mortgage-production jobs

- Microsoft says bribery investigation includes Russia, Pakistan

- EU said to weigh curb on collateral asset reuse in repo trades

- China’s manufacturing gains on stronger domestic demand

- Everbright Securities president Xu quits after trading error

- Yahoo tops Google in U.S. for July web traffic, ComScore says

- Hoover maker aims to turn bankrupt Oreck profitable next year

- Tesla CEO weighs overseas plants for mass-market electric car

- Potash rift seen lasting as Asia sales said to rile Uralkali

- JSW seeks to sell U.S. plant as demand revives

- Euro-area services output grows for first time in 19 months

- GM’s Opel revamps insignia to regain customers

- FHFA should develop policies to govern settlements: report

EARNINGS:

AM EARNS

- Abercrombie & Fitch (ANF) 6:30am, $0.29 - Preview

- Buckle (BKE) 7am, $0.52

- Children’s Place (PLCE) 6:30am, $(0.53)

- Dollar Tree (DLTR) 7:29am, $0.57

- GameStop (GME) 8:30am, $0.04

- Hormel Foods (HRL) 6am, $0.45

- Patterson (PDCO) 7am, $0.48

- Ross Stores (ROST) 8:25am, $0.93

- Sears Holdings (SHLD) 6am, $(1.07)

- Toro (TTC) 8:30am, $0.59

PM EARNS

- Aeropostale (ARO) 4:01pm, $(0.28)

- Aruba Networks (ARUN) 4:03pm, $0.11

- Autodesk (ADSK) 4:01pm, $0.42

- Gap (GPS) 4pm, $0.64

- Marvell Technology (MRVL) 4:03pm, $0.19

- Mentor Graphics (MENT) 4:05pm, $0.17

- Micros Systems (MCRS) 4:02pm, $0.62

- Nordson (NDSN) 4:30pm, $1.05

- Pandora Media (P) 4:02pm, $0.02 - Preview

- Solera Holdings (SLH) 4:07pm, $0.66

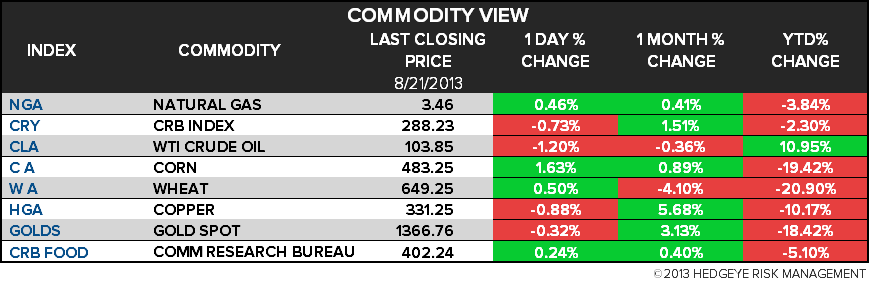

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Rebounds From Two-Week Low on China Manufacturing Growth

- Gold Rout Seen Bottoming by Analysts as China Buys: Commodities

- Russian Urals Set to Lose Iraq-Attack Premium: Energy Markets

- Toyota Said to Raise Steel Prices for Suppliers by 12 Percent

- Gold Rises in London as Bearish Bets Drop Amid Sign of Bottoming

- Corn Declines as U.S. Yields Boost Outlook; Soybeans Retreat

- Rubber Jumps as China’s Manufacturing Improves, Yen Weakens

- Gold’s Luster Burnished by Currency Collapse in Emerging Markets

- Indonesia Cuts Palm Oil Export-Tax to Boost Sales as Prices Drop

- FBI Said to Hunt for Criminal Acts in JPMorgan Energy Probe

- Rebar Falls to Lowest in Two Weeks as Mills Increase Selling

- Commodities May Decline 11% on Fibonacci: Technical Analysis

- Tin Smelters in Indonesia to Start Trading Through Exchanges

- Copper Advances as Manufacturing Unexpectedly Expands in China

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team