Investment Company Institute Mutual Fund Data and ETF Money Flow:

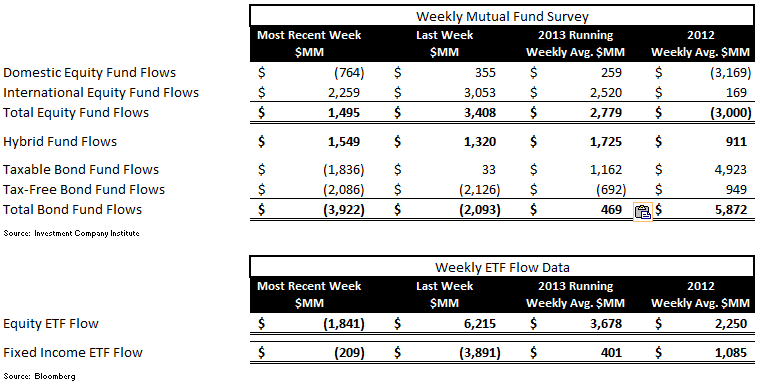

Equity Mutual Fund inflow slowed to $1.4 billion for the week ending August 14th, down from a $3.4 billion inflow the week prior but remained positive

Fixed Income Fund flows accelerated to a bigger draw down with a $3.9 billion outflow for the week which compared to the $2.0 billion outflow last week

Both Equity and Fixed Income ETF money flow was negative for the week with Equity ETFs losing $1.8 billion in fund flow and Fixed Income passive products losing $209 million in investor capital

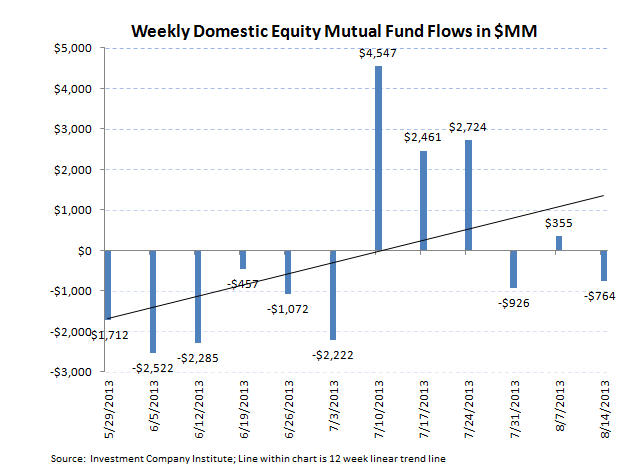

For the week ending August 14th, the Investment Company Institute reported softening equity mutual fund flow trends albeit positive flow trends and accelerating week-over-week declines in fixed income mutual funds. Total equity fund flow totaled a $1.4 billion inflow which broke out to a $2.2 billion inflow into international equity products and a $764 million outflow in domestic stock funds. These trends compared to the week prior which experienced a much larger inflow of $3.4 billion with positive flow in both stock categories. Despite this deceleration in stock fund flows, the year-to-date weekly average for 2013 now sits at a $2.7 billion inflow for total equity products, a substantial improvement from the $3.0 billion outflow averaged per week in 2012.

On the fixed income side, outflow trends worsened during the week with the aggregate of taxable and tax-free bond funds combining to lose $3.9 billion in fund flow. This was almost a doubling of the $2.0 billion lost in the prior week with the taxable bond category specifically shedding $1.8 billion in the most recent period versus a slight inflow of $33 million last week. Tax-free or municipal bonds continued their sharp outflow trends losing another $2.0 billion in the week ending August 14th, in line with the outflow from the week ending August 7th. The 2013 weekly average for fixed income fund flow has now drastically declined from 2012, now averaging just a $469 million inflow this year, a far cry from the $5.8 billion weekly inflow averaged last year.

Hybrid funds, or products that combine both fixed income and equity allocation, continue to be the most stable category bringing in another $1.5 billion in the most recent weekly period. The year-to-date weekly average inflow for hybrid products is now $1.7 billion for '13, almost a 100% increase from 2012's $911 million weekly average.

Passive Products Were in Outflow Last Week:

Both categories of exchange traded funds experienced redemptions by investors for the week ending August 14th. Equity ETFs lost $1.8 billion, the biggest outflow in 7 weeks and a reversal from the robust $6.2 billion which came into stock ETFs last week. Despite this week's outflow, 2013 weekly average equity ETF trends are averaging a $3.6 billion weekly inflow, a sharp improvement from last year's $2.2 billion weekly average.

Bond ETFs also had soft trends in the most recent weekly period losing $209 million in fund flow. This slight outflow was a vast improvement from the substantial outflow from last week of $3.8 billion however the 2013 weekly average is now just $401 million, much lower than the $1.0 billion average weekly bond ETF inflow from 2012.

HEDGEYE Asset Management Thought of the Week - Follow the Money Flow:

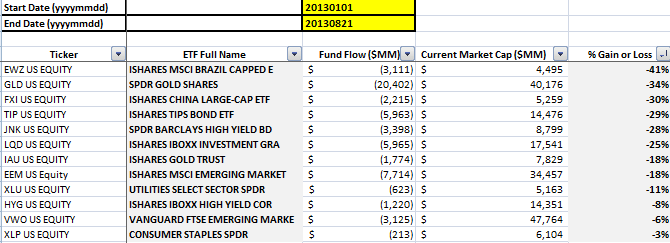

With exchange traded funds generally representing 60% institutional use and 40% retail investor use, we think it is valuable to look at year-to-date specific product flow trends to see where investor interest is gravitating. Looking at the ETF products with the most substantial fund flow as a percent of outstanding assets relays improving flow in domestic equity sector ETFs and also passive Japanese products. Conversely, 2013 has marked substantial selling of emerging market and bond ETF products thus far this year.

The biggest loss year-to-date has come from the MSCI Brazil iShare which has had over $3.0 billion withdrawn by investors or over 40% of its assets. The SPDR gold ETF has experienced a fund flow loss of similar magnitude having lost $20 billion from investor withdrawals or over 34% of its assets to end at a level of $40.1 billion. Bond products have seen accelerated loses since the beginning of the summer with the iShare TIPS fund now having seen a 29% redemption for the year and the SPDR high yield ETF, the JNK, now having lost 28% of its assets or $3.3 billion. With the passive unmanaged nature of these fixed income ETFs, we see these products as continuing to have disproportionate risk as bond fund flows continue to weaken.

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA