This note was originally published August 16, 2013 at 09:45 in Macro

- Bullish position on the UK (etf: EWU) and Germany (EWG) remains.

- Eurozone fundamentals inching higher; investor sentiment improving on weak comps. On a relative basis the Eurozone is well below its historical growth average and churning only modestly higher as deep structural imbalances and the lack of credit drag on growth.

- We underline the significance of Eurocrat and ECB resolve to lend support to the region and markets (at all costs), which, along with marginally better data, should continue to support Eurozone capital market performance.

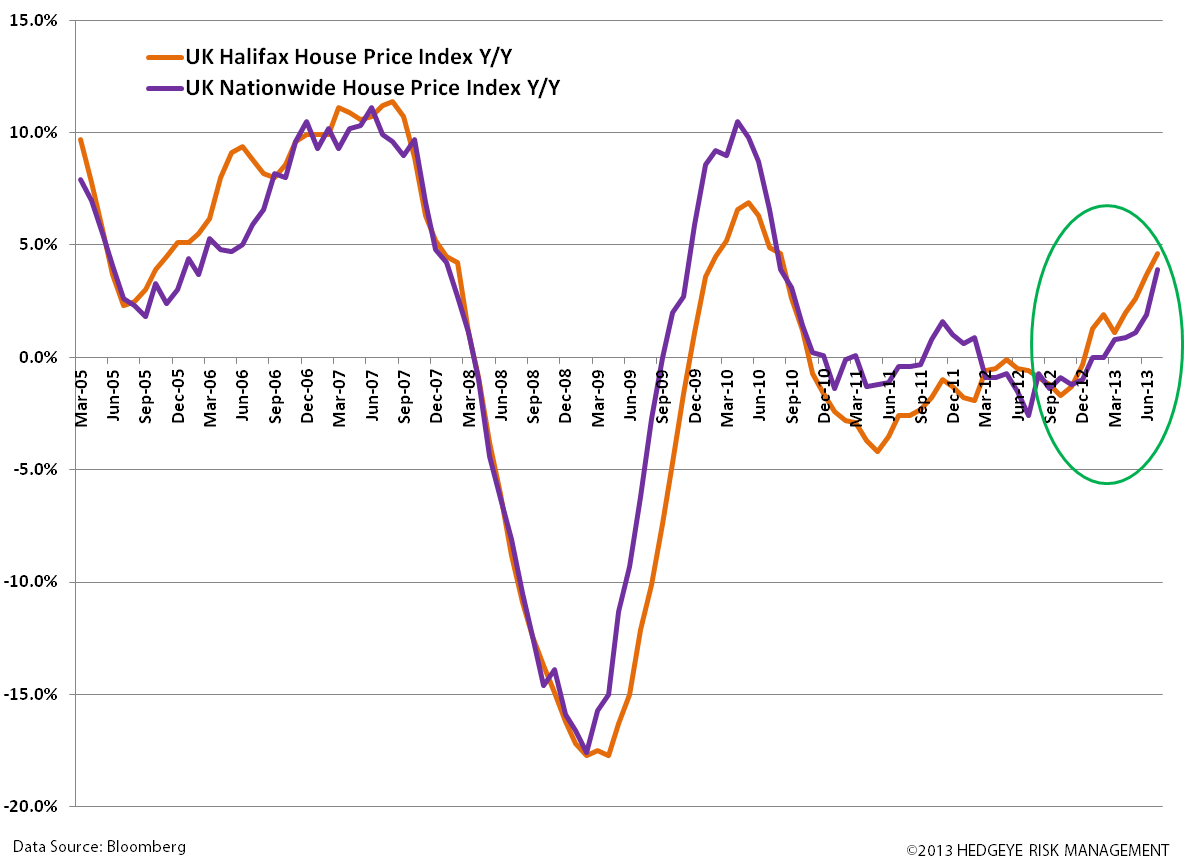

UK’s Island Economics

In support of our fundamental bullish call on the UK economy since our June 11th European update presentation titled “Where Does Europe Go From Here”, yesterday the UK printed a strong Retail Sales figure of 3.0% in July year-over-year (exp. 2.4%) vs 1.9% JUN.

The print and the down move in the FTSE100 yesterday prompted us to add the UK via the etf EWU to our real-time portfolio positions on the long side.

Our outlook on the UK is data and price dependent and hasn’t changed: we expect to see outperformance from the UK economy versus many of its European peers due to its decision to issue austerity earlier in the fiscal consolidation cycle. We are now seeing stronger signs of improved consumer sentiment, and expect PMI readings to maintain their level above the 50 line (expansion) into year-end. Beyond retail sales, industrial production and housing figures have improved year-to-date, and while wage volatility and sticky stagflation persist, we view reductions in the saving rate as another indicator of improved sentiment. Further, we’re bullish on the changing of the guard at the BOE to Mark Carney – while it’s up for argument on just how effective tying monetary policy to the unemployment rate is, we like the Bank’s move towards a more transparent state to better manage and guide expectations.

Eurozone Inching Higher

The big news this week was a better-than-expected first print of Q2 GDP out of the Eurozone, a follow-on to improving fundamental data out of the Eurozone in recent weeks.

The Eurozone’s +0.3% Q2 GDP rise marked the end of an 18 month recession (cheer!), and the figure beat our expectations for only modest improvement over Q1 (consensus was at +0.2%), especially in a quarter that was hampered by bad weather (including serious flooding throughout central Europe), continued misdirection in economic leadership from France’s Hollande (France has the second largest economy behind Germany in the Eurozone), and continued political strife in Italy, Spain, and Portugal.

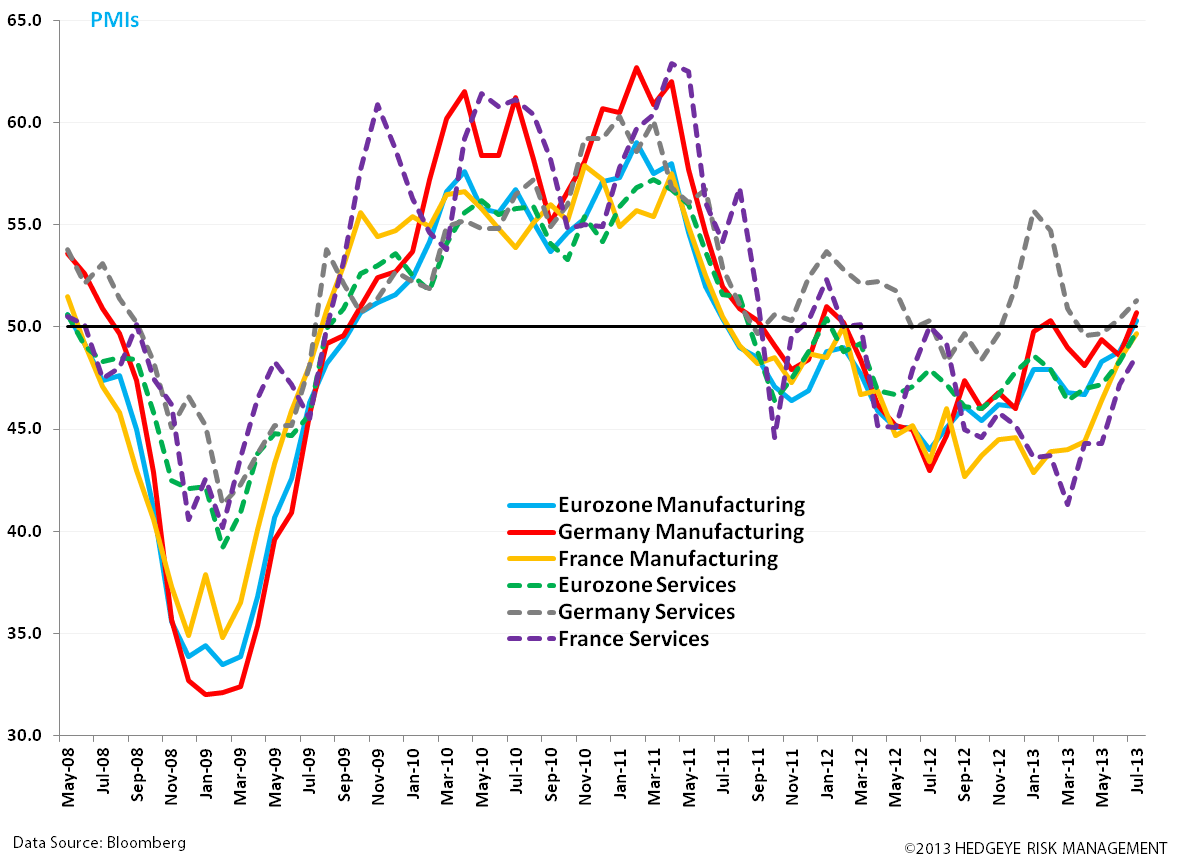

Clearly the data is looking better. Germany and France also beat Q2 GDP expectations. Germany reported growth of +0.7% Q/Q (+10bps above expectations) versus 0.0% in Q1 and France rose +0.5% Q/Q (+30bps above expectations) vs -0.2% in Q1. Add to this performance PMI figures that have improved across the region over the last 3-5 months (reaching over the 50 line in the last 1-2 readings) and improvement in sentiment readings across the core and periphery.

Risk Spreads are dropping to new lows. Also, 10YR Spanish and Italian bonds are trading at their tightest spreads over comparable German paper in more than two years at ~252bps and 235bps, respectively.

Not All Is Rosy

What’s our read? While there’s optimism to be had on improving data, GDP was still down -0.7% year-over-year in Q2 and we expect a very slow churn higher in Eurozone GDP in the balance of 2013. Certainly GDP will remain well below the pre-crisis average of 2.1% (since 2000) as the region hits the reset button on standards of spending and lending as budgets are readjusted at the government and household levels. We maintain our call for 2013 GDP between -0.8% and -0.6% year-over-year.

Beyond struggling to reset spending and lifestyles habits, here are some significant hurdles that we expect will continue to weigh on Eurozone GDP:

- The slim availability of credit, in particular to the small and medium sized businesses, the core drivers of growth and employment (see chart below on ECB Loans to Non-Financial Corporations and Households as proxy—at or near all-time lows)

- Diminished credit quality of banks, especially across the periphery, as they report increasing non-performing loans

- Further bank write-downs of non-performing assets

- Labor market reforms slow to enact or institute at all

- A protracted unemployment overhang, especially youth unemployment across the periphery, that will limit consumer spending and confidence

- Political uncertainty, in Italy, Spain, and Portugal, to weigh on budget reforms and confidence

To throw out a couple anecdotes from the media stories we’ve recently come across that paint a still subdued outlook, we include:

- The WSJ reported that auto sales in Europe are so bad that less than half the factories in the region operate at the minimum 75% of capacity needed to break even. It said that those operating below that level are mostly located in Italy, France, and Spain whose economies have been hit by the crisis. The article noted that governments in Western Europe are worried about seeing more workers join the ranks of the unemployed and that unions are aggressively protecting jobs, while the courts have also been sympathetic. The paper said that because of this, auto makers are losing billions of euros a year by retaining workers and factories they no longer need.

- A poll by ING-DiBa AG and the University of Hohenheim shows that only 17% of Germans believe that the worst of the Eurozone crisis is over, while 91% think that the crisis will still go on for a long time. Only 10% of Germans believe that politicians are being honest with citizens regarding Eurozone issues.

Concluding Thoughts

Our call remains that into Q4 we expect European PMIs to hover around the 50 line (ups and downs) but not to show a material breakout given the very weak structural issues that we do not see inflecting materially over the intermediate term, including weak credit conditions, high unemployment, alongside political uncertainty at the country level – Italy, Spain, and France in particular. We continue to be fundamentally bullish on German and the UK equities, so should we see any outperformance from PMIs, we think it could come from these two countries.

As it relates to the capital markets, we think a much larger force versus marginal improvement in fundamental data is the political resolve of the Eurocrats and Draghi to lend fund if needed (back-pocket OMT ready) and prevent any country from leaving the Eurozone, which we think can continue to stabilize and push markets higher. Already we’re seeing domestic and international investors become increasingly confident in Draghi’s heavy hand and buying distressed asset, for example housing in Spain and bank debt across the periphery, as the EU banking system slowly continues to heal.

Enjoy the weekend!

Matthew Hedrick

Senior Analyst