This note was originally published August 07, 2013 at 14:11 in Retail

We were negative on RL coming out of the print in May – not because we did not like what the company was doing – quite the opposite, actually. RL was investing in IT systems, stepping up its Retail and e-commerce investments on a global scale, and preparing to take in the Chaps license from Warnaco. But these initiatives cost money, and the outward capital flow unfortunately precedes turning on the revenue spigot by at least 9-12 months. Simply put, there’s almost no way that returns can turn up when this is happening, and valuation multiples don’t expand when returns are going down. Given that RL’s multiple was sitting near peak, it made sense to us to wait to get involved until the market to freaked out over sloppy results.

The financial results played out as we thought, but the reality is that if you asked us a couple of days ago if we’d see a sell-off this quarter, we’d have said ‘probably not’. Don’t get us wrong, the quarter itself was poor, with 4% sales growth de-levering to an 11% decline in EBIT. Comps came in down -1%, and inventory growth outstripped sales growth by a factor of 2x. Again, not return-enhancing metrics – consistent with our concern last quarter. But that said, we think that expectations were set appropriately headed into this print. 2Q guidance of lsd growth and margins down 300-350bp vs last year seemed to be the big culprit, as they suggest EPS in the range of $2.25-$2.20 vs the consensus at $2.57. The question, therefore, is likely whether that is the real number, or if it is a sandbag.

Our sense is that financial reality is somewhere in between guidance and current estimates. We’re coming out at $2.31 for 2Q, and where the consensus lands will be critical as it relates to our near-term take on the stock. We’ll watch that in the coming days, and will be back accordingly.

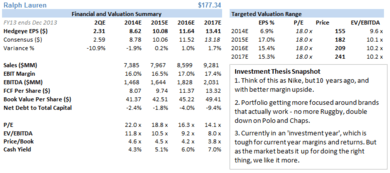

Long-term, we continue to like RL in that the actions that the company is taking today should propel RL’s top line over $10bn within 3-years, push EBIT margin into the 17-18% range, and take RNOA from 24% today to 35% as asset turns increase on top of a higher margin business. Those characteristics are tough to find. But the catch, once again, is that our estimates are hovering right on top of the Street’s for the next three years (based on last night’s consensus numbers – see table below). That’s rare for us and RL. We’re usually far above. That tells us that the Street finally has it right, or we’re missing something. Either way, we don’t have the conviction to jump in at current levels – at least not while it is still in the early half of its ‘investing year’.

Ralph Lauren Investment Summary

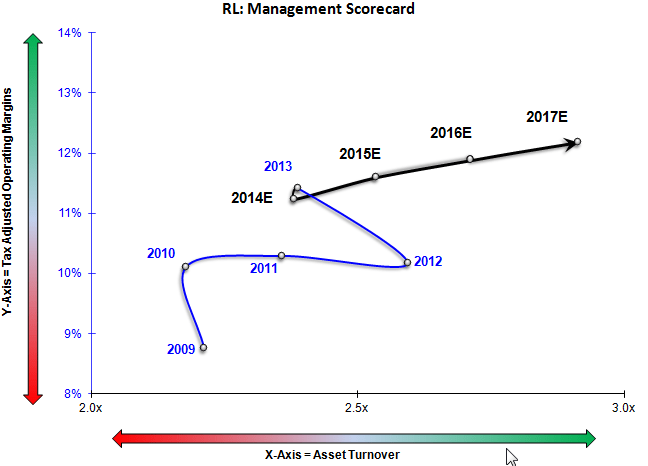

RL Profitability Roadmap: Solid Outlook Over Our TAIL (3-Year) Duration

HERE'S OUR NOTE AFTER RL'S 4Q RESULTS

5/23/13

RL: The Market Is Not Recognizing The Risk

Takeaway: Stocks don't go up when sales slow, costs increase, capex goes up materially and the stock is at 20x EPS. A textbook 'investing year.

Conclusion: We like what RL is doing, but the near-term financial implications will not be pretty and EBIT growth trajectory and RNOA will suffer. Even though this impact will likely be temporary, investors will need to wait until near the end of this calendar year until the risk profile improves. Until then, valuation matters.

DETAILS

We're surprised that RL was not down more on its 4Q print. Yes, the company overdelivered -- in typical RL fashion. But there are enough factors that are changing negatively on the margin that we think will make RL a good candidate for multiple compression in the sloppy quarters that lie ahead in the upcoming fiscal year.

We like this company as much as we ever have. It continually reinvests in its intellectual property to elevate the retail experience and gain share -- something that has worked for RL without fail.

Case in point…we kept a little scorecard of all the times that retailers and brands mentioned the words 'omni-channel' in press releases and earnings calls this earnings season. We stopped count at 100, and no, it did not take us long to get there. This has officially become the biggest cliché buzzword since 'supply chain' made it on to the scene 15 years ago. We swear that half of the execs talking about omni-channel don't even know what it means (if there even is a universally-understood definition). They're just following the cool kids.

Ralph is one of the cool kids. It did not discuss 'omni-channel' once on its call or press release. Why? The reality is that it has been implementing a true omni-channel strategy for much of the past five-years…at a time when no one knew what it even was. Now RL is implementing retail and e-commerce models that others will be trying to implement in another five years. Simply put, we think that RL will continue to be a winner.

But this is one of those years where the negatives to the story are likely to outweigh the positives. Specifically…

- FX will be a meaningful headwind in FY14 -- especially given RL's significant exposure to Japan. Check out the Yen's move over the past six weeks. Not good. FX is a $75mm hit to EBIT for the year.

- RL's Global SAP implementation, Korean e-commerce rollout, acceleration of retail rollout -- including NY flagship. There's another $75mm hit to EBIT this year.

- Capex is going from $276mm last year to up to $450mm in FY14 -- that's one of the biggest capex increases we're seeing out of anyone in retail.

In fairness to RL, it has proven to be an exceptional steward of capital in the past, and we have no reason to think that will change this year. But the reality is that the $150mm in extra costs puts RL in a hole for 13% EBIT growth. This would be ok if we could justify solid double-digit top line growth as an offset -- but the reality is that we cannot (even if partially due to FX). So we've got slowing sales, eroding margins, and a step-up in capex. Any way we cut it, we can't justify the combination of these factors leading to any form of multiple expansion.