This note was originally published August 09, 2013 at 14:58 in Restaurants

On Wednesday, Malcolm Knapp gave us a glimpse of how ugly sales trends were in July when he released his estimates for the month. Although the numbers released by Black Box yesterday are not as dire, it remains clear that the industry is beginning 3Q13 in a hole and must play catch up in order to make the numbers.

As a refresher, Knapp reported that July 2013 same-restaurant sales declined -3.8%, while traffic trends declined -5.1% -- both metrics slowed sequentially over a markedly weak June. Black Box numbers were slightly less gloomy, as same-restaurant sales declined -0.9%, while comparable traffic trends declined -2.2%.

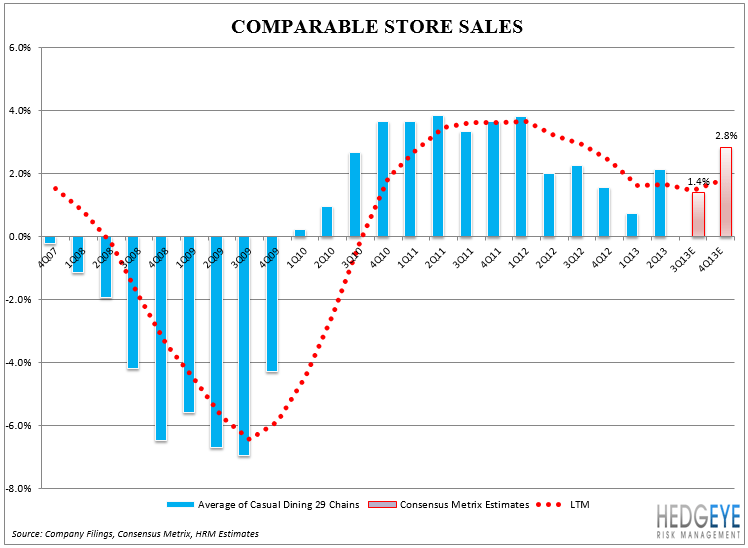

Currently, our Casual Dining Index (a compilation of 29 casual dining chains) is estimated to post same-store sales growth of +1.4% in 3Q13, before accelerating to +2.8% growth in 4Q13. This would indicate, that for the balance of 3Q13, same-store sales need to accelerate by 200-300 bps to make the current estimates. Knapp noted that while all four weeks in July were negative, each successive week in the month was sequentially better than the prior.

We believe a massive acceleration in trends will be difficult to achieve. According to our Casual Dining Index, average same-store sales growth in 2Q13 was +2.1%, indicating that same-store sales for the period were up +1.7% on a LTM basis, down significantly from its +3.7% peak in 1Q12.

With the casual dining group trading at 23.5x P/E and 8.8x EBITDA (adjusted for CHUY and NDLS), it appears as though the market is expecting a noticeably sizeable acceleration in same-store sales. While the job market continues to show signs of improvement, at least in the headline numbers, it seems as though the weakness we have seen in July can be partially attributed to a surge in gas prices.

Our top short in the casual dining space remains RRGB. The company is due to release 2Q13 earnings on August 15h before the open. We will post on anything incremental after the call.

Howard Penney

Managing Director