This note was originally published at 8am on August 02, 2013 for Hedgeye subscribers.

“Think of me like Yoda, but instead of being little and green, I wear suits and I’m awesome. I’m your bro — I’m Broda!”

-Keith McCullough

I’m not going to try to weave that recent #Tweetshow gem from Keith above into some sort of missive theme. It just makes me laugh.

Let’s start somewhere else.

Back in school the bullies used to wait until Picture Day to punch a kid in the face. Risk Management in Central CT starts early.

Yesterday could probably be considered an investor picture day and the market delivered a bevy of black eyes to the perma #EOW contingent.

In related End of World and Recency Bias news, it’s now August and for the better part of the last 5 months, the ‘Sell in May’ mantra has been iteratively thesis drifting towards an un-convicted call to ‘Sell in September’ alongside another crescendo in congressional budgetary and debt ceiling discord.

September, incidentally, also happens to be when the seasonal distortion present in the reported econ data flips from a headwind to a tailwind - serving to (optically) amplify any positive underlying economic trend.

Hearing implied volatility in ‘sell in December & go away’ calls is ripping!

Back to the Global Macro Grind……

For much of 1H13, our pro-domestic growth call was buttressed by some positive redundancy. That is, with our model signaling for the slope of U.S. growth to accelerate out of 4Q12, we had a bullish absolute call for domestic, consumer-centric equities.

With most of Europe Bearish TRADE & TREND, an expectation for slowing EM growth, and upside to troughed out expectations for U.S. growth, we also had a relative call supporting a long bias to domestic exposure.

In essence, even if U.S. growth turned out to be “okay” instead of very good, we were still taking a high probability swing at positive absolute performance.

As it happened, our conviction in the strength of the relative call was tested more acutely as we transitioned out of 1Q. A quick review of the last few months will be helpful in understanding how our view has evolved to where it is today.

As we moved through 2Q, it become apparent that consumption growth, while remaining healthily positive, would not accelerate sequentially. In part, this was not unexpected.

Fiscal policy impacts generally hit on some short lag and the 1Q13 comparison was artificially difficult as consumer spending in 1Q benefited from the special dividend deluge and compensation pull-forward that occurred in December 2012 ahead of impending fiscal cliff related tax law changes.

With the savings rate rising in 2Q and disposable personal income growth largely flat, divining the slope of sequential consumption growth just became simple math.

Further, with federal employment growth running at approx -2% YoY and furloughs for ~700K+ federal employees beginning in July – which, in tandem, equates to ~7% reduction in income for ~2% of the workforce – upside to disposable income growth would likely be constrained in 3Q13 as well.

Would a modest deceleration in consumption matter from a market perspective? – becomes the simple, but nontrivial investment question.

As we highlighted yesterday, when re-evaluating positioning, it’s often helpful to start by detaching yourself from the myopia of trying to contextualize every market tick and, from a broader perspective, remember how this whole reflexive economic thing works. Archetypically,

Rising spending drives income and employment higher which, in turn, drives consumption and confidence higher in a virtuous, self-reinforcing cycle. Credit serves to amplify the cycle with credit expansion following pro-cyclically as loan demand and creditworthiness both increase alongside rising incomes and higher household net wealth.

In short, if the TREND slope of improvement across the balance of key macro drivers (employment, consumption, credit, confidence) remains positive, and if the forward research view and risk management signals are still aligned, the path of least market resistance and the highest probability call is to stick with the TREND - particularly if you don’t have a discrete catalyst for a reversal.

So, how are the aforementioned macro metrics #TRENDing?

Labor market trends remain positive with Initial Claims continuing to register accelerating improvement while employment growth as measured by the BLS’s Establishment and Household Survey’s both remain positive.

Confidence readings across the primary surveys continue to make new 5Y highs and are finally beginning to break out of their post recession channel.

Business and Residential Investment growth has accelerated in each of the last two quarters.

On the credit side, banks are finally beginning to report positive loan growth, Commercial & Residential Real Estate loan demand continues to improve and credit standards across commercial and consumer loan categories continues to ease.

Consumption has shown a discrete acceleration, but faces some well advertised, nearer-term headwinds. If labor market trends remain positive, does the market look past middling consumer spending growth over the next few months with an eye towards a diminishing fiscal drag and easy compares as we annualize the sequestration and the tax law changes in early 2014? That’s an increasingly probable risk for the consensus #EOW bear crowd to manage.

Now, Is Congress a discrete negative catalyst? As our Healthcare Sector Head, Tom Tobin would say; you can never underestimate congress’s ability to create a crisis so they can subsequently save us from it. Congressional risk may rise, on the margin, but this iteration is likely to be mostly noise so long as the fundamental trends remain positive.

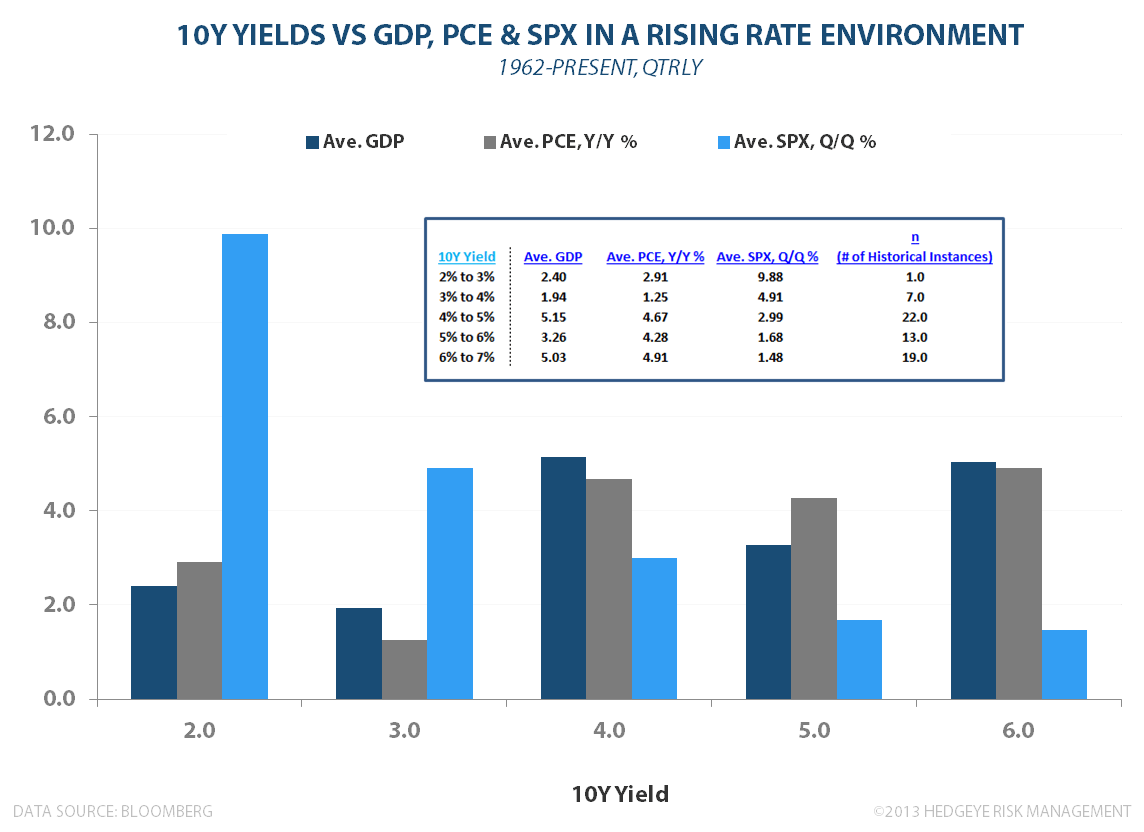

Is #RatesRising a catalyst? We have a hundred page slide deck and a 60 min presentation on why we don’t think a return to interest rate normalcy is a threat to growth or market performance. (ping sales@hedgeye.com if you’d like a copy)

Is today’s Employment Report a discrete catalyst? Yes, but not really. We don’t have any particular edge on the NFP number, but given the ongoing strength in the jobless claims data it’s more likely than not we print something close to consensus at 185K.

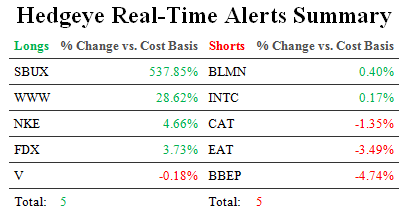

So, now that I’ve peppered you with bullish jabs for the last 800 words, I’ll remind you that we’re not bullish on everything at every price. In fact, we moved to net neutral into yesterday’s close (5 longs, 5 shorts) as almost everything pro-growth, domestic consumption (XLY, XLF, $USD) signaled immediate term overbought.

But we’ll take our long exposure higher again on the signal so long as the TREND slope of improvement in the Macro data remains positive. At present,….

“Your Friend, the Trend Remains” - Broda

Our immediate-term Risk Ranges are now as follows:

UST 10yr 2.60-2.78%

SPX 1690-1712

Nikkei 14101-15095

VIX 11.96-13.74

USD 81.62-82.87

Gold 1251-1326

80o and sunny on tap for the weekend. Enjoy.

Christian B. Drake

Senior Analyst