Estée Lauder’s 4QFY13 results surprised to the upside as organic sales growth came in at +8%, driving $0.24 in EPS versus $0.21 consensus. While FY14 guidance of $2.74-2.87 (inclusive of $0.10 FX headwind) falls below the Street at $2.94, organic sales growth guidance of 6-8% is reassuring. In 4QFY13, high-end brands grew 20% versus overall sales growth of 6%. Investors have clearly been reassured by the underlying top-line trends. As we wrote yesterday, the investment community was waiting for reassurance around the company’s sales growth. Concerns regarding the implementation of SMI also needed to be addressed and, judging by the results and earnings call commentary, it seems that the company is nearing the end of the “investment” phase of the initiative and is poised to reap some rewards.

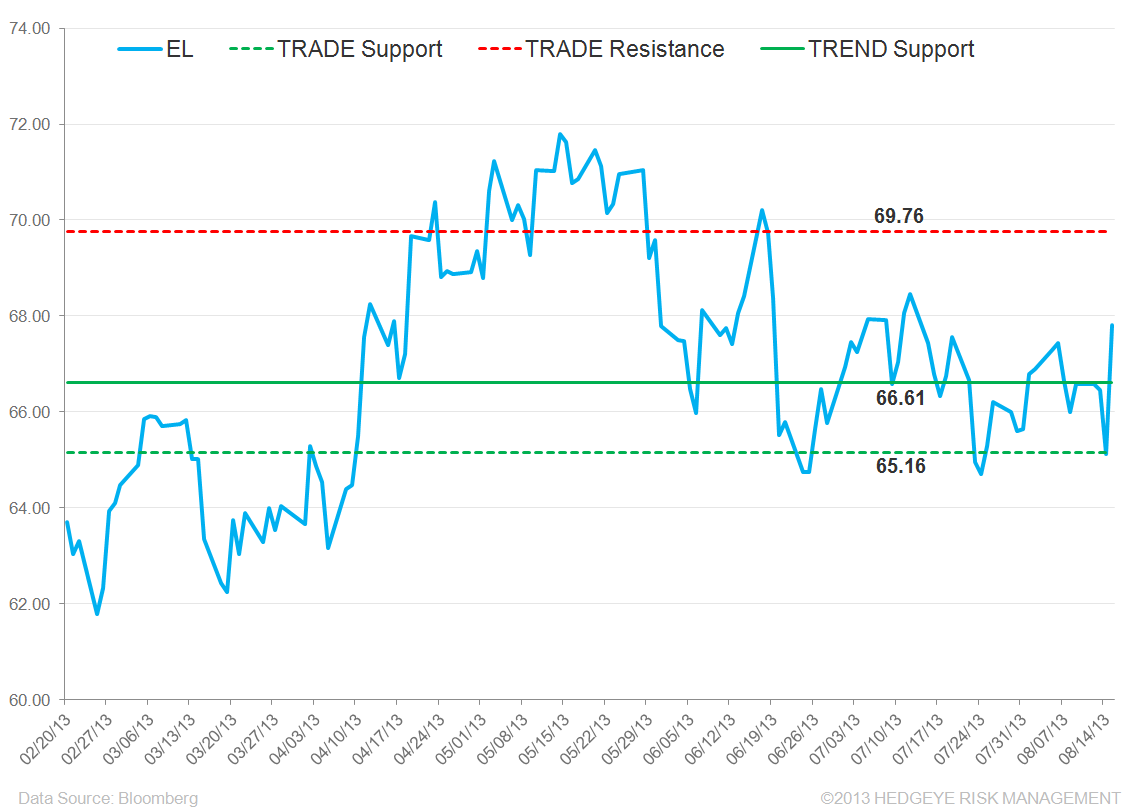

In terms of the quantitative setup, according to our macro team’s quantitative model, the stock is breaking out above its intermediate-term TREND line.

Below, we highlight the positives and negatives from 4QFY13 earnings, the FY14 guidance, and the earnings call this morning.

What we liked:

- EPS of $0.24 beat consensus expectations of $0.21

- Organic sales growth of 8% came in above expectations

- High margin luxury skincare brands growing 20%

- Mgmt expecting to outgrow industry by at least 1%

- Industry growth expected to be 3-4% in FY14, 4-5% thereafter

- FY13 operating cash flow increased 9%, mgmt guiding to 14% growth in FY14

- Performance and opportunity in emerging markets bode well for long-term growth

- EL fundamental setup continues to be attractive with robust growth and yield

What we didn’t like:

- Slow sales growth continuing in U.S., Southern Europe, Korea

- FX continuing to be a significant headwind, FY14 impact difficult to estimate at this point

- “Temporary softness” in the U.S. – remains to be seen if this is so

- Gross margin decline in 4QFY13 – transient, according to mgmt

Rory Green

Senior Analyst