In the game Jenga, each player, in turn, pulls a wooden block out of a stacked tower with the goal of not causing the tower to collapse. It idiom speak, its tantamount to trying to avoid pulling the straw that breaks the camel’s back.

The economy over the last 4 years has been a kind of Inverse Jenga with policy makers, economists, and strategists speculating on what combination of policy and macro factor(s) need to be in place for the ethereal economic edifice to not only not re-implode, but to propagate a positive reflexive economic cycle.

Are those requisite ‘pieces’ in place currently?

For thought experiment sake, let’s suppose you just recently crawled out from under your Edward Snowden hideout rock to find the following dynamics. While you don’t want to be long everything equities at every price, on balance, would you provide a persistent short bid given the following macro realities?

- Labor Market: Breaking a 4 year trend and showing accelerating improvement in the face of a negative seasonal headwind and a discrete fiscal policy drag

- Credit: Household Debt/GDP has retraced back to trend, household credit growth has moved back to the zero line and consumer and commercial loan demand and credit availability are both improving.

- Confidence: After a 5 year tread-sideways stint, all measures of consumer and business confidence are legitimately breaking out.

- Private Sector Balance Sheet: Financial assets are making new nominal highs (largely a boon to the top 10%) and home prices (broad populace ownership) are retracing their losses and now growing double digits. Some measure of wealth effect should follow on the back of significant NTM asset re-flation. Corporate cash remains solid, corporate balance sheets have been buttressed by a multi-year cost cutting run, and corporate earnings as a % of GDP are still near peak. Mean reversion from peak margins remain an obvious risk to prices, but an acceleration in investment spending presents an similarly positive prospect for TREND economic growth.

- Flows: Flows can amplify and/or dominate fundamentals for extended periods and, at present, flows to equities, and U.S. equities in particular, have inflected. Funds continue to flow out of Fixed Income alongside #RatesRising, EM equities/bonds/currencies hold negative leverage to both #StrongDollar & #RatesRising, as does Gold the broader commodity complex.

- Fed: Central Bank intervention, despite its supportive role, has increased market uncertainty and served to both shorten economic cycles and amplify market volatility. The Fed has used its ‘communication tool’ and consensus has begun to accept the impending end of unprecedented market intervention – whether they are doing it b/c organic trends are good or to avoid burgeoning asset price imbalances is probably a secondary point. In reality, it is probably some combination of the two.

- Valuation: Market valuation is getting a bit rich on a measure like the Shiller P/E, but still has headroom for a turn or two on a convention P/E basis, earnings yield basis, etc. Valuation, in itself, is not a catalyst over the immediate and intermediate terms.

Of course, on the other side, muted Inflation, stall-speed real wage growth, slack capacity, rising oil/gas prices, Congress and rest of world risk - among others - remain ongoing concerns.

The Jenga question is whether the confluence of the positive dynamics above represent a macro factor cocktail sufficient for catalyzing a self-reinforcing upswing domestically?

YTD market performance has clearly backed pro-growth positioning, and with sentiment still middling, the domestic macro data coming in good, and the quantitative setup for equities still bullish, we’re inclined to stick with a constructive outlook for the U.S.

In short, we don’t think improving employment, #StrongDollar, #RisingRates are negative dynamics and expect an equity sell-off to be met with a bid as we move towards support. The levels we’re watching for on the SPX are TRADE Support at $1659 and TREND support down at $1631.

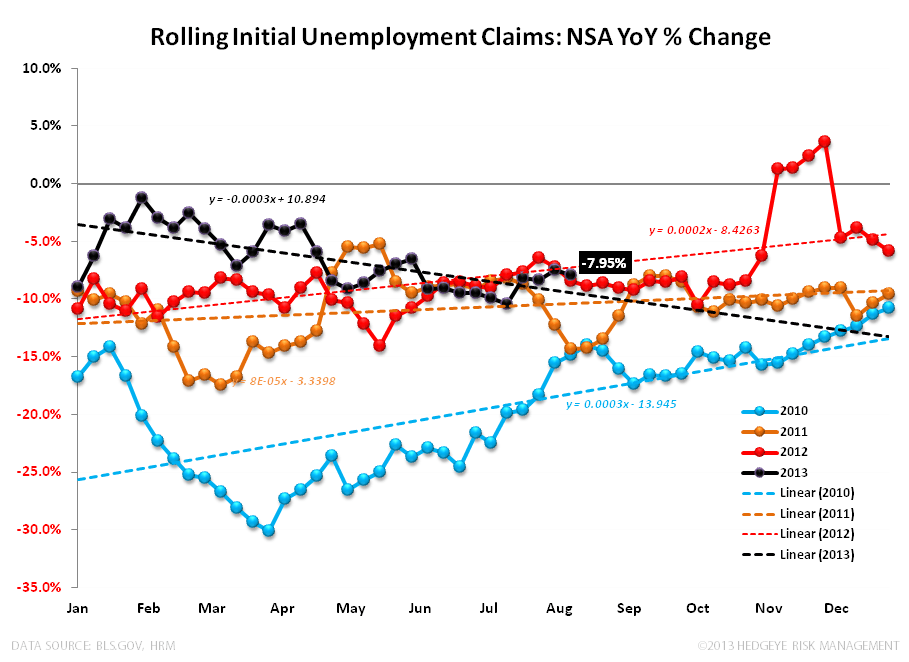

INITIAL CLAIMS: ANOTHER NEW LOW

NSA: Non-seasonally adjusted claims, our preferred read on the underlying labor market trend, made a new absolute low for the cycle at 280K - marking its third consecutive sub-300K reading in a row and the lowest since September 2007. On a YoY basis, initial claims accelerated to -11.7% from -9.9% the week prior with the 4-week rolling average improving 50bps to -8% from -7.5% the week prior.

Excluding the (seemingly) anomalous data point for the week ending 7/19, the average YoY improvement over the last twelve weeks is -9.8% - a very strong rate of improvement and one that continues to defy the trend of the last three years (see the slope of the linear trend lines in the 1st chart below). Improvement in the 4-wk rolling measure of YoY Claims should show marked improvement next week as the one weak data point of the last 17 weeks rolls off.

SA: The seasonally adjusted, headline claims number printed its best number of the year, and best number since October 2007, at 320K. This weeks data represents an accelerating YoY rate of improvement of -12.8% YoY (vs -9% the week prior) with 4-wk rolling average down 4K WoW.

As Josh Steiner and our financials team re-highlighted last week:

Based on our analysis of the seasonality distortions shifting from headwind to tailwind from September through February, we think the SA number, with no underlying fundamental improvement, will shift from 333k to around 305-310k. There is, however, clear underlying fundamental improvement, so we wouldn't be surprised to see a 2-handle on the SA initial jobless claims reading by late 1Q14.

The Labor Market is probably the most critical piece in Economic (Inverse) Jenga, and it continues to show acceleratign improvement.

Christian B. Drake

Senior Analyst