This note was originally published at 8am on August 01, 2013 for Hedgeye subscribers.

“We are sowing the seeds of Ignorance, Corruption, and Injustice, in the fairest field of Liberty.”

-John Adams

According to Joseph Ellis in Revolutionary Summer, that’s what John Adams wrote to Joseph Hawley on August 25, 1776. Adams could have said that about heavy-handed government in August of 2013 – and, in principle, he’d still be right. But betting against the prospects of American growth rising above compromised politicians has often been wrong.

Politics versus people - that’s not new. Americans generally dislike socialists and/or plutocratic pomp. On August 13, 1776, George Washington called the British out like most of us call out conflicted central planners today: “Their cause is bad; their men are conscious of it, and if opposed with firmness and coolness… victory is most assuredly ours.” (Revolutionary Summer, pg 86)

I like that, a lot.

Back to the Global Macro Grind…

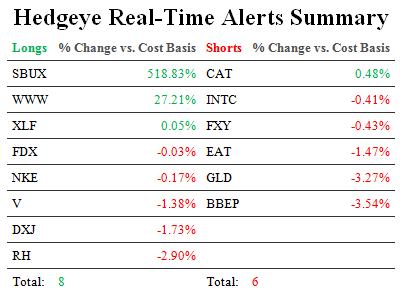

I also like seeing all of the growth factors in our multi-factor model rip to the upside. It’s especially fun to watch on days like yesterday when my contra-stream (I built one on Twitter of market pundits who are wrong at least 65% of the time) starts whining.

Winning versus whining – that’s not new either. There are a lot of losers out there who whine but, over time, Americans eventually put those people on mute and roll with winners who have principles they can associate with.

There’s been a lot of whining about US GDP “dropping to 1%” in Q213 – but that didn’t happen either. US GDP has by no means had a championship season, but it’s been a heck of a lot better than Q412’s 0.38% - and it’s what happens on the margin in macro that matters to us most. Here’s the Q213 breakdown:

- Consumption (C) = +1.8% quarter-over-quarter, contributed +1.22% to Q213 GDP

- Investment (I) = +9.0% quarter-over-quarter, contributed +1.32% to Q213 GDP

- Government (G) = -0.4% quarter-over-quarter, contributed -0.1% to Q213 GDP

In other words, government spending fell as Consumption and Investment rose. Good, eh? It’s not a new story in America. It just hasn’t happened in a while – and that’s the point.

Since C + I + G + (EX-IM) is the GDP equation, whiners (particularly partisan ones) will add that:

- Net Exports (EX-IM) = +5.4% quarter-over-quarter, but contributed negatively to GDP by -0.81%

- Inventories contributed positively to GDP by +0.4%

- Inflation (PCE Deflator) was at its 2nd lowest level ever of +0.8%

But let’s get real here – who really cares about those line items when the big stuff (Consumption and Investment growth) is finally going the right way for once?

To give them some air-time, the Princeton/Yale/Harvard Keynesian Econ 101 textbooks will also whine about “net exports being down because the Dollar went up” and “disinflation is a threat to our academic dogma” – but again, who cares?

I went to Yale and, admittedly, was confused about this “inflation is good, deflation is bad” concept. My family doesn’t buy into the class warfare labeling thing, but we do buy (and invest) more when the purchasing power of our hard earned currency appreciates.

Is Bernanke’s fear-mongering about “deflation” really the hobgoblin?

We answer that on slide 36 of our current Global Macro Themes deck (ping sales@Hedgeye.com if you’d like a copy) where we outline a recent study by Atkeson & Kehoe that spans a time period of 180 years (across 17 countries) that found no relationship between deflation and depressions.

The objective study actually found a greater number of episodes of depression with economies experiencing inflation than with deflation. Over the 180 year time period:

- 65 out of 73 deflation episodes had no depression

- 21 out of 29 depressions had no deflation

So what say you President Obama? Yes, we know. We know that you know that we know.

Bernanke’s cause is no longer saving us from the end of the world. That was so 3-5 years ago. Perversely, it’s to talk down growth in order to uphold un-precedented (and un-elected) central planning power on the order that this country hasn’t seen in 237 years.

But he’s conscious of it. So is the country.

Mr. Market gets it too. That’s why all of these end of the world (#EOW) trades that were driven by an explicit Policy To Inflate (Gold, Treasury Bonds, etc.) are coming unglued. That’s also why growth investors are getting paid.

Liberty flows. She still plays to the hands of the independent minds. We don’t have to be long Bernanke Bubbles in order to get paid. We have to be right on the slopes of the lines in our model.

Growth’s slope is up; Inflation’s is down – and unlike the government, I like that, a lot.

Our immediate-term Risk Ranges are now as follows (12 big macro risk ranges are in our new Daily Trading Range product):

UST 10yr 2.52-2.71%

SPX 1682-1699

Nikkei 13421-14295

VIX 11.96-13.85

Yen 97.12-101.01

Gold 1279-1327

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer