Conclusion: Macy’s has been #1 on our list of top three shorts (followed by Gap and Dick’s), and as such, the print today is not a surprise to us. We have no crystal ball as to the comp that Macy’s has been generating, so we’re not claiming to have forecasted the specific sales shortfall in this given 13-week period. But we’ve viewed the triangulation of M’s P&L, Cash Flow Statement and Balance Sheet as being like an increasingly stressed balloon under water. This event does nothing other than strengthen our confidence in our call.

DETAILS

Out of any name we cover (and we cover just about all of retail) there is not a single name we find ourselves more fiercely debating than Macy’s. The most common bull arguments we hear are a) the company has been so poorly run for so long, and that investments in Magic Selling, MyMacy’s, Omni-Channel, etc… are making up for years of share loss, and b) the stock is so cheap at just 12x earnings.

But we think that valuation is irrelevant, as it is not a catalyst – and never has been – especially with a levered zero-square-footage growth retailer where numbers can change so quickly.

We recognize that there are certainly ways that Macy’s can operate more efficiently and can fine-tune its approach to going after share-of-wallet. But we think that there are too many factors converging on both the P&L and balance sheet that are stacking the odds against a positive change in return on invested capital. When returns are going down, there’s no reason a 12x multiple can’t turn into a 10x multiple – and there’s no rule that says that it needs to stop there. Factors that specifically concern us are as follows…

1) Top Line

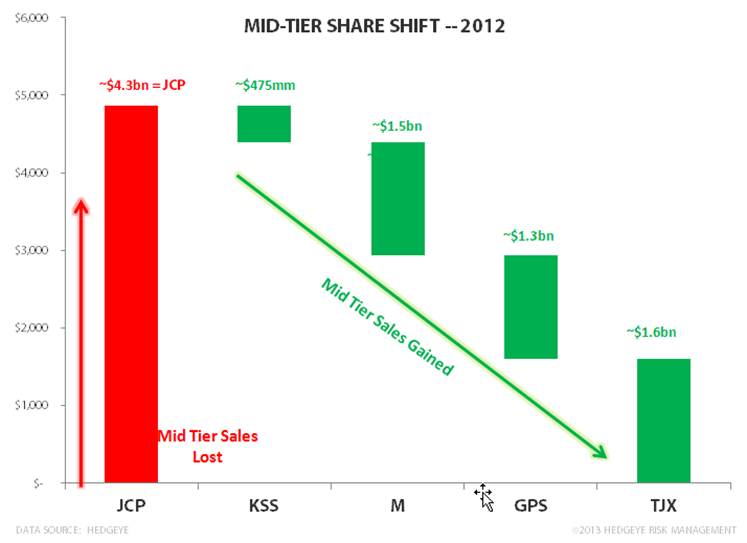

a) We can’t forget that in 2012, Macy’s grew its top line by $1.5bn, which is the same time that JC Penney lost $4.3bn in sales. Macy’s management completely discounts the idea that any of its sales gain has come at the expense of JCP. If not outright cocky, we think that at a minimum management is being intellectually dishonest. JCP will start to regain share at some point in 2H --- or lose share at a lesser rate (which is a negative change on the margin for competitors). If JCP fails, it will inflict pain while it tries. The other retailers (including Macy’s) are in denial.

b) Macy’s management did a very poor job articulating the source of the 2Q sales miss. Transaction count was down 1.6%, and they noted that consumers are more interested in buying cars, houses and spending on home improvement than they are in spending in department stores. Seriously? What’s ridiculous is that there’s no way for them to know why consumers are NOT shopping in their stores. This is particularly troubling in light of point A – in that Macy’s is blaming macro factors at the same time we’re seeing sales competition heat up in the mid tier.

c) The company noted that comps had turned up in 3QTD. That’s nice given that we’re just starting back-to-school. But there’s a long way to go in BTS. We give the company credit for trying to keep expectations somewhat grounded that its way too early to declare victory – especially when there so many unknowns as to why sales performance missed like it did throughout 2Q.

2) Gross Margins were down only 10 basis points for the quarter – which is pretty impressive given the magnitude of the sales miss. But keep in mind that the sales/inventory spread eroded by 700bp, as inventories were up 6.4% despite a 0.8% sales decline. Had the company more appropriately cleared out inventory on hand, we’d have seen more Gross Margin pressure. (Notice the swing into the third quadrant of our SIGMA chart below). Either way, management has been vocal about saying that gross margins would be tough to improve from here, and that EBIT margins would need to come from SG&A leverage…

3) …but SG&A is headed higher. In order to kick start the top line and have the proper marketing programs in place for a less-certain 2H, the company is taking up marketing costs. We’re not knocking it, as it’s the right thing to do. But the simple point is that with both the top line and gross margins under pressure, the P&L gets levered in the wrong direction with an uptick in SG&A. Let’s not forget that Macy’s has almost $400mm in interest expense as well – which is another negative leverage kicker.

4) Lastly, capex is running at $925mm this year. There hasn’t been any increase in capex guidance, which is good, but the reality is that it is still up 33% from $698mm last year.

The punchline is that we’ve got sales down, gross margins rolling over, increased SG&A spending, and higher capex. In that context, the ‘cheap valuation’ argument is simply irrelevant. We’re modeling flat operating profit over the next four years, with earnings growth only being driven by 3-4% of financial engineering (debt paydown and repo). Our earnings 3-years out are 25% below consensus (see our assumptions in financial summary below). While a 10x p/e and 5x EBITDA multiple only suggests a stock in the low $40s out that far, the reality is that those same multiples could get to a stock with a 3-handle closer in.