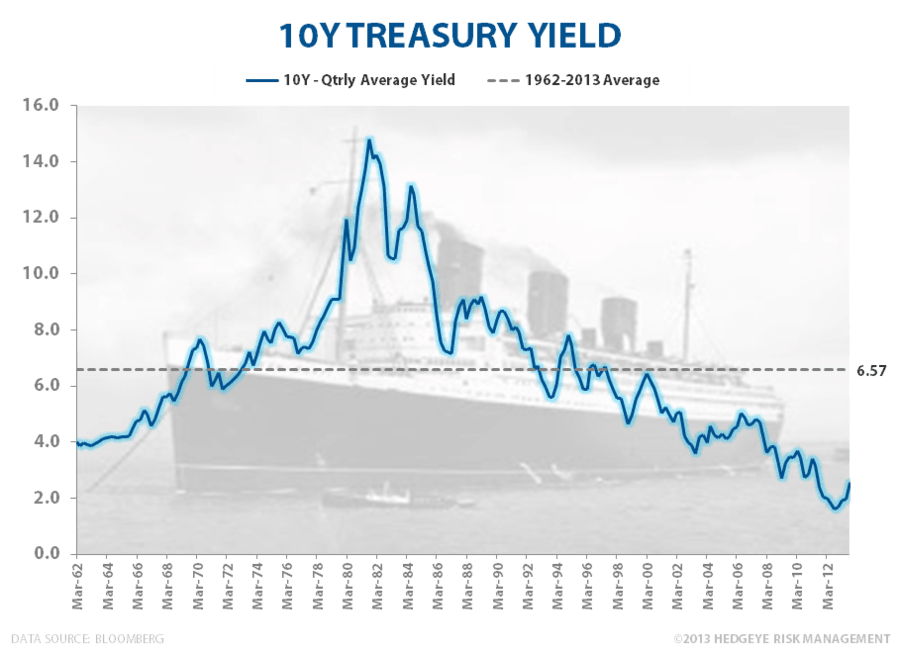

#RatesRising and #DebDeflation remain two of our Top-3 Global Macro Themes here in the third quarter of 2013.

They are both playing out as a) U.S. economic data delivers sequential #GrowthAccelerating in July and b) Jackson Hole gets discounted as a hawkish event.

The 10-Year Treasury is now yielding 2.71%. It's a nice step up of higher-lows and higher-highs. We are now up +14 basis points month over month.

Bottom line: #RatesRising has epic reverberations. Epic implications. That is why we are banging this drum so loudly.