There have been a few upgrades in the sector recently based, in part, on optimism about business getting less bad. This thesis has certainly played out in the gaming and cruise line sectors. While the same thesis will eventually play out in lodging - even a broken clock is right twice a day - we are not seeing any evidence of sequential improvement. Our 2010 estimates for HOT EBITDA and EPS remain 10% and 30%, respectively, below the Street.

YoY occupancy remains way down from last year. As we opined in our 01/07/09 post, "FILL 'EM AND THEY (INVESTORS) WILL COME", improvement in occupancy is a strong signal that there is indeed light at the end of the tunnel, even if lower rates are still driving overall RevPAR down. Lodging stocks typically do not sustain rallies until occupancy bottoms. Unfortunately, there is no visibility on that pivot.

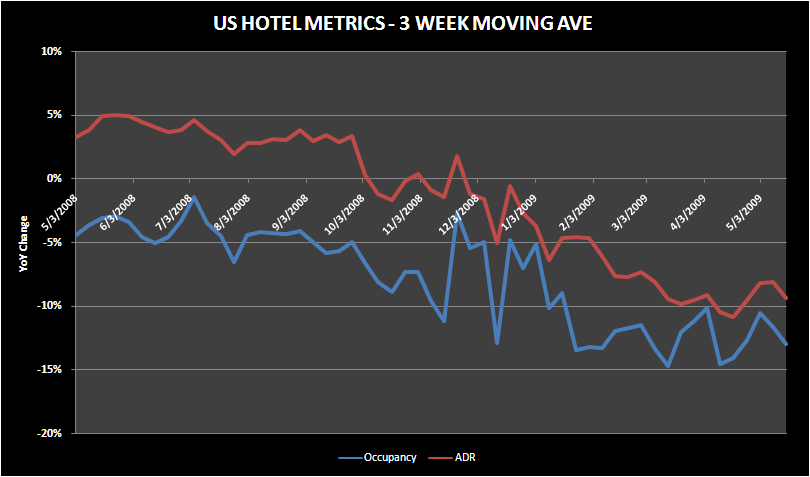

As can be seen from the chart below, lodging fundamentals are not improving. We're not sure what data other sell-side analysts are looking at, but the STR data doesn't show any recovery or stabilization and our network of private hotel franchisees certainly doesn't see things getting any better. Just because the YoY decrease in RevPAR isn't accelerating doesn't mean that we've reached the bottom or that there is any improvement in sight. Occupancy fell 11% in April, and is tracking down 12.5% for the first 3 weeks of May. Given the lack of demand for rooms, the only way to fill rooms is by stealing share from your neighbor by dropping price. In order to change this you need real demand growth stimulated by job growth and income growth - things stabilizing at bad levels isn't enough.

We will give credit when credit is due. Starwood has done a great job cutting costs, but we do not believe that all of these cost cuts are sustainable, especially the ones at the capex level. We wrote about this in our 5/2/09 note "YOU TUBING HOT". Like the gamers, many hotel companies are simply deferring capital expenditures. The deferred maintenance capex issue is why many of the recent asset sales have come with mandatory investment requirements. We heard that the W New York - The Court & Tuscany is on the market for $100MM but the required capital improvements are almost as high as the ask price. Cuts on timeshare are only sustainable until the inventory on hand is sold, and then companies need to start investing again - otherwise we need to look at these businesses on a liquidation basis, not a multiple basis.

We understand the reflation trade. In fact, Research Edge was a big proponent of this thesis beginning in early March (thanks Keith), especially with the gaming and cruise lines sectors. That trade has worked. With cost of capital rising and valuations rising there needs to be more to keep this rally going. How about the fundamentals? Not quite yet.