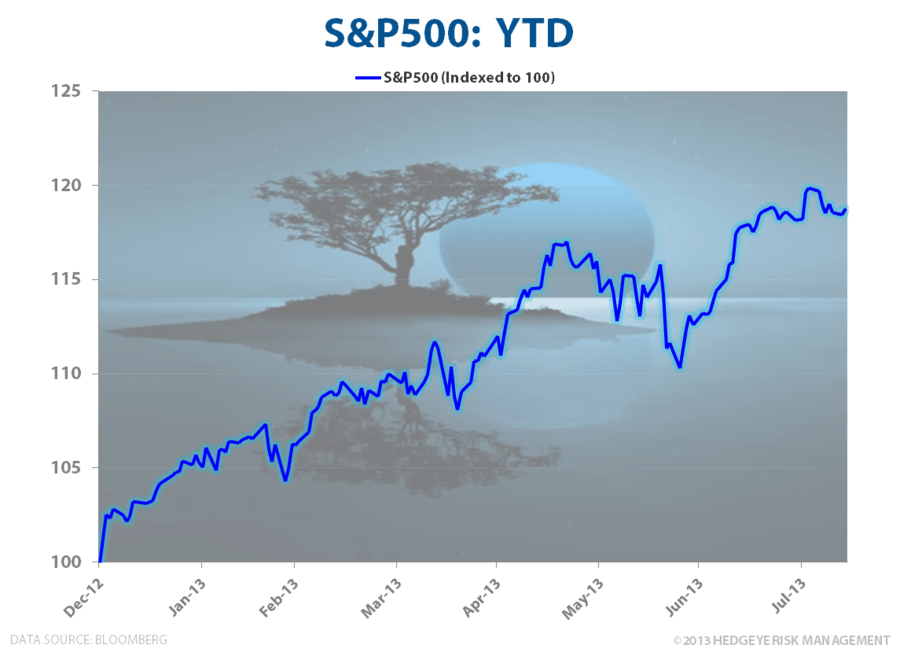

Here's a look at the epic move in the S&P 500 since we first made our call to go long U.S. equities. Stick with the game plan that's working. Get long growth, short fear.

To be sure, we are plenty bearish, on plenty of things, the things that are actually going down. But here's the point: bears have been mauled and have missed the move in equities for the better part of the year. Meanwhile, as money continues to flow from the bond market to avoid losses, equities will be waiting with open arms to receive this capital exodus.