Summary Bullets:

- Short EVEP remains a Hedgeye Best Idea (added 4/26/13 at $47.00/unit);

- 2Q13 results were in-line, no change to 2H13 guidance, an uninteresting quarter operationally;

- 1st Utica acreage monetization was NOT a positive surprise;

- EVEP is pushing up against its total leverage covenant and likely needs to issue equity in the next six months;

- EVEP is now capitalizing a material amount of interest, and maintenance capex is likely understated; both items are "artificially" boosting DCF.

2Q13 results in-line……Adjusted EIBTDA came in at $52.6MM vs. $55.6MM consensus, and DCF of $0.61/unit (0.80x coverage) was in-line. For the quarter, we have clean EPU of $0.13, FCF of -$0.96/unit, CF of $0.93/unit, and open EBITDAX of $42.4MM. EVEP maintained 2H13 guidance. Operationally, it was an uninteresting quarter.

Utica acreage sale #1 was NOT a positive surprise……EVEP popped 9% on Friday morning as, in our view, investors mistakenly extrapolated EVEP’s sale of 4,345 net acres in Guernsey, Noble, and Belmont counties for $56MM, or $12,900/acre, over its entire package for sale. This is by far EVEP’s best Utica acreage, and the price tag is neither surprising nor indicative of potential prices for its other acreage packages. We were modeling $20k/acre for the Guernsey acreage. In late June 2013, Eclipse Resources acquired ~49k net acres in the core of the Utica (Guernsey/Belmont/Noble/Monroe counties) from The Oxford Oil Company at a price between $10k - $15k/acre (exact terms not disclosed). Prospectivity of the play varies across EVEP’s acreage, and the acreage sold was largely in the “core of the core.” We assume that EVEP monetizes 45,000 net acres in the wet gas window of the Utica for $205MM (~$4,500/acre), including the package already sold, between now and the end of 1Q14. The big piece is the 11,000 net acres in Carroll County (mostly in the NW corner of Carroll County). We model $5k/acre, though with CHK dominating Carroll County Utica leasehold, it’s more difficult to handicap.

Total leverage covenant is a problem……EVEP ended 2Q13 just inside its total debt to adjusted EBITDAX covenant of 4.25x. We estimate that EVEP has to come up with ~$150MM of cash before the end of 3Q13 to stay compliant with that covenant. The first Utica acreage sale for $56MM has them in need of another ~$100MM cash before quarter-end. It will likely come in the form of either additional Utica acreage sales and/or an equity raise. The situation does not improve from there, as EVEP will again be bumping up against the total leverage covenant in 4Q13. Bottom line – unless EVEP can manage a large asset-for-equity deal, we believe that a ~$200 - $250MM secondary needs to happen within the next 6 months. Either way, equity is needed to remedy a stretched capital structure and liquidity position ($520MM drawn on the $710MM borrowing base).

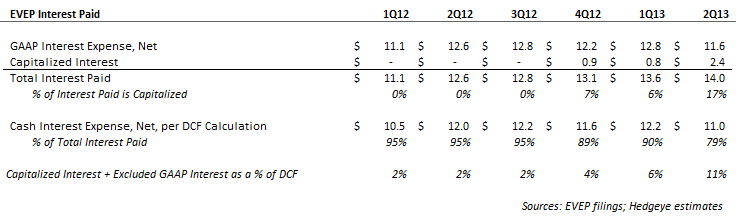

EVEP capitalized 17% of interest expense in 2Q13……EVEP started capitalizing interest in 4Q12 when it began investing heavily in its unconsolidated midstream affiliates (UEO and Cardinal). In 2Q13, EVEP capitalized $2.4MM of interest, which was 17% of total interest paid and 9% of DCF. EVEP is certainly permitted (under FASB Statement No. 34) to capitalize the interest associated with the midstream build-out, but we consider it somewhat aggressive as capitalizing interest increases DCF, which is the key metric for an MLP like EVEP, and the metric most use to value the equity. It doesn’t sit right with us to see a serial capital raiser capitalizing a material amount of interest paid. If EVEP expensed this interest paid, and deducted all GAAP interest expense from DCF, then DCF would have been $23.1MM, for 0.71 coverage, vs. reported $26.1MM and 0.80 covereage.

Maintenance capex remains below 2012 trend……Maintenance capex in 2Q13 came in at $14.7MM, or $0.94/Mcfe produced. This was 48% of total capex, $30.7MM, and is roughly half of the DD&A rate, $1.76/Mcfe. The maintenance capex rate of $0.94/Mcfe suggests that EVEP is one of the most efficient E&Ps with the drill bit in North America, though its annual reserve replacement statistics paint a different picture, such as its $4.49/Mcfe Drill Bit F&D Cost (excluding revisions) in 2012. EVEP’s maintenance capex took a curious step change lower in 1Q13, coming in at $13.6MM, falling 29% QoQ, and coinciding with the Company’s drop in DCF and distribution coverage. Maintenance capex remains below 2012 trend by $4 – 5MM, which is ~17% of DCF. We believe that EVEP’s maintenance capex is understated, and as a result its DCF overstated.

Don’t worry, be happy……EVEP’s Executive Chairman John Walker said this on the 2Q13 conference call: “I want to thank those analysts who took the time to really understand EVEP and the Utica play, as well as our investors who hung in there as our unit price fell into the low 30’s. I wish that we or myself personally, at EnerVest and EVEP could have bought units as the price declined, but we've had restrictions on buying or selling EVEP units since last year because of our ongoing negotiations. Again thank you very much.” No comment necessary.

Kevin Kaiser

Senior Analyst