Post election optimism and some better-than-bad data in India masks serious potential pain on the horizon

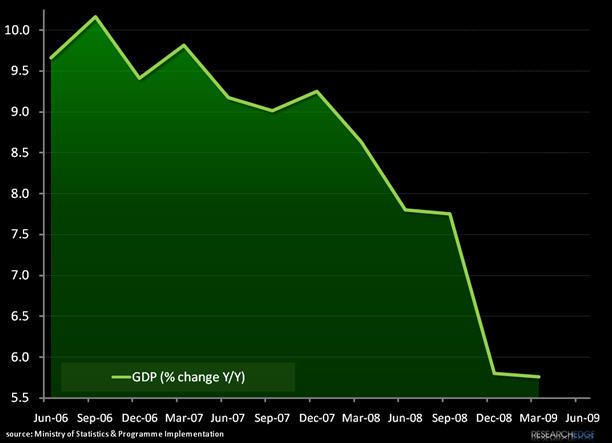

Today's data release from the ministry of statistics showed that Indian GDP grew at a better than hoped for rate in Q1: 5.8% Y/Y. Although the rate of growth has now contracted on a y/y basis for 5 consecutive quarters the figure still represents much better than anticipated recovery in response to government stimulus programs and rate cuts. This is good news indeed for The victorious Singh Administration as it attempts to shore up confidence, but it still greatly lags government target growth rates needed to drive higher employment and consumer demand.

Prime Minister Singh's initial moves in his new term are critical. India needs to borrow a significant amount to implement new stimulus and social programs, bringing the total borrowing for the year to 3.62 trillion Rupees - yet with total public debt above 75% of GDP there is a real chance that the country's credit ratings will slip below investment grade exacerbating already expanding long term yields. Any move that could undermine confidence in the nation's credit carries risk since a stronger Rupee will be critical, with over 80% of current external debt already denominated in foreign currencies and new capital raises likely to be issued in USD, not to mention an import dependence for key commodities.

Inflation and Debt

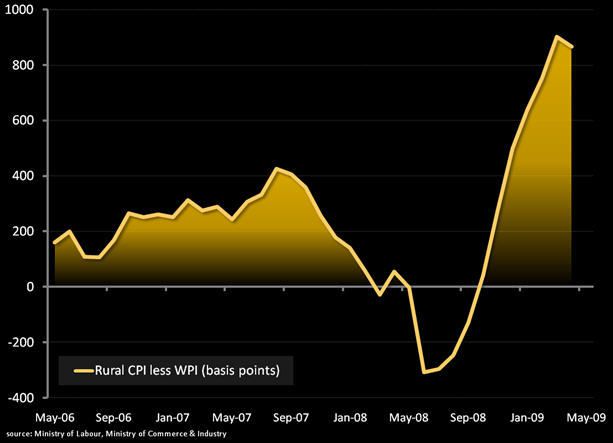

Wholesale price Inflation levels released yesterday by the Ministry of Commerce registered below 1% for the 11th consecutive week. With inflation seemingly tamed, market expectations are squarely pegged on continued easing from the central bank as the government gets down to the business of kick-starting growth. One cloud on the horizon however has been the continuing resilience of consumer inflation, with the measure for rural workers still hovering above 9% and urban measure over 8%. With government subsidies currently insulating consumers from direct energy commodity pressure (more below) the discrepancy is driven by pressure in consumer staples -making further rate cuts less tenable.

Note that earlier this week the Food Ministry responded to rising sugar prices by banning new contracts and new positions in existing contracts on the National Commodity Exchange in Mumbai. Prices of Sugar have been up sharply on anticipation of major shortfalls in domestic production for the current cycle, with an expectation that India will be a net importer this year for the first time since 2006.

Another new development is a move by the newly empowered INC administration to lift fuel price caps and allow refiners to maintain natural margins in response to lower oil prices. This lifts a major burden from state controlled energy companies and has driven equities sharply higher but it also adds an element of inflationary risk in the near term if oil reflation (or rupee deflation) resumes.

Still, this week's news is decidedly net positive for India Equity Bulls and, more importantly, for the Indian economy and people. Singh -a massively respected leader before this new victory, has been handed a very large check in the form of the optimism sweeping the nation post election, and he will need every ounce of that goodwill to buoy sentiment as his administration makes some very tough calls. As investors we continue to remain skeptical on the long term prospects for the Indian Economy and have a short term bias on the equity market there.

Andrew Barber

Director