RRGB remains on the Hedgeye best ideas list as a SHORT.

Summary

RRGB is scheduled to release earnings before the market opens on 8/15. Given that RRGB is one of the last casual dining companies to report 2Q13 EPS, it should be no surprise that they will likely miss the revenue estimates due to the soft sales environment prevalent within the industry.

Heading into the print, our primary question remains unanswered: In a slowing sales environment, can RRGB prudently manage the expense line while reinvesting in the core business? This concern arises as the company is in the midst of a core brand revival that has consensus expecting significantly improved traffic trends in the quarter. While these efforts may prove successful over time, we believe this is unlikely to occur in 2013.

The list of casual dining companies that have seen estimates revised lower following 2Q13 earnings releases is quite long, as RT (-83%), BJRI (-8%), CAKE (-2%), and TXRH (-1%) have all been revised down over the past month. While RUTH (+7%) saw EPS revised up, we would rightfully point out that the company competes more in the fine dining segment as opposed to the hyper competitive bar and grill category. Given the current secular trends, we believe there is a high possibility RRGB will report a miss on both the top and bottom line in 2Q13.

Sales Trends

Over the past month, consensus estimates for 2Q13 revenue growth have fallen from +7% to +5%, while EPS estimates for the same period have remained steady at $0.66 or +26.9% growth. With 2Q13 revenue estimates having been toned down, we believe 3Q13 guidance is too aggressive, as consensus is looking for EPS growth of +37% on revenue growth of +8%.

Consensus expectations are for same-store sales of +2.7% and +3.0% in 2Q13 and 3Q13, respectively. While these may be high, more concerning to us is the expectation for traffic growth of +30 bps and +70 bps over the same period. Considering the industry is experiencing a noticeable decline in traffic, this would indicate that RRGB is picking up that market share. We view this as unlikely.

HEDGEYE – We don’t believe the current brand transformational initiatives will be enough to fix the secular decline in traffic the company has been experiencing since 1Q12.

Food Costs

RRGB’s food costs are estimated to decline -17 bps Y/Y in 2Q13, after falling -59 bps Y/Y in 1Q13. The company is selling more liquor, which is helping its food cost trends, but we believe red meat will continue to see significant inflation over the balance of the year.

HEDGEYE – We believe any benefits RRGB experiences in 1H13 will reverse and, ultimately, negatively affect margins in 2H13.

Labor Costs

The labor cost line should be a point of concern for RRGB. The company saw labor costs rise +34 bps in 1Q13 and the Street is looking for labor costs to be flat Y/Y in 2Q13.

HEDGEYE – With the probability of a top line miss very high, we suspect the company will see some labor deleverage in 2Q13.

Other Operating Costs

Over the last three years, lower other operating costs has been a big source of operating margin improvement for RRGB. Since peaking at 22.6% of sales in 2Q10, other operating costs has declined more than 200 bps to 20.5% on a LTM basis. In 1Q13, other operating costs declined -6 bps Y/Y and is expected to decline -20 bps Y/Y in 2Q13.

HEDGEYE – We believe RRGB’s brand transformation initiatives will require some investment and, without a significant improvement in traffic, the company will have a difficult time leveraging this line.

Operating Margins

As it stands today, the Street is expecting the company to post margin improvement on the back of lower food costs and by leveraging other operating costs. Consensus estimates are for operating margin improvement of +45 bps Y/Y to 5.56% of sales. This would be RRGB’s best operating margin line since 2Q08, when operating margins were 6.37% of sales.

HEDGEYE – We view this as unlikely, given the slowing sales trends and the investment needed to transform the Red Robin brand.

Sentiment

Highlighted in the chart below, 31.3% of analysts rate RRGB a Buy, 56.3% rate RRGB a Hold, and 12.5% rate RRGB a Sell. Further, short interest has moved lower since early July and now makes up 9.23% of the float.

HEDGEYE – While EPS estimates have begun to move slightly lower over the past 3 months, we would contest they are still too high.

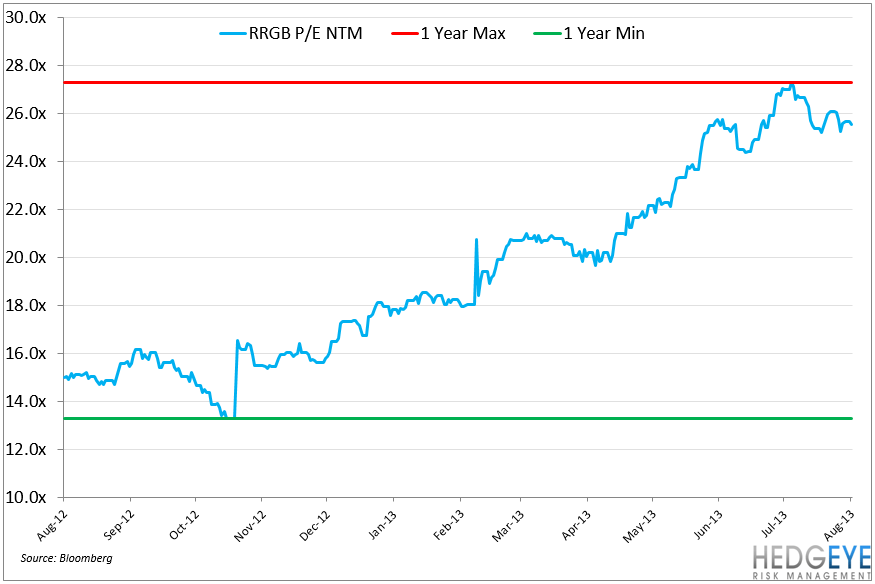

Valuation

At 8.2x EV/EBITA, RRGB is trading at a slight discount its Casual Dining peer group at 8.8x EV/EBITDA. Despite trading at this discount, it is important to remember that RRGB’s valuation is at peak levels and we believe, for now, it is appropriately valued below its peer group.

HEDGEYE – We believe the whole group is likely to see multiples revised lower in the current quarter.

The company is hosting its 2Q13 earnings call on Thursday morning at 10am EST. We'll post on anything incremental after the call.

Howard Penney

Managing Director