Following the release of 3Q13 results, we continue to believe that the long-term potential of JACK is underappreciated, particularly with respect to the future growth of Qdoba. The company’s recent initiatives only enhance this view.

3Q13 Results

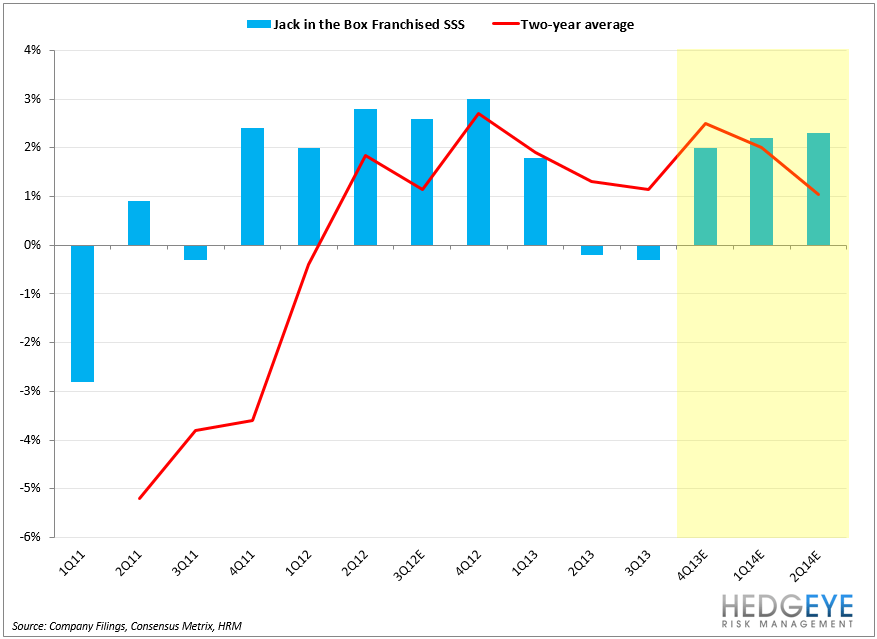

JACK reported 3Q13 adjusted EPS $0.03 above consensus along with a top line miss (-3.71%) that was in line with industry softness. Company sales trends for the quarter were mixed as same-store sales for Jack in the Box fell short of expectations (+1.2% versus +1.8% consensus), while same-store sales for Qdoba came in above expectations (+0.5% versus -0.1% consensus).

Strategic Initiatives

In June 2013, upon completion of a strategic market review led by newcomer Tim Casey, the company announced plans to close 67 of its company-operated Qdoba restaurants. We responded positively to this announcement in our note, “Jack: Right-Sizing The Qdoba Ship,” when we wrote:

“The upside in JACK, as we have often written, is in the multiple assigned to the Qdoba business. To the extent that it occurs, future upside to earnings is obviously also a positive.”

We continue to stand by this, and believe that CEO Linda Lang’s assertion that the closures are expected to result in higher future earnings, AUV’s, restaurant operating margin, cash flow and ROIC, will come to fruition. To date, the company has closed 62 underperforming Qdoba locations, transferred 3 to a franchisee and will close the remaining 2 when their leases expire at the end of the year.

As for Jack in the Box’s refranchising strategy, they intend to sell 29 additional restaurants by the end of FY13 and an additional 60 by the end of FY14. Upon completion, the company’s goal is to have between 80-85% of Jack in the Box locations franchised, which similar to the closure of Qdoba stores, should have a positive impact on financial performance.

Change at the Top

The company also announced this week that CEO Linda Lang plans to retire as of Jan. 1, 2014, and will be replaced by current President and COO, Leonard Comma. We expect this transition to be seamless, as Leonard is well-respected within the industry and, in our view, fully capable of leading JACK in its future endeavors.

Potential Upside

In our view, the company’s aggressive move to restructure Qdoba is likely to improve the brand’s profitability and should provide investors with the confidence to assign the brand a growth multiple. Due to this renewed growth profile, we see approximately 25% potential upside in the stock over the next 2-3 years. Below we offer some more thoughts on 3Q13 results:

What We Liked

- Strong strategic plays in refranchising and restructuring by Jack in the Box and Qdoba, respectively

- Jack in the Box 3Q traffic improved sequentially from 2Q

- Raised full-year restaurant operating margin guidance to 17-17.5%

- Qdoba closures expected to add $0.15-$0.16 to FY13 EPS from continuing operations

- Raised full-year operating EPS guidance to $1.72-$1.78

- The company has $84.7m remaining in its stock buyback program that expires in Nov. 2014 and an additional $100m authorized for stock buybacks that expires in Nov. 2015

What We Didn’t Like

- Jack in the Box company same-store sales were down in July

- Scaled back full-year guidance for new Qdoba restaurants from 70-75 to 65-70

- Qdoba margins decreased 270 bps to 20.6% in 3Q, driven by a combination of sales deleverage, commodity inflation, product mix changes and increased staffing levels

- Competitive environment – seeing deep discounting from some casual diners as well as strong value plays by other QSRs

Howard Penney

Managing Director