This note was originally published at 8am on July 26, 2013 for Hedgeye subscribers.

“Forces might make it easy for group-based processes to turn collaborations into cheating opportunities.”

-Dan Ariely

There’s some serious irony that I’m finishing up my behavioral economics review of Dan Ariely’s The (Honest) Truth About Dishonesty while our profession gets its reputation tarred and feathered by the fun cops.

I call it our profession, because it is. We are all responsible for self-policing this Street. For too long we have allowed our compensation structures to cloud our definition of grey. Leadership principles are black and white. It’s time to champion transparency and accountability.

No, it’s not easy to write about this. I think we all have former friends who have lied to us. Accepting that isn’t easy either. Social groups affect us in many ways that we are too human to understand.

Ariely reminds us that “when cheaters are part of our social group, we identify with that person and, as a consequence, feel that cheating is more socially acceptable. But when the person cheating is an outsider, it is harder to justify the misbehavior, and we become more ethical in our desire to distance ourselves from that immoral person and from that other out-group.”

“… results show how crucial other people are in defining acceptable boundaries for our own behavior, including cheating. As long as we see other members of our own social groups behaving in ways that are outside the acceptable range, it’s likely that we too will recalibrate our own internal moral compass and adopt their behavior…” (pages 206-207).

Leadership isn’t how much money you make; it’s your opportunity to make a difference.

Back to the Global Macro Grind…

The Russell 2000 clocked another all-time closing high yesterday of 1054 (+24.1% YTD) as mostly every growth stock that beats toned down expectations rips to new YTD highs. Slow growth investor T-Bonds were down (again). This remains a growth investor’s market.

Growth, growth, growth – if you can find it, buy it – that’s not just a progressive message that stands in stark contrast to the fear-mongering one that is getting pummeled (VIX -29% YTD), it’s a good way to live your life. In order to grow, you need to embrace change.

What’s interesting about being long growth is that not all “growth” investors have actually agreed with it, yet. That said, it’s important to remember that we’re all storytellers – and the market doesn’t care about our own individual versions of the story.

Here’s the non-fictional account of what we call growth “Style Factors” for 2013 YTD:

- Top 25% EPS Growth Stocks (SP500) = +23.8% YTD

- Low Dividend Yield (growth) Stocks = +26.4% YTD

- High Short Interest Stocks = +22.6% YTD

In other words, if you are long high-beta stocks that A) look “expensive” B) have high short interest and C) deliver better than “expected” growth results – boom! Non-cheater alpha is yours to keep.

Not only are non-obvious growth Style Factors beating the SP500’s YTD return of +18.5%, so is growth as a sector-style within the SP500:

- Consumer Discretionary Sector ETF (XLY) = +25.1% YTD

- Utilities Sector ETF (XLU) = +12.3% YTD

That’s a massive (and widening) performance spread that looks a lot like being long US Stocks vs US Treasury Bonds.

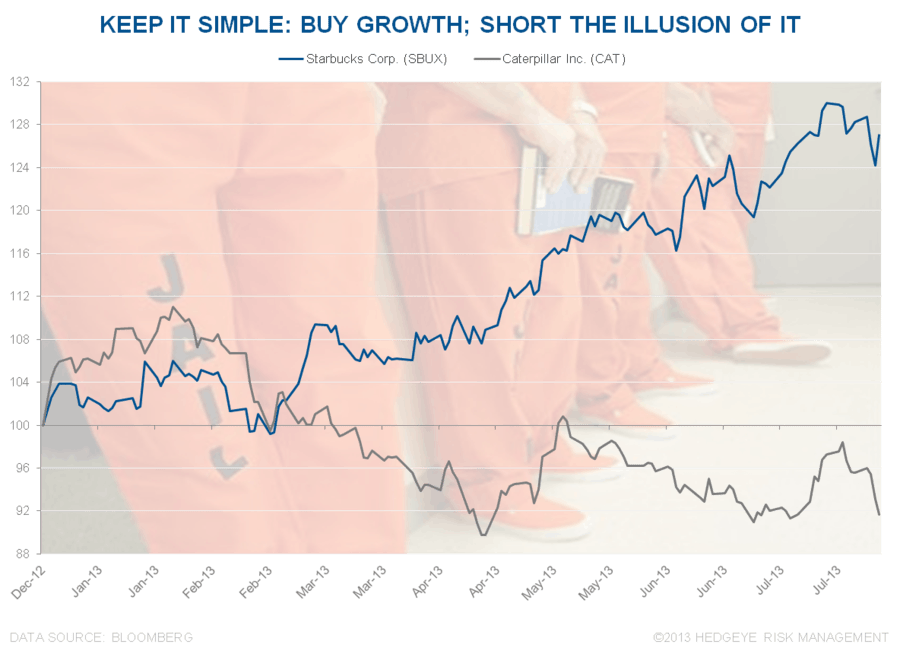

And there’s more alpha where that came from. Whether it was Visa (V), Facebook (FB), or long-time Hedgeye favorite Starbucks (SBUX) this week, Mr. Market is telling you that you don’t need to cheat to win in this business. You need to pay up for the growth that you can find.

While this doesn’t always make sense to people until they make the amount of mistakes I have, the other side of being long this growth rip is shorting “value” stocks that look “cheap” (if you use the wrong numbers).

That’s CAT.

So all in, what we have here is an opportunity to separate the pretenders from the pros. This is the new old school - roll up your sleeves and do your own work. No need for insider information. Just have the confidence and humility to let Mr. Market tell you all you need to know.

Math is our edge. It’s black and white. The opportunity to capitalize on leadership principles and a repeatable process has never been so bright.

Our immediate-term Risk Ranges are now:

10yr Yield 2.47-2.65%

SPX 1675-1700

VIX 11.82-13.37

USD 81.54-82.57

Yen 98.41-100.78

Gold 1244-1359

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer