The big move in Japan this week definitely caught me off guard.

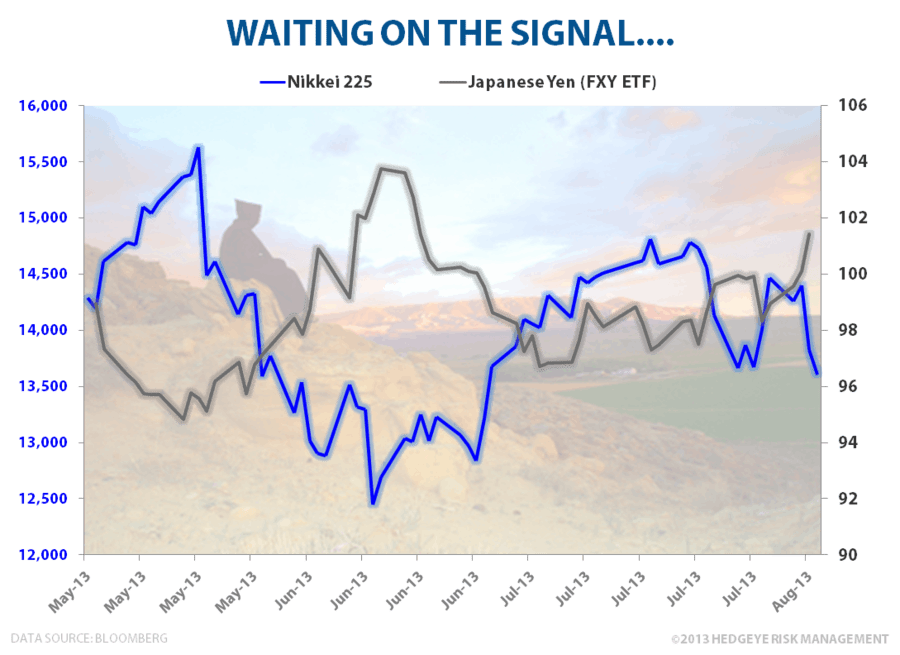

Now the question becomes: Are we are past the maximum, short-term "Yen short/Nikkei long" pain? At 96.16, Yen (vs USD) is 3.1 standard deviations oversold in my model. No, that doesn’t happen very often.

Meanwhile, the Nikkei is holding TREND support of 13,445. So yes, I am tempted to buy back the DXJ on that. Waiting on the signal.

(Editor's note: This post is a brief excerpt from Hedgeye CEO Keith McCullough's morning research. For more information on how you can sign up and start harnessing the Hedgeye team's award-winning, proprietary research, please click here.)