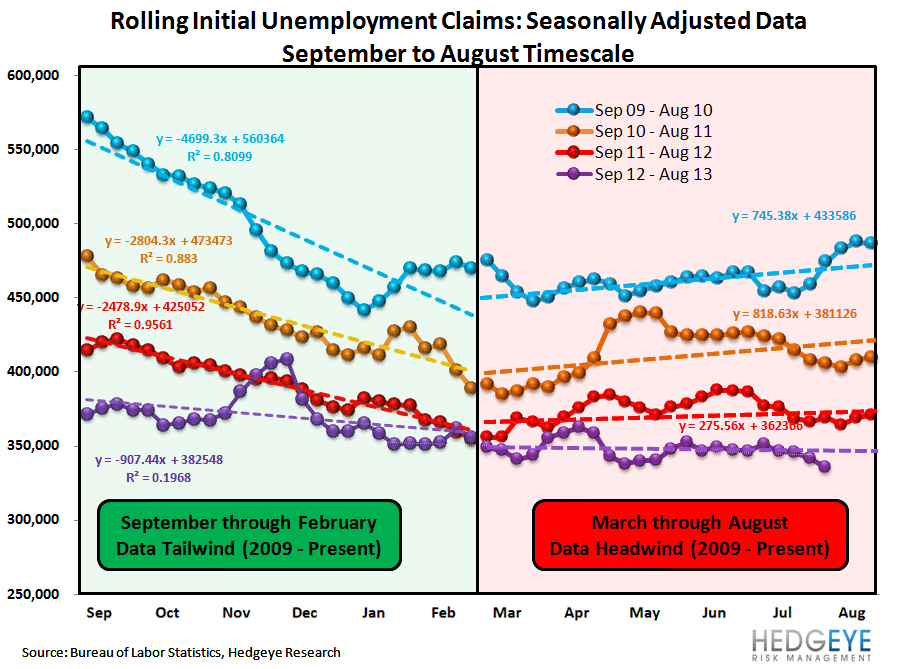

Less Than 5% of the Time

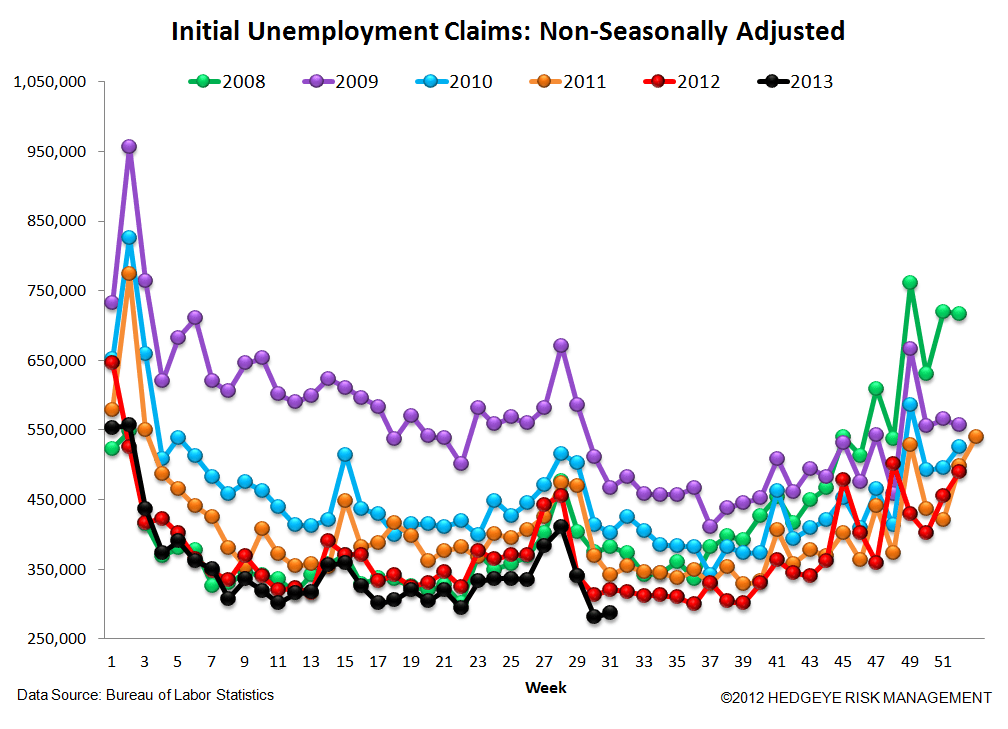

Labor market data continues to come up roses as the most recent non-seasonally adjusted initial jobless claims came in 10.5% lower than a year ago. That's a slight improvement vs. the previous week, which saw a 10.1% improvement, and is a bit ahead of the average for the last 12 weeks, which is -8.8%. Giving exception to the single anomalous data-point 3 weeks ago (-0.2%), we find the average over the last 12 weeks has been a YoY improvement of 9.7%, extraordinary for this point in the cycle. This rate of improvement is understated by the seasonally-adjusted data, which also looks quite good. Based on our analysis of the seasonality distortions shifting from headwind to tailwind from September through February, we think the SA number, with no underlying fundamental improvement, will shift from 333k to around 305-310k. There is, however, clear underlying fundamental improvement, so we wouldn't be surprised to see a 2-handle on the SA initial jobless claims reading by late 1Q14. For perspective on just how strong that is, historically, since 1975 we've observed 2-handles in 2Q06, 2H99, 4Q88, 3Q78, or less than 5% of the time. Specifically, 93 of the last 2,014 weeks have seen sub-300,000 SA IC weekly prints.

Our favorite ways to play a stronger-than-realized improvement in the labor market remain financials with levered exposure to home price recoveries as well as unsecured lenders. Capital One (COF) and Bank of America (BAC) remain two of our favorite ideas on the long side.

The Data

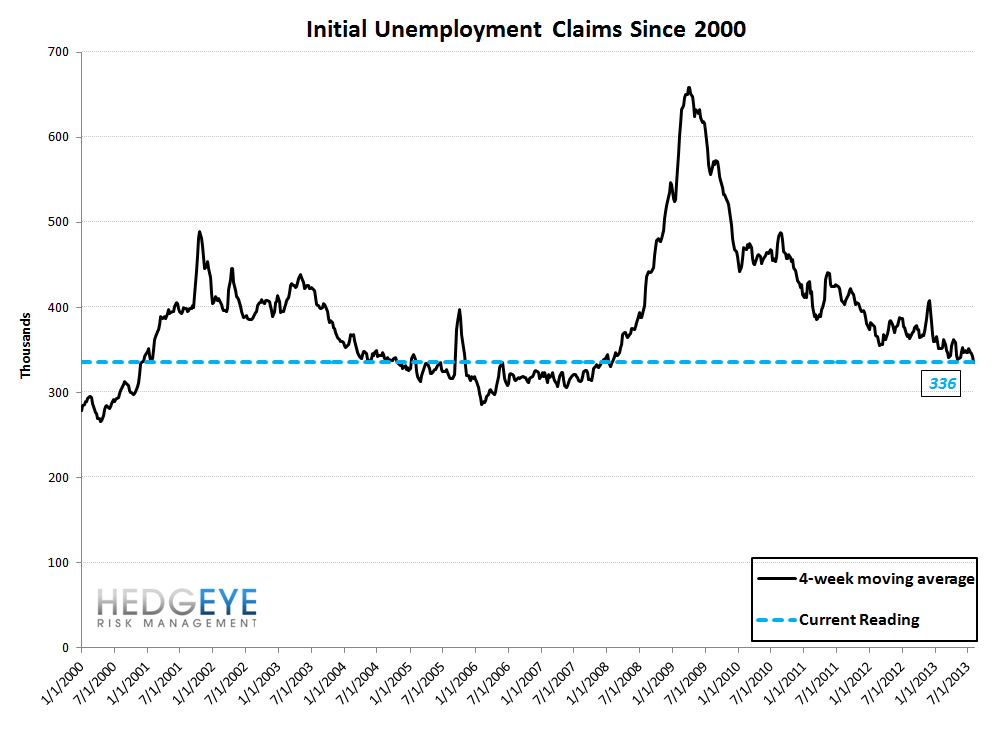

Prior to revision, initial jobless claims rose 7k to 333k from 326k WoW, as the prior week's number was revised up by 2k to 328k.

The headline (unrevised) number shows claims were higher by 5k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -6.25k WoW to 335.5k.

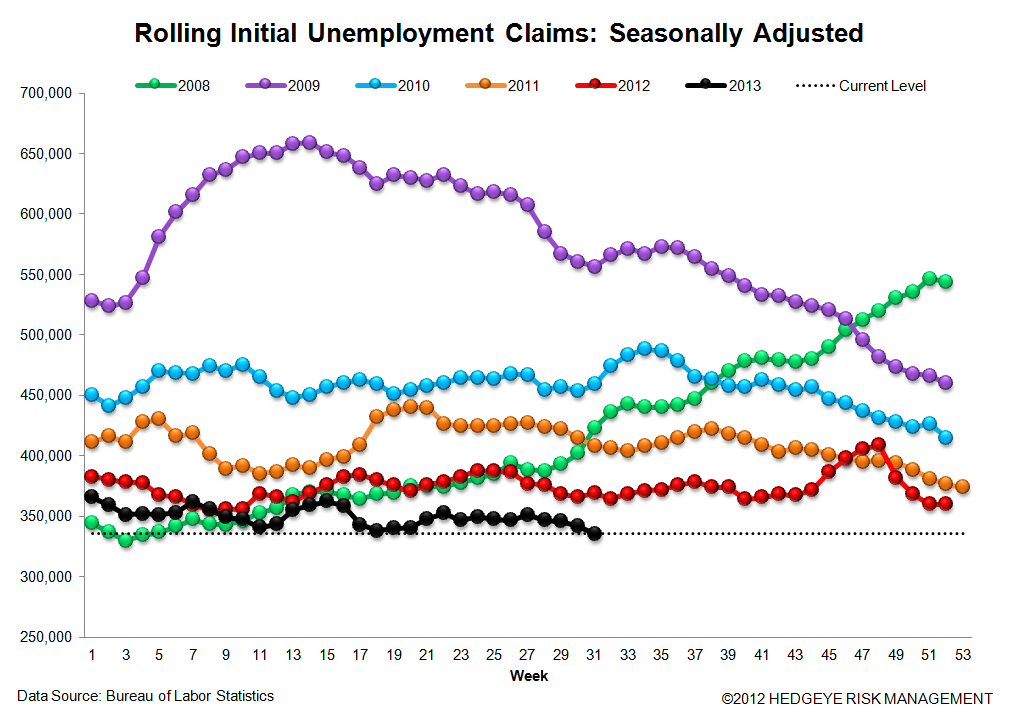

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -7.8% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -8.8%

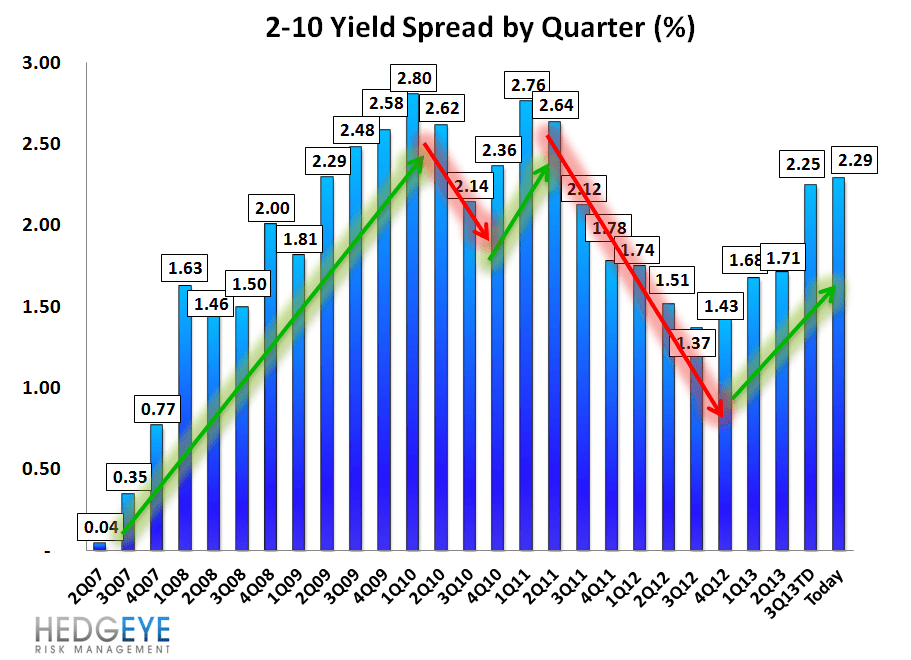

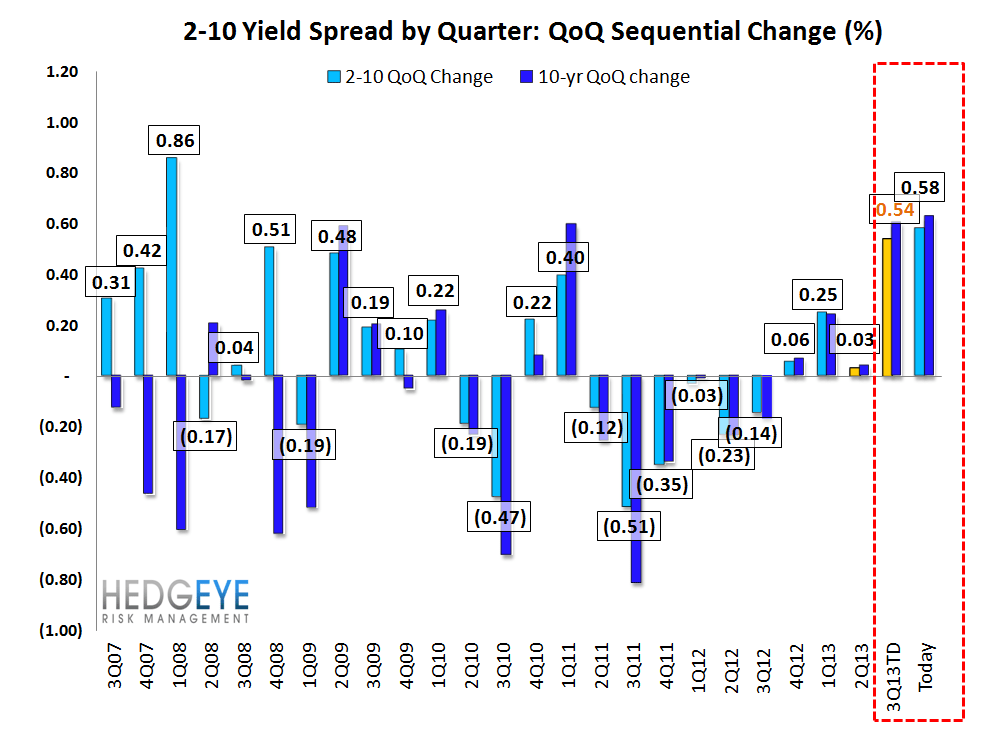

Yield Spreads

The 2-10 spread rose 2 basis points WoW to 229 bps. 3Q13TD, the 2-10 spread is averaging 225 bps, which is higher by 54 bps relative to 2Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT