Key Takeaways:

The most recent release of the weekly ICI mutual fund survey data continues to be supportive of our thesis of a reallocation from fixed income into equities. For the week ending July 31st, both taxable and tax-free fixed income had substantial outflows for the week with the equity category experiencing a modest inflow.

Weekly ICI Survey Reported:

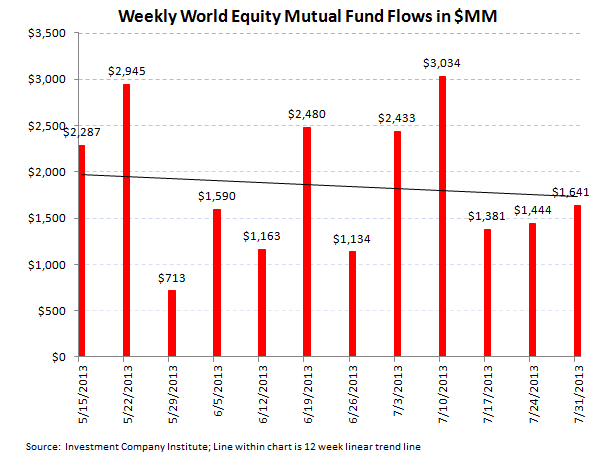

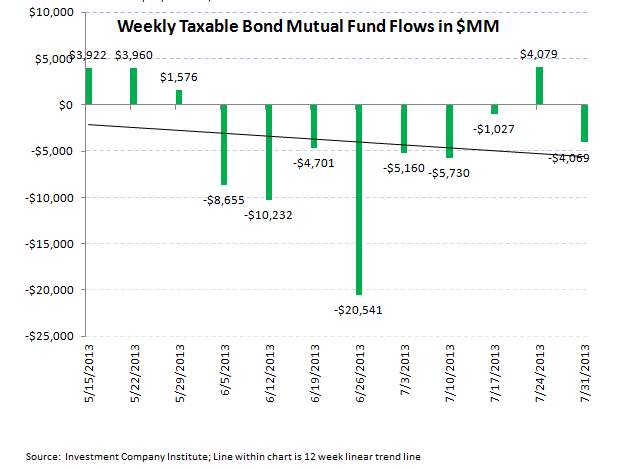

The Investment Company Institute (ICI) has just reported its weekly mutual fund flow data for the week ended July 31st. The survey which encompasses 95% of all open ended mutual funds relayed a continuation of an emerging preference for equity funds which had another inflow during the week at the expense of fixed income mutual funds, which had outflows across the board. For the 7 days ending July 31st, all equity fund products took in $714 million, which was an aggregation of a $1.6 billion inflow into world equity funds, net of an outflow of $926 million in domestic stock funds. Conversely, the fixed income side of the ledger continues to be a slippery slope with outflows of $4.0 billion in the taxable bond category for the 7 day period and an accelerating outflow for tax-free or municipal bonds of $2.8 billion. The hybrid category, the 5th and last survey reported by the ICI, relayed another strong inflow for funds which combine both equity and fixed income products of $1.7 billion. The charts below reflect the data reported overnight by the ICI and also display the past 12 weeks of fund flow information for reference.

The most recent weekly trends are representative of the emerging trends that we are forecasting will accelerate and replace the most recent cycle of equity fund outflows sourcing fixed income related inflows. This was the pattern in the last rotation between asset classes in 2008 and 2009, where equity fund draw downs were first parked into money funds before a re-allocation into fixed income throughout '08 and '09. To put into context the slow shift from out-sized stock fund flows into incremental equity fund demand, the running year-to-date weekly average money flow for equity products is now a $2.7 billion inflow, a reversal from the 2012 weekly average of a $2.8 billion outflow. Thus investors are slowly voting with their capital as to which asset class is becoming more appealing. Conversely, the all bond category outflow this week of $6.9 billion is an acceleration from the 2013 weekly average inflow of $696 million and a substantial drop from 2012's $5.8 billion weekly inflow average. As we continue to discount the relatively higher risks for fixed income versus equities, we expect these bond fund outflows to be persistent.

Total Asset Flows including ETFs is also sporting better trends:

While the ICI survey is useful for the mutual fund complex only, a more comprehensive money flow view would have to incorporate the emerging exchange traded fund (ETF) vehicle. While ETFs are still only 13% of the mutual fund industry, their higher growth rate against funds continues to increase ETF market share and hence a comprehensive view of industry trends has to include this new asset management product.

Using publicly available information from ETF sponsors on creation units outstanding and net asset value (NAVs), we are able to also bolt on the money flow trends in exchange traded funds to the ICI weekly survey. We have aggregated this ETF fund flow data using the ICI date convention of Wednesday to Wednesday of the week prior and present this data as a more detailed information set than the ICI survey alone.

This "total" money flow information (both ICI fund survey and our customized ETF data collection) is projecting a similar asset allocation shift from fixed income to equities. For the week ending July 31st, total fund flow broke out to a $6.6 billion inflow for equities which disaggregated into the $714 million total equity fund inflow from ICI and $5.9 billion from equity based ETFs. On the fixed income side, the $6.8 billion mutual fund outflow was softened by $500 million in bond ETF inflows to net to a $6.3 billion outflow for fixed income.

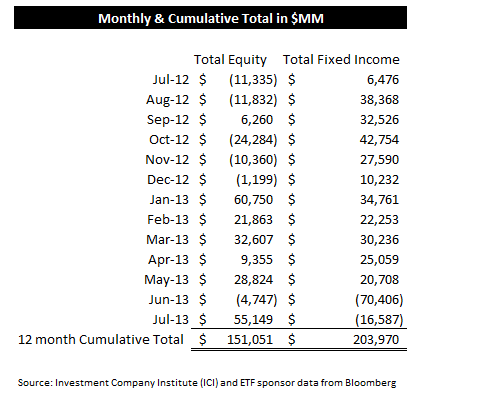

From a broader perspective, the months of June and July also paint a trend of re-allocation amongst stocks and fixed income. Again aggregating both mutual fund flow and ETF flows, June marked a massive $70 billion out of bond products. This has been followed by a $16 billion draw down in July. Equities fared relatively better than fixed income over the same time period experiencing just a $4.7 billion outflow in June which has been washed out by a large $55.1 billion subscription in July. While the cumulative trailing twelve month total flow aggregates still favor fixed income at $203 billion in new flow versus $151 billion to equity products, we estimate the more recent trends will be more reflective of the rest of '13 and also 2014.

Slowly Turning the Aircraft Carrier...Long Term Trends Slowly Unwinding:

The aforementioned secular trends of equity outflows sourcing new fixed income subscriptions over the past 5 years are slowly reversing which can be seen in running year-to-date tallies. Within the ICI mutual fund landscape, all equity funds including domestic equity and world equity are now totaling over $92 billion in year-to-date inflows incorporating this most recent ICI survey. This is a substantial reversal from the $153 billion outflow in 2012 and this year threatens to be the first positive year for mutual fund flow since 2007. For fixed income, ICI mutual fund trends have slowed drastically year-to-date. For the first 7 months of '13, both taxable and tax free products are now totaling just $10 billion in year-to-date inflow, a far cry from the over $300 billion that the fund class took in last year in 2012. Bond fund flow peaked in 2009 with the $379 billion that was allocated by investors to the asset class coming out of the credit crisis.

The year-to-date ETF trends are in a similar vein to year-to-date mutual fund trends. Equity ETFs are working on a record year for inflow with $113 billion having already been allocated to the asset class by investors. At this pace 2013 would vastly eclipse the record year of 2008 which drew in $127 billion in equity ETF subscriptions. On the bond ETF side, 2013 has generated $16 billion in new investor monies, a deceleration thus far in the $56 billion in fixed income ETFs taken in last year which appears at this point to be the high water mark for bond ETF flow.

The most recent weekly survey from the ICI is supportive of our recent asset management sector launch which outlined our estimate that significant risks are inherent in the U.S. bond market which will spur an invest-able asset allocation shift from fixed income into equities. Fixed income money flow has had an out-sized historical run with the past 8 years aggregating over $1 trillion in new money flow which we estimate has put in a top in U.S. bond returns assisted by the unprecedented fixed income liquidity programs from the U.S. central bank. Conversely, equity money flow has been decidedly negative for 5 years which has resulted in over a $500 billion redemption from the asset class. However, with stocks working on their 4th positive year of returns in 5, and with equities a healthier relative asset class to fixed income, we estimate a reversal in equity outflows which will benefit leading equity asset managers at the expense of managers more dependent on fixed income which is experiencing slowing fund flow subscriptions and eventual fund outflows.

Our Asset Management launch piece is enclosed here:

http://docs.hedgeye.com/HE_F_AssetMgmt_launch.pdf

Our detailed Powerpoint presentation is enclosed here:

http://docs.hedgeye.com/DomesticAssetManagementCoverage_07.29.13.pdf

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA