MCD remains on the HEDGEYE best ideas list as a SHORT.

In order for McDonald’s to generate sustainable revenue and operating growth consistent with the company’s long-term goals, we believe MCD must make changes to its core U.S. store operations.

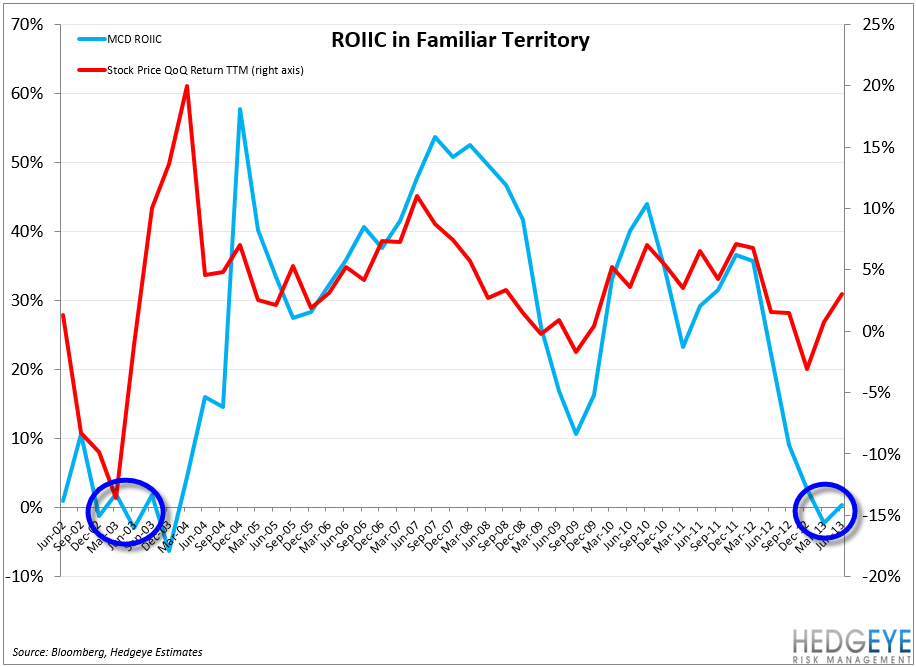

ROIIC, We Meet Again

Over the years, we have built a Restaurant Dashboard that tracks a number of companies and industry metrics, allowing us to consistently and constantly gauge investor sentiment and company performance. While some metrics fall in and out of favor over time, one metric that has outlasted the test of time for every company is one of our favorites – Return on Incremental Invested Capital (ROIIC).

Depicted in the chart below, MCD’s ROIIC has returned to levels not seen since 2002-2003, which was a period of underperformance and called for major restructuring. We have been very critical of the direction MCD is heading since the end of 1Q13 and remain in that camp following the release of 2Q13 results.

Issues on the Horizon

Stepping back and reviewing 2Q13 results, the only solace management offered shareholders that the underperformance would not continue was two-fold, and in our opinion, relatively weak:

- “Throughout McDonald’s history, we’ve effectively grown both the top and the bottom lines to varying degrees across a variety of economic and competitive cycles.”

- “We have an iconic brand, an outstanding system of owners/operators, suppliers and employees, and superb real estate locations in nearly every market around.”

While we are in agreement with the above, these comments neglect several issues that call for immediate attention:

- Evidenced by an increasing number of negative articles on the company, the franchise base is very unhappy with senior management.

- A declining category is no plausible excuse, let alone a cause, for the current issues the company is facing. We don’t see Wendy’s or Taco Bell complaining about a declining category.

- The competition in the QSR landscape has regrouped and MCD appears to be standing still.

This raises the question: How did MCD get to the point where ROIIC is currently at levels not seen since 2002-2003? Perhaps the answer is best expressed by drawing on an analogy to Starbucks. Using this analogy, we ultimately find that MCD needs to readjust its basic store operations.

A Tale of Two

Breaking down the business models:

- MCD is a food destination first and a beverage destination second.

- SBUX is a beverage destination first and a food destination second.

Both companies have struggled in their attempts to diversify away from their respective core competencies. In the past, an over-emphasis on anything other than the core business has led to the underperformance of the core. We recall a time when SBUX attempted to sell books and compact discs in an effort to diversify and these efforts ended in an unmitigated disaster. We believe that MCD has taken the “McCafe” strategy too far too fast, while ignoring the underlying trends in the initial test markets. For more on this thought, please review our post “MCD: An Espresso-Based Conspiracy Theory” penned earlier this year. In short, attempting to sell Latte’s and blended ice drinks is no easy task and is obfuscating the brand image, while diverting resources away from the core business.

Another MCD versus SBUX comparison:

- SBUX believed that introducing TurboChef ovens to its stores would improve the consumer perception of their food. We view the purchase of La Boulange as proof that this strategy was ineffective.

- MCD believed that introducing espresso machines and blenders to its stores would help make it a beverage destination. But, in the end, consumers do not view MCD as a beverage destination, as the company has struggled to compete with SBUX and DNKN on quality.

The bottom line for us is simple: MCD needs to take a step back from their aggressive McCafe beverage strategy in the U.S. As outsiders, it seems clear to us that the expensive McCafe equipment has simply complicated the back of the house operations. Clearly, operators are unhappy and many of the one’s we have spoken to have indicated that it now costs more to “plug-in” the espresso machine than the sales they generate from it.

McDonald’s and the franchisee community now find themselves in a precarious situation as they face a new and growing problem. This new equipment has failed to generate enough revenues to validate its presence in stores. And now, many of these machines are approaching, or already surpassed, their fifth year in existence, meaning that the majority of them will either need to be repaired or replaced. At this point in time, management must ask themselves some very important questions:

- Will the franchisees be willing to continue to invest in an expensive machine that slows the speed of service and does not generate incremental profitability?

- What percentage of McDonald’s marketing and promotion dollars have been spent promoting beverages in 2013?

- Did the company achieve a worthwhile ROI on the aforementioned marketing dollars spent?

Back to the Basics

MCD has faced difficult sales comparisons for years (2005-2011), yet this has never stopped them from posting positive same-store sales. According to management, the new products are working thus far in 2013, but difficult comparisons are the reason for declining same-store sales. In our view, the new products are not working and operational throughput issues persist.

CMG and others are changing the landscape for fast food. In what we would take as positive news on the margin, MCD has acknowledged that it needs to do a better job attracting millenials with fresh ingredients and variety! Now, what changes in service style does MCD need and what will it cost? That’s something for management to figure out, what we can surmise is the premium wraps did not adequately convey that message to the intended audience.

MCD is in need of a period where they get back to the basics of serving fresh, prepared food. They can continue to pay lip service to being a beverage destination if they please, but the truth is they will likely never be able to compete against the concepts that successfully make a living serving beverages.

Is Thompson the Next Greenberg?

We’d be remiss to end the note without touching upon the disappointment of the dollar menu. As you may recall, selling food for $1 was a strategy that cost Jack Greenberg (ex-CEO of MCD) his job in 2002. Yet, the Dollar Menu was Don Thompson’s “go-to” move in 2012 through 2013, and it is turning in undesirable results. Will Don Thompson face the same fate as Jack Greenberg or will he accept the reality of the current situation and strive to reestablish the core business?

Howard Penney

Managing Director