My colleague, and Research Edge's Asian Strategist, Andrew Barber told me the other day that he had a dream that we would one day all be driving cars powered by natural gas. While Barber is a great analyst who has nailed China this year, he is also a man of ideas. As of now, cars powered by natural gas are just that, an idea. We neither have the vehicles to do this, nor the infrastructure in place to deliver the natural gas. With all things, though, there is a price.

Currently, the oil / gas ratio is suggesting that price may be near as we are at an extreme in the price differential between the two commodities. In fact, the oil / gas ratio (the price of one barrel of oil divided by the price of one BTU of natural gas) is currently nearing 18x, which is 9-year high.

According to many experts, a barrel of oil contains roughly 6 BTUs of energy equivalence. On that basis, natural gas should be trading at ~$10.80 per BTU. Based on its current price of $3.93, natural gas is trading at just 36% of energy equivalent price. In theory, if oil stayed at its current price and natural gas reverted to its energy equivalency value, there would be ~175% upside to natural gas. As we know, in the real world arbitrage opportunities happen for a reason and the theoretical energy equivalency value is just that, theoretical.

Our competitor Dennis Gartman uses many ratios to justify his positions. On most, we would vehemently deny that there is a fundamental underpinning (Gold versus Agriculture as an example). With oil and natural gas, on the other hand, there is clearly some fundamental basis to consider this ratio since both oil and natural gas have an energy value that can be measured.

Some analysts suggest that on the industrial demand side, there is 5 - 10% overlap in oil and natural gas, which can be switched at different price levels. While this may be accurate, the most relevant data point relates to transportation. As the EIA reported last month in their year end natural gas review:

"Natural gas for vehicle fuel has increased over the past several years but remains at less than 1 percent of the total."

Until we see this number move meaningfully, it will be hard to argue that oil and gas are interchangeable from a usage perspective.

Investors who use history as a guide would suggest that either oil is over priced or natural gas is under priced. In the short term, they could both be correct. Longer term, the reality is more likely that we have entered an era of cheap natural gas and relatively expensive oil. Most importantly, oil has quantifiable supply constraints and burgeoning demand from emerging economies, most specifically China, while the natural gas market is flush with supply domestically and abroad.

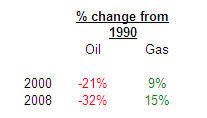

We can see this change in growth of domestic supply of both commodities. In the simple table below, we have outlined the growth in domestic oil product and gas production in 2008 and 2000 versus 1990, with 1990 as the reference year. As we can see, on domestic basis, the market for oil has tightened dramatically. Since 1990 oil production on an annual basis in the U.S. is down -32%, while natural gas production is up 15%.

While the oil / gas ratio is a relevant input for a fundamental view of the two commodities, until interchangeability becomes more prevalent between the two commodities, the history of the ratio is probably not the best guide to its future.

Daryl G. Jones

Managing Director