TODAY’S S&P 500 SET-UP – August 6, 2013

As we look at today's setup for the S&P 500, the range is 40 points or 1.94% downside to 1674 and 0.40% upside to 1714.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.34 from 2.33

- VIX closed at 11.84 1 day percent change of -1.17%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC retail sales

- 8:30am: Trade Deficit, June, est. -$43.2b (prior -$45b)

- 8:55am: Redbook weekly retail sale

- 10am: IBD/TIPP Eco Optimism, Aug., est. 47.5 (prior 47.1)

- 10am: JOLTs Job Openings, June, est. 3.895m (prior 3.828m)

- 11am: Fed to buy $4.75b-$5.75b debt in 2018-2019 sector

- 11:30am: U.S. to sell 4W bills

- 1pm: U.S. to sell $32b 3Y notes

- 4:30pm: API crude, oil product inventories

GOVERNMENT:

- President Obama travels to Phoenix to give remarks on middle class homeownership, then to Burbank, Calif., where he’ll appear on “The Tonight Show with Jay Leno”

- FDA Dep. Commissioner Michael Taylor delivers remarks at Institute of Medicine discussion of caffeine in dietary supplements, other foods, 9am

WHAT TO WATCH:

- Australia cuts rate to record 2.5% as currency strengthens

- Amazon.com’s Jeff Bezos to buy Washington Post for $250m

- IBM furloughs U.S. workers of hardware group to cut costs

- Sony rejects Loeb push to sell part of entertainment unit

- Time Warner Cable makes a-la-carte proposal in CBS dispute

- Icahn bought 4m Dell shrs on Aug. 1; holds 156.5m shares

- Revlon to purchase Colomer Group from CVC for $660m

- Paulson & Co. said to gain in July as recovery fund recoups loss

- FBI finds vulnerabilities in mkt-moving govt. reports: WSJ

- Italian contraction slows as recession lasts record 2 yrs

EARNINGS:

AM EARNS:

- Aircastle (AYR) 7:30am, $0.33

- American Realty Capital Properties (ARCP) 6:25am, $0.19

- Archer-Daniels-Midland (ADM) 7am, $0.44

- Arcos Dorados (ARCO) 8am, $0.56

- Ares Capital (ARCC) 8am, $0.39

- BreitBurn Energy Partners LP (BBEP) 8am, $0.13

- Charter Communications (CHTR) 8am, $0.31

- Cinemark Holdings (CNK) 6am, $0.52

- Cognizant Technology Solutions (CTSH) 6am, $0.97

- CVS Caremark (CVS) 7am, $0.96

- Denbury Resources (DNR) 7:30am, $0.36

- Diebold (DBD) 8am, $0.27

- Dish Network (DISH) 6am, $0.53

- Dominion Resources (D) 7:30am, $0.65

- Emerson Electric (EMR) 6:30am, $0.98 - Preview

- FirstEnergy (FE) 8:25am, $0.54

- Fossil Group (FOSL) 6:55am, $0.93

- Harman International Industries (HAR) 8am, $0.86

- Health Care REIT (HCN) 7:30am, $0.92

- Henry Schein (HSIC) 6:51am, $1.23

- Hospitality Properties Trust (HPT) 7am, $0.75

- Inergy (NRGY) 7:45am, $0.05

- Inergy Midstream (NRGM) 7:45am, $0.10

- IntercontinentalExchange (ICE) 7:30am, $2.14

- International Flavors & Fragrances (IFF) 7am, $1.18

- Isis Pharmaceuticals (ISIS) 8:30am, $(0.23)

- Liberty Interactive (LINTA) 6:45am, $0.27

- Louisiana-Pacific Corp (LPX) 8am, $0.34

- MGM Resorts International (MGM) 8:30am, $0.01

- Michael Kors (KORS) 7am, $0.49

- Molson Coors Brewing (TAP) 7:30am, $1.39

- Nationstar Mortgage Holdings (NSM) 6:30am, $0.89

- Oaktree Capital Group (OAK) 8:30am, $1.62

- OfficeMax (OMX) 7am, $0.03

- Parker Hannifin Corp (PH) 7:30am, $1.96

- Regeneron Pharmaceuticals (REGN) 6:30am, $1.75 - Preview

- Rowan Cos Plc (RDC) 8am, $0.55

- Ryman Hospitality Properties (RHP) 8:30am, $0.78

- Saputo Inc (SAP CN) 11:59am, $0.73

- Scotts Miracle-Gro (SMG) 7am, $2.43

- Sempra Energy (SRE) 9am, $1.28

- Spectra Energy (SE) 6:30am, $0.32

- Spectra Energy Partners (SEP) 8am, $0.37

- Spirit Aerosystems Holdings (SPR) 7:30am, $0.50

- Starwood Property Trust (STWD) 7:30am, $0.47

- Tenet Healthcare (THC) 7:30am, $0.71

- Textainer Group Holdings (TGH) 9am, $0.95

- Tidewater Inc (TDW) 7:51am, $0.76

- TransDigm Group (TDG) 7am, $1.84

- Zoetis (ZTS) 7am, $0.36 – Preview

PM EARNS:

- Acadia Pharmaceuticals (ACAD) 4:01pm, $(0.09)

- Avis Budget Group (CAR) 4:15pm, $0.51

- BioMed Realty Trust (BMR) 4:47pm, $0.39

- CF Industries Holdings (CF) 4:05pm, $7.61 - Preview

- CH Robinson Worldwide (CHRW) 4:15pm, $0.74

- Computer Sciences (CSC) 4:15pm, $0.67

- DaVita HealthCare Partners (DVA) 4:01pm, $1.84

- DigitalGlobe Inc (DGI) 4pm, $(0.26)

- EOG Resources (EOG) 5:05pm, $1.73

- Exelixis (EXEL) 4:15pm, $(0.30)

- First Solar (FSLR) 4:02pm, $0.53

- Genpact (G) 4pm, $0.25

- Gulfport Energy Corp (GPOR) 4pm, $0.13

- Jazz Pharmaceuticals (JAZZ) 4:01pm, $1.51

- Live Nation Entertainment (LYV) 4:04pm, $0.07

- Marathon Oil Corp (MRO) 5:26pm, $0.71

- Nuance Communications (NUAN) 4:01pm, $0.32

- Oasis Petroleum (OAS) 4:30pm, $0.60

- RLJ Lodging Trust (RLJ) 4:30pm, $0.58

- Rosetta Resources (ROSE) 4pm, $0.97

- SandRidge Energy (SD) 4:05pm, $(0.04)

- Sotheby’s (BID) 4pm, $1.37

- Twenty-First Century Fox (FOXA) 4pm, $0.35 - Preview

- Two Harbors Investment (TWO) 4:05pm, $0.31

- Vivus (VVUS) 4pm, $(0.41) - Preview

- Walt Disney (DIS) 4:15pm, $1.01 - Preview

- Zillow (Z) 4:02pm, $(0.11)

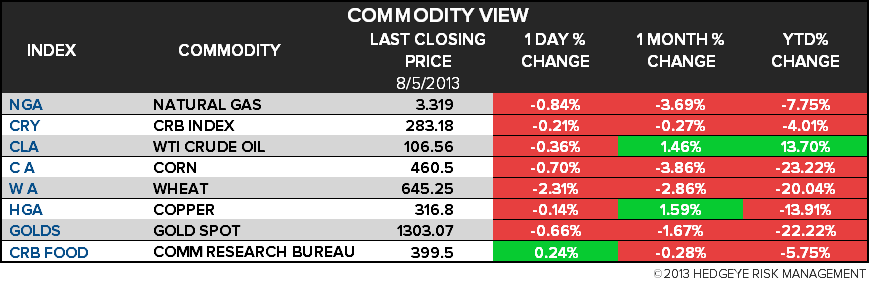

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- China’s Gold Imports From Hong Kong Decline as Demand Slows

- p Commodities Market, Industry News »

- Palladium Shortages Spur Bullish Hedge-Fund Wagers: Commodities

- Gold Slides Below $1,300 as Investors Weigh Stimulus Outlook

- Palm Inventories in Malaysia Seen Staying at Lowest in Two Years

- Copper Rises as German Factory Orders Stoke Rebound Speculation

- Tanker-Rate Slump Signals Retreat in U.S. Oil Imports: Freight

- Corn Declines to Lowest Since 2010 on U.S. Crop Progress Report

- Tin Backwardation Widens as Top Supplier Indonesia Curbs Exports

- China to Sell 500,000 Tons of Soybeans in Auctions This Week

- BullionVault Survey Says 37% of Buyers Kept Assets Over Year

- Italian Oil May Flow as Offshore Drilling Ban Ends: Bull Case

- S. African Corn Trade Risks Staple-Food Supply: Chart of the Day

- Coal at Risk as Global Lenders Drop Financing on Climate: Energy

- Gold to Gain as Output Languishes on Spending Cuts, WGC Says

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team