This note was originally published July 24, 2013 at 13:11 in Restaurants

We remain bullish on Starbucks at current levels.

Despite the stock trading at the high end of its historical consensus forward earnings and cash flow multiples, we believe there is more upside in store. The bullish factors we are focused on include rapid unit growth in China, expansion into new segments of the global food and beverage industry and a commodity tailwind that appears to be getting stronger.

There is still significant leverage in the SBUX business model. In 3Q13, SBUX is estimated to report 23.3% EPS growth ($0.53) on 12.9% revenue growth. In 2Q13, the company reported 27.5% EPS growth ($0.48) on 11.3% revenue growth.

One of the biggest risks to SBUX is sentiment, as SBUX is currently the highest ranked stock in the Hedgeye Sentiment Monitor. In 2Q13 SBUX raised its full-year EPS guidance to a range of $2.12 to $2.18. With sentiment high and expectations likely baked into estimates, it is difficult to envision a significant upside surprise in 3Q13 earnings.

Short-term trades are difficult to call from a fundamental perspective, but the bullish long-term TAIL remains the best play in the restaurant space.

Sales Trends

Same-store sales are estimated to be 6.1%, -0.5% and 9.2% in the Americas, EMEA and China, respectively. All regions, barring EMEA, are expected to have slowed on a 2-year basis.

We suspect that the EMEA region will report a same-store sales number down 2-3% and will be one of the biggest disappointments of the quarter.

China is comparing against a significantly easier comparison (12%) in 3Q13 versus 2Q13 (18%). Having no edge on what the sales trends look like in China, we would suspect that there is risk to the downside due to the current macro fundamentals in China.

Consensus expectations for same-store sales in the Americas are at 6.1%, which would be a slight sequential improvement over the 6.0% reported in 2Q13. However, this would suggest the 2-year trend is slowing sequentially, by 40bps, to 6.6%. All told, Starbucks’ Americas business is one of the best positioned chains in the restaurant industry.

HEDGEYE – There are a number of initiatives under way that could drive additional traffic and check (technology, food and juice) and allow for above average sales momentum for the immediate-term.

Margins

Operating margins improved 180bps in 2Q13 and the expectations are for them to improve another 120bps in 3Q13. We suspect that the Americas will be the biggest driver of margin improvement, with operating leverage provided by the scale and synergies among digital, card, loyalty, mobile and social platforms.

HEDGEYE – We believe that the coffee tailwind will benefit SBUX for the next two fiscal years.

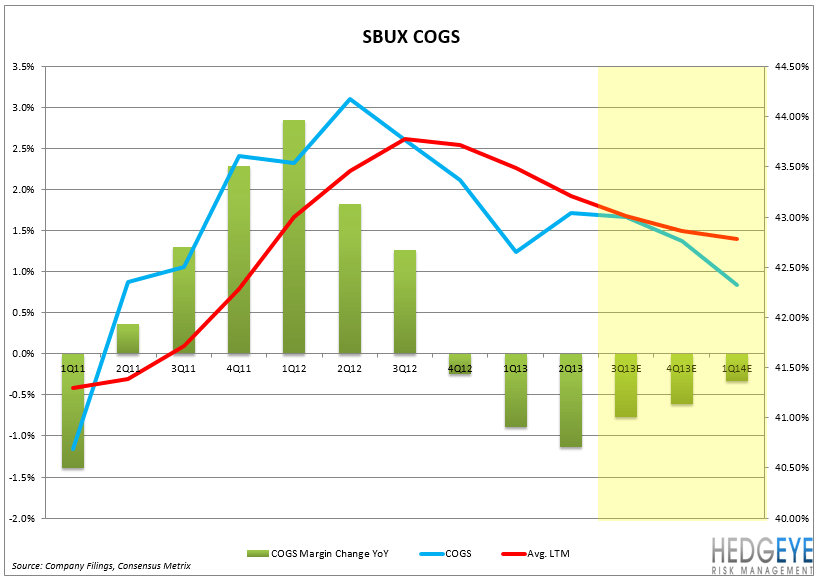

Food Cost Trends

The coffee tailwind is only three quarters old and we have no reason to believe SBUX will face any significant margin pressure from other commodities.

HEDGEYE – We suspect SBUX will realize a multiple year benefit from a decline in food costs.

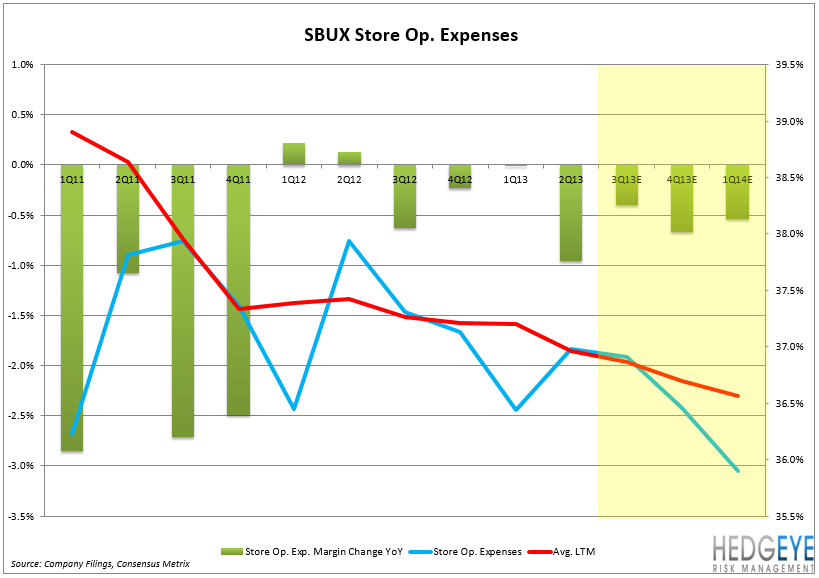

Store Operating Expenses

SBUX continues to leverage the store operating expense line. Strong top line momentum, in addition to an intense focus on store operations (labor and waste utilities management), is giving the company significant leverage on this line.

HEDGEYE – While nothing lasts forever, we believe that the strong traffic trends in the U.S. indicate that the customer experience remains very positive.

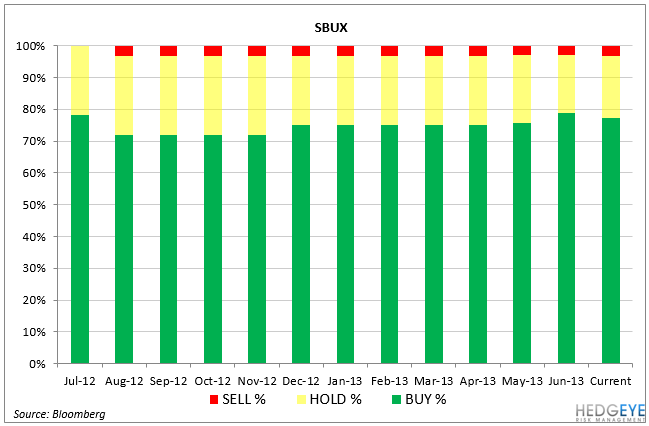

Sentiment

Highlighted in the chart below, 77.4% of analysts rate SBUX a Buy, 19.4% rate SBUX a Hold, and 3.2% rate SBUX a Sell. Sell-side sentiment regarding the stock remains very high. Further, short interest in the stock is only 1.18% of the float.

HEDGEYE – Sentiment is high, but where else can you turn to for global growth in the restaurant space?

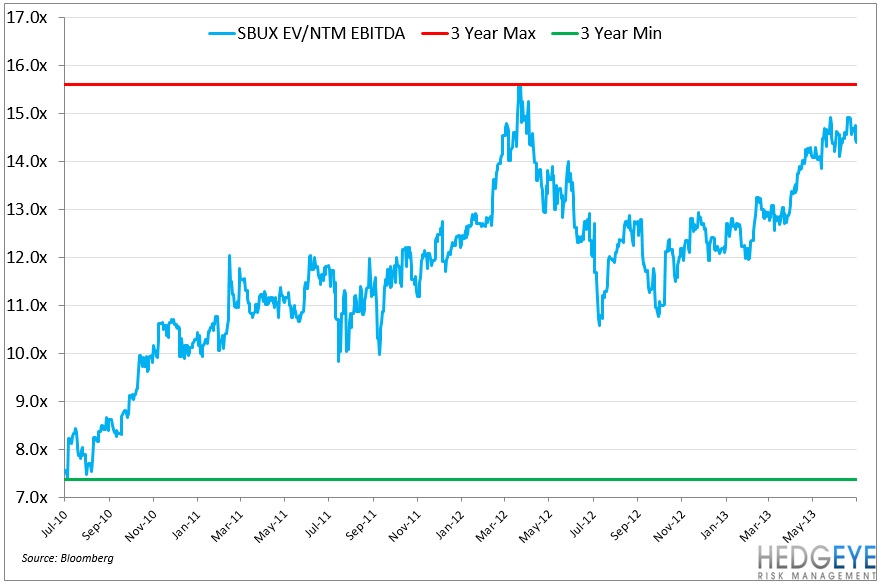

Valuation

At 15.0x EV/EBITDA SBUX is trading significantly above its QSR peer group trading at 12.4x EV/EBITDA. With YUM’s ongoing issues and MCD facing a secular downturn, it is not surprising that SBUX is trading at a premium multiple to both companies.

HEDGEYE – We suspect there could be a correction in valuation. However, the most important question remains: How much upside is there to EPS?

Howard Penney

Managing Director