This note was originally published at 8am on July 22, 2013 for Hedgeye subscribers.

“They cheat. You cheat. And yes, I also cheat from time to time.”

-Dan Ariely

This weekend I cracked open a behavioral psych book that is quite relevant to our profession this morning. The book is about how and why people cheat. It’s called The (Honest) Truth About Dishonesty, by the founder of The Center for Advanced Hindsight, Dan Ariely.

“In a nutshell, the central thesis is that our behavior is driven by two opposing motivations. On one hand, we want to view ourselves as honest, honorable people… on the other hand, we want to benefit from cheating and get as much money as possible.”

“This is where our amazing cognitive flexibility comes into play. Thanks to this human skill, as long as we cheat by only a little bit, we can benefit from cheating and still view ourselves as marvelous human beings.” (pg 27)

Back to the Global Macro Grind …

Now what happens if your internal view of cheating by a “little bit” ends up being viewed externally as cheating by a lot? Well, in our business, that might mean your firm gets a big fine and/or, alternatively, you get to slap on an orange-jump suit for a while.

With an oversupply of money managers, the pressure to perform in this profession is intense. I get that. That’s why people cheat. I’ve worked in more than enough hedge fund environments to know how some people define grey – and the definition is loose.

I also get what it means to build a family, firm, and culture with principles that are black and white. In the face of temptation, those principles need to stand like a rock. Ariely nails this in quoting Oscar Wilde (pg 28): “Morality, like art, means drawing a line somewhere.”

Enough about that. Our Macro edge isn’t inside info; it’s math – so let’s draw some TREND lines:

- SP500 = at the all-time highs, +18.7% YTD, with bullish intermediate-term TREND support = 1602

- Russell2000 = at the all-time highs, +23.7% YTD, bullish intermediate-term TREND support = 965

- US Dollar Index = -0.5% last week to $82.61 = +3.6% YTD with bullish TREND support = $81.63

- US Equity Volatility = -9.4% last week to 12.54 = -30.4% YTD with bearish TREND resistance = 18.98

- US Treasury Yield (10yr) = -10bps to 2.48% last week = +41% YTD with bullish TREND support = 2.21%

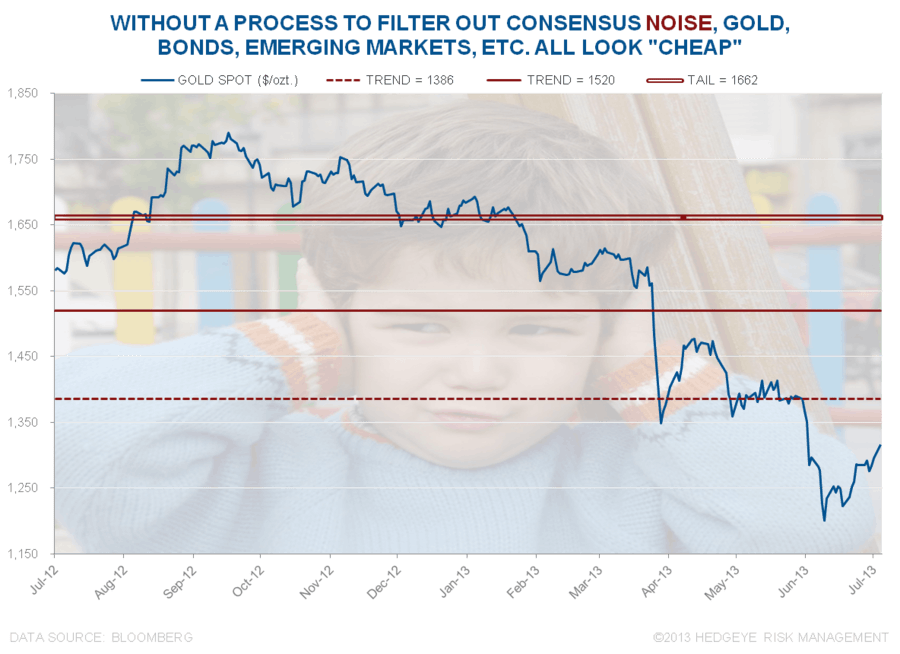

- Gold = +1.1% last week to $1294 = -23.3% YTD with intermediate-term TREND resistance = $1520

In other words, the 2013 Global Macro playbook didn’t require any cheating at all.

So far, from a US centric investor’s perspective at least, all you’ve needed to do was:

A) Short Fear (Gold, Bonds, Volatility) and

B) Buy Growth (High Beta, Low Yield, Growth Stocks)

It hasn’t been any more complicated than that.

What has been complicated has been understanding the storytelling of US stock market bears and Gold Bond bulls alike. With Gold, Bonds, and Yens bid up to lower-highs again this morning, there will be nothing new on that front either.

Another thing that isn’t new is “long-term” investors saying they don’t care about “all the short-term stuff” until all the short-term stuff is going the other way. This is where our immediate-term TRADE risk management duration comes in handy:

- Japanese Yen (vs USD) immediate-term TRADE support = 98.49

- Gold’s immediate-term TRADE resistance line = $1386

- 10yr US Treasury Yield’s immediate-term TRADE support = 2.45%

So, what would get me to start doubting our intermediate-term Macro view?

A) Every one of those TRADE lines being violated on a closing basis, then confirmed for more than three weeks

B) A fundamental research case that doesn’t lead me to believe in #StrongDollar #RatesRising #CommodityDeflation

What wouldn’t get me to change my views are things like:

- “Hearing Bernanke could do XXX this week”

- “Consensus is too bearish on Gold”

- Etc. etc.

You know, all the loosy goosy whispering stuff. There’s always someone cheating to aid and abet their position somewhere. It’s our job to absorb all the noise into our process and make the highest probability decisions we can make with public information.

Take for example the latest bull case on Gold (i.e. that people are too “bearish” on Gold, now that it’s crashing). Every man, woman, and child who is still long it is now talking about the “high short position” of a few weeks back…

Meanwhile this morning’s CFTC futures/options data showed consensus ramping the NET LONG Gold position by +56% last week to +55,535 net long contracts.

Ostensibly, the catalyst for buying Gold was what it’s been for both the YTD and the last ½ decade – Bernanke speaking. But, on Bernanke day (last Wednesday), Gold got clocked. The bull catalyst is consensus. Don’t let yourself cheat thinking about the intermediate-term TRENDs of #StrongDollar and #RisingRates otherwise.

Our immediate-term Risk Ranges are now:

UST 10yr 2.45-2.75%

SPX 1675-1702

VIX 12.20-14.53

USD 81.87-83.21

Yen 99.30-101.26

Gold 1241-1318

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer