Ideas Updates

The latest comments from our Sector Heads on their high-conviction stock ideas.

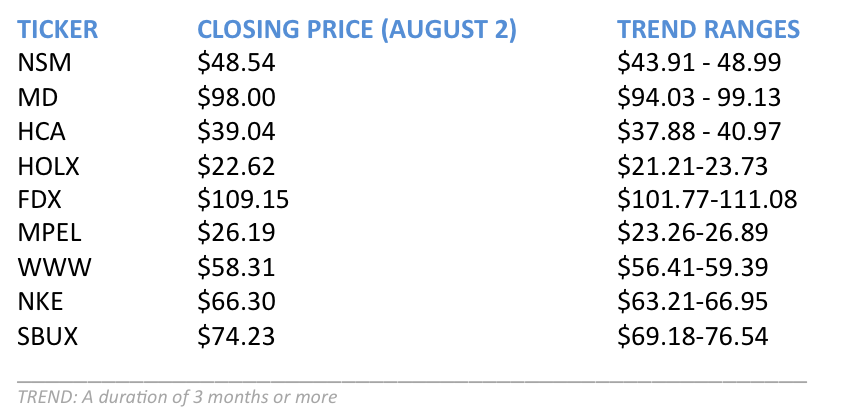

- NSM – Nationstar Mortgage shares have continued to perform well over the short-term, rising approximately 30% since the end of June (as of this writing). Most recently, the shares are responding favorably to competitor Ocwen Financial’s (OCN) 2Q earnings results, which came out on Thursday before the market open. OCN said two things that buttressed the investment case not just for OCN, but for the group including NSM. First, they said that a material driver of incremental margin improvement is the better-than-expected performance on the delinquency side of the business. This is attributable to both rapidly rising home prices and the improving labor market conditions and should be a benefit to NSM as well when they report earnings next week. Second, Ocwen indicated that the outlook for further MSR portfolio acquisitions is better than what they had thought in the prior quarter. Their pipeline of deals grew quarter-over-quarter in spite of closing a significant amount of new business in the quarter. This also bodes well for NSM, as they’re all competing for the same pipeline of business.

TRADE: In the short-term the market will trade NSM on the strength of its 2Q earnings, which will be released on Tuesday August 6. We currently expect that results will beat expectations.

TREND: Over the intermediate term, the stock will trade around announcements of MSR acquisition deals. We think NSM remains well positioned here, alongside Ocwen and Walters.

TAIL: In the long-term, there is still a tremendous opportunity for non-bank servicers like Nationstar to roll-up the servicing business. NSM is well positioned to be a prime beneficiary. We continue to think consensus earnings estimates remain too low for 2013/2014.

- MD – The market cares more about acquisitions here than organic volume growth. Mednax stock is performing very well on a solid earnings report, everywhere except patient day volume in their NICUs. We’re revisiting our work and making adjustments, but continue to love the story long term. MD generates most of its revenue growth from acquisitions. Based on the CEO’s comments during the call, opportunities for acquisitions continue to be robust.

- HCA – HCA Corp reported their preannounced Q2 results and did not change guidance for the year, although they did change how they will get there. Revenue will now be driven more by pricing than volume, although both are expected to accelerate in 2H13. Management also pushed out commenting on what the Affordable Care Act will mean to the company until February 2014, when they issue 2014 guidance. On the margin guiding to slower volume growth and pushing out a discussion of the ACA are marginal negatives. We’ll be running our survey of Obstetricians next week asking about pregnancy and delivery trends. We are also reviewing Birth forecasts. Real trends have not matched the Birth Regression forecast YTD, so we’re revisiting and expanding the original work. Anecdotally, we notice that traffic to www.babynames.com is accelerating, which may be a sign of improvement.

- HOLX – Exciting days are here for Hologic with the change of CEO and thoughts of “unlocking value” – despite no clearly articulated idea of what that could mean, not to mention stock price volatility that is not for the faint of heart. We’ll get earnings numbers on Monday, which were already preannounced. Qiagen announced weak results in their HPV testing line and spoke about “aggressive competitor pricing,” by which we assume they mean HOLX. Good for HOLX, bad for QGEN. We’re continuing to wait for news of a reimbursement code for 3D Tomo sometime later this year. It’s a big risk if a code isn’t forthcoming, but a homerun if it does. So far we can’t find anyone who believes a reimbursement code won’t be announced soon by CMS. Our OB/GYN survey on patient volumes, which showed acceleration into this month, will be another key data point in the coming week.

- FDX – FedEx shares were very strong this week in an unusual response to the news that FDX is not the target of a new Pershing Square fund. Our read: the rumored investment in FDX by Pershing Square, headed by activist investor Wunderkind Bill Ackman, brought significant attention to the upside potential for FDX shares associated with the Express restructuring. A positive response to “bad news” is probably a good sign. While reading the market’s tea leaves can be a dicey affair, it seems investors actually like the company’s prospects and would just as soon not have FDX become another ring in the Bill Ackman-Carl Icahn-Whoever-Else-Comes-Out-Of-The-Woodwork circus. Separately, TNT Express reported a disappointing quarter. As we indicated in our earlier analysis, we continue to think that this troubled Europe-focused transport would makes sense as an FDX acquisition target.

- MPEL – Gaming | Lodging | Leisure sector head Todd Jordan has no update on Melco Crown this week.

- WWW – This week kicks off the Outdoor Retailer trade show in Salt Lake City. Wolverine World Wide had a fairly large presence there with most of its brands, but particularly highlighted Merrill and Sperry. Merrill used the event to launch a new sub-brand called 'All-Out', which adds to its successful 'M-Connect' sub-brand. In effect, the new offering is an extension of its barefoot running product, but adds more cushioning into the equation to appeal to a wider audience. The price points are up to $120, which are rather steep, and will be impressive if they hold. Regardless, what we like about this is that the company is introducing new sub-brands and platforms as opposed to simply updating styles that existed last year. Simple updates give the illusion of growth, but never really result in better top-line. Companies need to come out with new product lines to keep the top line machine running. WWW is one of the few companies that “gets it” in this regard.

- NKE – Nike continues to gain share in footwear with both Nike and Brand Jordan, but it is NKE's apparel business that really has kicked into high gear in recent weeks. According to SportscanINFO, NKE's trailing 3-week apparel sales have consistently been in the 30-32% range, with a relatively stable average price point. That's not half bad when considering that the industry overall has been growing in the high single digits. Outstanding brand growth in the context of healthy category sales is just about all we could ask for.

- SBUX –Restaurants sector head Howard Penney has no update on Starbucks this week.

Macro Theme of the Week – Hedgeye’s Q3 Macro Themes, Part 3

Hedgeye gives you an edge you won’t find with the conventional financial professionals. Wall Street insists you’re either Bullish or Bearish. Hedgeye says that, at any given moment you’re either Bullish, or Bearish – or not Bullish enough, or not Bearish enough. That difference is not merely semantic. It goes to the heart of effective risk management – the point of departure for all successful investing. An old traders’ adage says, “Cut your losses – your winners will take care of themselves.” It’s all right not to be fully invested at any given moment. And it’s especially all right not to react in flat-out Bull/Bear mode to every day’s economic numbers.

Six-Shootin’ Ben

Last week’s unemployment claims caught markets off guard. This “deceleration hiccup” was greeted with panic by traders who saw it as a reversal of the trend building since the beginning of the year. Hedgeye says this is “the Trees vs. the Forest.” The market is a web of interconnections, not a scatter of single economic data points. In forestry this interconnectedness is called an Ecosystem. In the marketplace, we call it Economic Reflexivity, and we have seen it in action in the past three quarters as rising demand and spending have driven increases in employment and income – which in turn drives demand and spending – what economists call a Virtuous Cycle.

For those who object that unemployment isn’t “really” declining, because so many new jobs are not full time positions, note that any predictable and sustainable increase in income increases a person’s confidence – if only the confidence that one day they will transition to a “real” job. Importantly for consumption, even a 20-hour work week burnishes one’s credit, and improving creditworthiness has a positive, pro-cyclical impact on household net wealth and on what economists call Propensity to Spend (economists love the word “propensity,” it saves them having to make actual predictions, which are usually wrong.)

Case in point: this week’s reassertion of the positive trend in unemployment claims. Hedgeye remains bullish, even as frenetic Talking Heads were rending their garments (the NY Times’ blog headline reads: “US Adds 160,000 Jobs As Growth Remains Sluggish” http://www.nytimes.com/2013/08/03/business/economy/us-adds-162000-jobs-less-than-expected.html). Headline-chasers focus on the word “sluggish” – we’re focused on “growth,” with the line on the graph sloping positive across confidence, consumption, and credit.

Bernanke’s trigger-point now comes down to a single number: 6. His stated policy is to continue a variety of easy-money policies until unemployment falls to 6.5%, but any unemployment figure that has a “6” in front of it will be a wake-up call for the markets. Hedgeye’s Macro work indicates we should see a six handle on unemployment some time in the fourth quarter. Maybe not 6.5%, but reported unemployment should drop below 7% before year-end. Given the psychology of markets around round numbers, even a 6.8% unemployment number should trigger a surge in equities, accompanied by a drop in bond prices. We’re staying tuned to see whether “Six-Shootin’ Ben” Bernanke can plug the pips in a 6 at this distance.

#AsianContagion

Hedgeye’s Macro Themes for Q3 2013 are:

- #RatesRising

- #DebtDeflation

- #AsianContagion

In the last two weeks we featured the first two themes, #RatesRising and #DebtDeflation. This week we finish with #AsianContagion.

With the exception of Japan’s Nikkei index, every benchmark equity index across Asia’s markets is bearish on Hedgeye’s proprietary TREND measure (three months or less.)

Buoying Japan’s equities markets is the same Print-And-Spend policy that the Fed has used to pay off Wall Street, emanating from the same ivory tower that has paid untold trillions in bonuses to America’s failed bankers. Bernanke’s Princeton colleague Paul Krugman continues to exhort the Japanese to print, print, print their way to prosperity. One of Professor Krugman’s areas of expertise is the “liquidity trap,” when bond yields have sunk so low the market treats them like cash.

Krugman has written that Japan’s “lost decade,” the ten (or twenty, depending on who you ask) years following the collapse of Japan’s real estate bubble, was an extended liquidity trap. Like cockroaches dosed for generations with insecticides, in a liquidity trap the markets become immune to further cash injections. In Keynesian economics, the central bank’s job is to manage interest rates by adding or withdrawing liquidity – buying or selling bonds in the open market. Thus, in the liquidity trap government policy is incapable of stimulating economic growth.

Krugman has argued that Japan’s government hasn’t thrown enough cash into the system. With the Abe government firmly in place after last month’s elections, Krugman and his Keynesian buds have a ringside seat at a real live social experiment: will Abe-nomics, with its tsunami of banknotes, bail out Japan, or will the economy continue to lag?

Mind you, not everyone thinks Japan is lagging. Some observers point out that most Japanese kept their jobs during the “lost decades,” and that measured by standard of living, foreign trade, and the strength of the currency, Japan’s decades weren’t “lost” at all. This must also be seen through the lens of cultural values and expectations: Japanese value stability of employment more than the ability to climb the corporate ladder. Not everybody thinks like us.

Anyway, for the time being Shinzo Abe, the well-liked – and re-elected – Prime Minister, is printing Yen for all he’s worth, and Japan’s stock market is inflating like a giant balloon at the Macy’s Thanksgiving Day Parade. Abe’s winning the election could provide the political stability for much-needed economic reforms, but for now he’s mirroring America’s experiment in putting free money in bankers’ pockets. This policy should work well for their equities markets – until it doesn’t.

… but Asia…

But don’t look anywhere else in Asia for comfort. The rest of Asia’s policy makers are well and truly out of ammo as Asian economic growth has been nearly cut in half since 2010.

And if you weren’t worried about China, now would be a good time to start.

China has been the main driver of growth in the region, accounting for nearly 38% of all Asian GDP last year. Now the Chinese government is acknowledging that growth is in a downturn, publicly forecasting growth in the 7% range – well below the double digits of only three years ago.

China’s fixed capital formation grew like Topsy during the expansion years. But many of these were empty make-work projects designed only to inflate GDP, leaving the country awash in unused airports, unfinished roads and office buildings – and in bank loans for these projects with no revenues.

China’s banks are a loudly ticking time bomb. Their assets are bloated to an estimated 270% of GDP. A huge percentage of those “assets” are already in creditor limbo, having secured roads and bridges and tunnels and airports to Nowhere. China’s banks face a potential crisis as investment in major fixed asset projects declines amid eroding liquidity throughout the financial system.

Rising Rates should hit China’s markets too, pushing Asian rates higher. This will clobber the region’s capital-intensive economies, many of which expanded capacity specifically to serve Chinese demand. Rising rates – globally, but especially in the “safe haven” US Treasury market – coupled with a strong Dollar, should punish overvalued Asian currencies, sparking inflation, but in the context of economic decline. This spells economic trouble, and the potential for social unrest.

Senior analyst and keen-eyed Asia watcher Darius Dale says Chinese policy makers are starting to appear less concerned about a possible domestic asset price bubble. This could give them more flexibility in some kind of easy-money policy aimed at domestic stimulus. Any such policy move is likely to be slow to be implemented, and much slower to take effect. Dale cautions that massive debt rollovers generally slow economic growth by sucking liquidity out of the financial system, “diverting incremental credit from productive enterprises.” Perhaps more crucial is the impact on a fragile economy, which can hamper the creation of a stable economic base by diverting liquidity away from marginally productive business, or from temporarily unproductive ones that are merely trying to weather the economic storm.

Finally, any debt rollover China’s leaders may contemplate will almost surely not be offset by a significant increase in private savings. Without China to fuel the engine, Asia’s economic racecar looks to be in for a long pit stop.

Conclusion: 3Q2013 Macro Themes

Hedgeye has identified a triumvirate of global themes that could be a Perfect Storm for the patient investor. #RatesRising, #DebtDeflation, #AsianContagion. Stay with growth sectors in equities, says Hedgeye CEO McCullouogh, especially in the US – watch the slope of the curve to see where growth has taken root, don’t be distracted by the day-to-day numbers, and keep your eye out for a possible future buying opportunity in bonds.

Don’t fear deflation – it just makes stuff you want to buy cheaper. Or do you really think the Bernanke Fed is doing you a favor with oil over $110 a barrel?

Asia? Not for the faint of heart – despite how great the news from Japan may sound. A solid political base does not necessarily translate into a solid equities market, especially when that market is being driven by the government printing Yen. The Weimer Republic tried that. To bastardize a phrase: Those who do not learn from history… come to work on Wall Street.

Says Hedgeye CEO McCullough, we are looking at the mother of all long term cycles in the equities markets. It’s OK to be early – and it’s not too late to be early, even with the markets at these levels. Be guided by interest rates, look for real growth sectors, be patient. And keep Hedgeye.com on your screen.

Sector Spotlight – Financials: Prometheus Un-Bond?

As advertised, Financials sector senior analyst Jonathan Casteleyn wowed our institutional clients this week with an in-depth call on the Asset Managers group. Followers of Hedgeye will not be surprised to learn that Casteleyn’s view of the group is heavily influenced by his analysis of the declining bond market. Indeed, lest there be any doubt in your mind, the presentation was titled “Fixing Your income: The Danger of the Bond Market.” Also note last week’s Sector Spotlight, which highlighted Hedgeye’s Debt Deflation macro theme, with the key takeaway that there just aren’t enough shares of stock in the world to satisfy investor demand. That’s a big data point, and one that weighs heavily in Casteleyn’s analysis.

Bond-doggle

With $38 trillion in face value of bonds outstanding, the US bond market is at an all-time high. And the market capitalization of the US bond market represents more than 2/3 of all securities traded in America. Casteleyn tracks the bull market in bonds over the last generation as yields on ten-year US Treasury bonds came steadily down, from over 9% in 1989, to under 2% earlier this year, before lifting back over the 2% mark – though only barely.

Fed actions to ease credit, starting with the beginnings of the QE cycles in 2008, have also had the effect of compressing the spreads between corporate and Treasurys – with even “high yield” bonds (what used to be called “junk”) coming down to mid-single digit yields as prices on all fixed income instruments inflated.

All this pushing down of yields has created fragility in the market, as measured by “Duration,” a measure of a bond’s price sensitivity to changes in its own yield . Casteleyn calculates the duration on the 10-year Treasury at around 8.9, the highest it’s been since 1989. With duration at this level, the 10-year Treasury bond will lose about 9% in price for every one percentage point increase in yield-to-maturity.

Bernanke’s rodomontade notwithstanding, the “real” marketplace is gearing up to make this happen with or without the Fed. Especially, it would seem, without.

Broker dealers have significantly trimmed their exposure to interest-rate sensitive products. If their customers decide to flee for the exits and dump their bonds, the brokers are the last ones who want to be stuck holding that inventory. This situation is made more precarious by the fact that traders at the brokerage firms have never seen a down market in bonds and will have no clue how to trade when prices begin to cascade. Today’s fixed income traders are all younger than sixty, which means they never had to trade bonds in a bear market. The last time bond yields took off to the upside was off a bottom in 1970. Rates shot up over the ensuing decade, largely in response to Muammar Gaddafi and the Arab oil embargo of 1973. Anyone who couldn’t trade that precipitous decline in bond prices didn’t last. Anyone who could trade it is probably sipping champagne on the deck of their yacht while watching the electronic flickers across their CRT indicating that the markets are once again bound for Hades in a grass-woven two-handled carryall.

Our simple prediction of the Worst Case Scenario is, rates shoot up, triggering a spate of panic selling in the bond market. This looks like the financial equivalent of a 12-lane freeway with no speed limits, not traffic lights and no cops. We come around a blind curve and the road suddenly goes from twelve lanes down to one. Casteleyn says the major brokerages have cut their fixed income exposure to half the levels they were at in 2010. If we didn’t know better, we’d say the major financial firms must be in a mild state of anticipatory panic.

The Case of the Tail That Didn’t Bark

Casteleyn says there are historical patterns that tend to play out in market pricing relationships. The Fed may play the role of Alpha Dog, but it’s ultimately the market that sets interest rates, and it has been clear to even the most casual observer that Bernanke no longer has the ability to bend the markets to his will. Although a cynic might observe that each one of his little pronunciamentos creates just enough intra-day volatility to allow traders to make a quick few bucks

A move in the price of the 10-year Treasury tends to herald a shift in the Fed Funds rate. With a lag that historically ranges between 8-14 months, market forces driving 10-year bond prices down have translated into Fed policy moves to increase the Funds rate. With duration up at levels not seen for almost 24 years, we think it reasonable to predict a spike in rates. We don’t know when this will happen, but the market is gearing up for it.

Sharp cuts in fixed income liquidity at the major brokerage firms are matched by individual investor outflows from muni bond funds. Last year, muni bond funds took in about $1 billion in new money every week. This year, they have seen outflows of $500 million a week – until just this week, which saw a whopping $2 billion in muni bond fund redemptions. Investors big and small are frantically draining liquidity from the system, creating, in Casteleyn’s words, “the potential for an explosion.” On the flip side, equity mutual funds are starting to see a trickle of positive inflows – the first they have seen since 2007 – and US households still have $9 trillion in cash, nearly 11% of total assets and near an all-time high in total liquidity. When all is said and done, Casteleyn estimates there is something on the order of $440 billion that will need to come into the equities markets in the intermediate term.

Prognosticating from his current models, Casteleyn says it is completely reasonable to expect a 5% decline in bonds between now and year end – generating a net outflow of $100 billion. This could just as easily be followed by a 10% rise in equities prices, leading to $80 billion in inflows as cash chases price.

One wild card is the nation’s pension funds. Pension fund asset allocation to equities is at all-time lows, while the allocation to Alternative Investments (read: “Hedge Funds”) is at an all-time high. The total pension fund deficit stands at around $222 billion, and the sector appears massively under-exposed to equities.

How do pension managers get out of a $222 billion hole? They can either put more cash in (where does it come from?) or they can grow their way out. We note that New York State’s Department of Financial Services has just launched a review of pension funds, under what Department chief Benjamin Lawsky calls “his office’s little-known authority to examine public retirement systems in the state” (Wall Street Journal, 30 July, “Regulator Steps Up Checks On Public Pensions.”) We would not be surprised if pension managers feel pressure to cut exposure to declining sectors (bonds), and to non-transparent sectors (hedge funds) and shove all that cash into equities. So regulatory meddling might once again accelerate an economic cycle that is already in train.

Casteleyn says current outflows from the fixed income markets thus far in 2013 are the biggest we have seen since 2008. But in 2008 there was Lehman, there was TARP, there was then-Treasury Secretary Paulson calling a frantic secret midnight conference call with members of Congress warning in urgent whispered tones that there would be rioting in the streets and martial law “within days” if the banks weren’t given hundreds of billions of dollars in bailouts (we’re not making this up…) Today, there’s just lots and lots of cash washing around, there’s Bernanke at the helm of what appears to be a rudderless craft and… are those storm clouds on the horizon?

But even as the tail of market interest rates wags the Fed’s alpha doggy, equities tend to perform well on initial rate hikes. The average historical performance of the equities market after a Fed rate hike has been a 2.8% increase after three months, a 7.5% increase after six months, and a 9.4% rise 12 months out. Timing, it would seem, is all, and Bernanke may navigate these treacherous shoals after all. If he can just hold the line on rates another couple of months, the big upsurge in the equities market should start right around the time he departs at the end of January, covering him with retrospective glory.

Who says the Professor doesn’t understand the markets?

Investing Term – Collateralized Debt Obligation

CDOs were in the news this week when a Manhattan jury found “Fabulous Fab” Fabrice Tourre guilty of fraud in connection with a Goldman Sachs CDO deal called Abacus. You may remember Tourre from his televised appearances during the Goldman Sachs hearings. Tourre came across as somewhat cocky, helped along by his French accent as he answered the Congressional panel’s questions. “Dat’s de deal!” he asserted.

Goldman extricated itself from the Abacus matter in 2010, paying a record $550 million fine. Goldman also acknowledged that its marketing materials for the subprime product contained incomplete information (SEC Release 2010-123 http://www.sec.gov/news/press/2010/2010-123.htm), a major concession in the Alice-In-Wonderland world of SEC settlements where individuals and firms accused of fraud routinely pay relatively small fines while “neither admitting nor denying” the charges.

If you want a great discussion of the role of CDOs in the financial crisis, read The Financial Crisis Inquiry Report. Authored by the Congressional Financial Crisis Inquiry Commission and published in 2011, it is engagingly written and remains one of the most informative books about the financial crisis. It’s not as fast-paced as books like Andrew Ross Sorkin’s Too Big To Fail – you don’t get the close-up of Hank Paulson vomiting in his office waste basket – but it’s nice to know we got something for all those taxpayer trillions.

CDOs For Dummies

A CDO is assembled by taking a pool of interest-paying assets and putting them together in a way that provides predictable streams of payments to the investors.

For example, a banker takes a bagful of mortgages and sorts them into stacks according to creditworthiness. We’ll call them “A,” “B,” “C,” and “Doo-doo.” The A’s, being by far the best risk, pay the lowest rate of interest, while the Doo-doos obviously pay the highest.

The mortgages are rolled up and sold to investors in “tranches” – the French word for “slice,” nod to Fabulous Fabrice – with the senior tranche receiving an AAA rating, based on its receiving nearly all of its income from the top-rated mortgages in the pool. Senior tranches also have first claim on revenues from the lower-rated tranches to guarantee their stated payments, and on the collateral itself in the event some of the mortgages in the pool default. If the Doo-doos default, the owner of the Doo-doo tranche is out of luck. If the AAA tranche defaults, the Doo-doos’ collateral could be sold to make the AAA investors whole. This wipes out the Doo-doos, but the investors “knew” they were taking on this risk.

Starting with the first CDO issue in 1987, and up until the mid-2000’s, banks created diversified CDOs, packaging together everything from auto loans and aircraft leases, to construction loans and credit card debt. This was great for the banks, because by securitizing their loans they could remove them from their books and replace them with actual cash from the investors. This helped banks to continue to lend, while keeping their reserve requirements low. (Can you see where this starts to create systemic risk? Hold onto your hats.)

So the banks were lending and re-lending, all on the same capital base. They generated loan fees and took in investor cash, all without having to increase reserves. Defaults were sequestered inside the CDOs and wouldn’t hit the books of the banks. Diversified CDOs offered a degree of safety against sector risk, and the CDOs were yielding as much as 2% or even 3% above corporate bonds at equivalent rating levels.

Around 2005, the world’s appetite for dollar-denominated interest-bearing instruments really heated up. This was great for CDO issuer business, but the banks soon ran into a supply constraint, because let’s face it, not everyone in America automatically qualifies for a mortgage. (We told you it was going to get interesting.)

In short order, banks and realtors and investment bankers and mortgage originators – aided and abetted by Congress, the president, and especially the eminence not-so grise of Fed Chairman Alan Greenspan – combined to give the world what they wanted. Enter the shadowy world of subprime mortgages, “NINJA” and “Liar” loans, of falling interest rates and federal housing guarantees. Former treasury secretary Hank Paulson says in the FCIC report “subprime mortgages went from accounting for 5 percent of total mortgages in 1994 to 20 percent by 2006. Securitization separated originators from the risks of the products they originated.”

When were they going to tell us this?

By 2006-2007 the industry had created CDOs out of CDOs, with names such as “CDO Squared.” They took all the BBB and CCC tranches and piled them together into great CDOs that they then convinced the rating agencies to deem AAA. The argument was that that pooling a bunch of sub-prime mortgages across a number of geographic regions created sufficient diversity to lower the overall risk of the instrument. The rating agencies bought it. Guys like Fabrice Tourre sold it. People like your company’s pension fund manager, your state public employees’ pension manager, and investment managers all over the world all bought it. By 2006 there was more than $1.5 trillion in CDOs outstanding globally.

Not So Fabulous

Many on Wall Street were expecting Tourre to be acquitted. They called the SEC’s case “weak” and said the government’s lawyers kept lulling jurors into a stupor with technical jargon. But the judge kept a brisk pace, with the result that the jury was able to go home for the weekend and cash their final per diem checks.

Some observers said the jury seemed intent on nailing Tourre, not just because he came across as a perfect snot – and a poster boy for the case against immigration reform – but because, despite all the dirty dealings on Wall Street over the years, he was all they got. Tourre was the jurors’ only chance to actually nail someone for the financial crisis – a period about which the SEC has been stunningly quiescent, when they weren’t busy being incompetent.

We hope for a more effective SEC chairman Mary Jo White. The compromised culture of settlements and the profound culture of incompetence, bred by years of hostility and neglect by Congress, have embedded financial fraud as an acceptable business model. Ever-larger settlement amounts merely set up tollbooths on the superhighway of crime. Tourre appears to be the one unlucky son of a gun who will bear the Scarlet $, as we are at the tail end of the Commission’s ability to try Financial Crisis-era cases. (Note that the statute of limitations on SAC’s Steven Cohen’s alleged activities just ran out, which is likely why the Commission hit him with an administrative “failure to supervise” charge, possibly hoping they can coattail that into something meatier.)

We urge Ms. White to get in Congress’ face to put some muscle into the Commission’s policing efforts. It’s long overdue.

by Moshe Silver

Moshe is a Hedgeye Managing Director and author of the Hedgeye e-book Fixing A Broken Wall Street