Keeping with our Forest vs. Tree theme of the last couple weeks (U.S. Growth - #TRENDing, 2Q13 GDP: Hurry Up & Wait, Separating the Forest from the Trees in EM) - from a broad, top down perspective, remember how this whole economic reflexivity thing works:

Rising demand/spending drives income and employment higher which then drives consumption and confidence higher in a virtuous, self-reinforcing cycle. Credit serves to amplify the cycle with credit expansion following pro-cyclically as loan demand and creditworthiness both increase alongside rising incomes and a re-flation in household net wealth.

At present, the TREND slope of improvement across the Labor Market data (inclusive of today’s initial claims release), Confidence, Consumption & Credit are all positive. We aren’t buyers of all things, pro-growth U.S. equities at every price, but we likely will continue to not be buyers of Bonds, Gold, or broader EM at any price in the immediate/intermediate term. In fact, our 0% allocation to commodities turned 100 days old today.

Below is the breakdown of this morning's claims data, along with some sector specific takeaways, from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact .

- Hedgeye Macro

---------------------------------------------------------------------------------

Full Sails

Last week we flagged the deceleration in trendline improvement on a one week basis. It was notable in that it was a deviation vs the preceding 9 weeks of data. That inflection proved short-lived, however, as this week's print resumes the trend of accelerating improvement in the labor market that had been in place prior to last week.

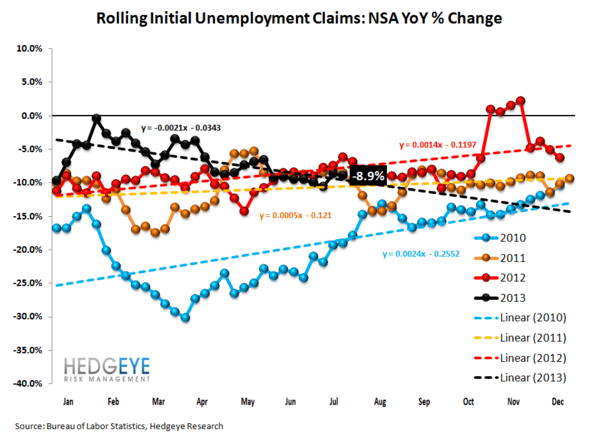

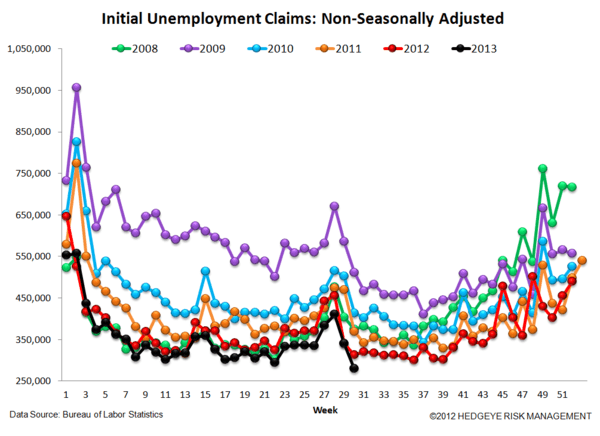

This past week, rolling NSA initial claims were 8.9% lower than the prior year. This marks a modest acceleration in the rate of improvement vs the prior week, when rolling NSA claims were better by 8.7%, but remains down vs the two weeks ago rate of -10.6%. On a single week basis, NSA claims were 10.6% lower than the previous year, a sharp acceleration vs the prior 1-week print of -0.2%, and back in-line with the previous 9 prints of -9.9%, -13.3%, -9.4%, -9.2%, -7.7%, -11.7%, -9.4%, -7.6% and -8.0%.

To reiterate what we've been saying for 9 of the last 10 weeks, this trend of accelerating improvement in the labor market is profound. We saw it across the board in 2Q earnings as credit metrics, namely new delinquency trends, came in better than expectations and bottom line beats were largely catalyzed by larger than expected reserve release predicated on this accelerating labor market dynamic. The data we've seen thus far in 3Q, now one month along, suggests a continuation of the trend we saw in 2Q, at least on the credit front.

The Data

Prior to revision, initial jobless claims fell 17k to 326k from 343k WoW, as the prior week's number was revised up by 2k to 345k.

The headline (unrevised) number shows claims were lower by 19k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4.5k WoW to 341.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -8.9% lower YoY, which is a sequential improvement versus the previous week's YoY change of -8.7%

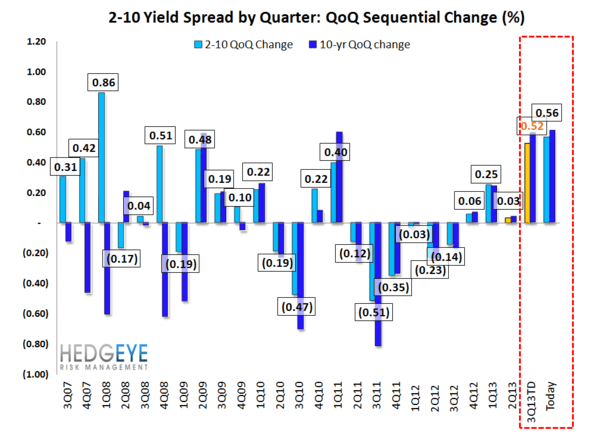

Yield Spreads

The 2-10 spread rose 4 basis points WoW to 227 bps. 3Q13TD, the 2-10 spread is averaging 223 bps, which is higher by 52 bps relative to 2Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT