Or is Washington The New Reality Wall Street now? Who knows... Rhetorically, the politicization of the US Financial System is making this very hard to follow...

What is never hard to follow is the money. If you want to gain a clear understanding of where economic systems have a high probability of playing out, follow how people get paid.

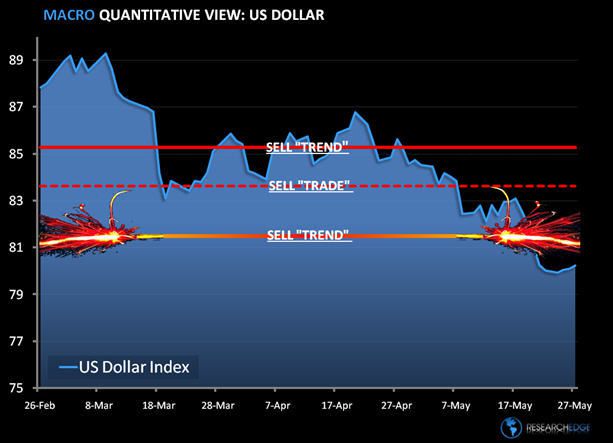

In sharp contrast to the made-up rules to made-up "stress tests", the US Dollar trades on a marked-to-market basis. In global currency trading, there is no such thing as a newly implemented American Idol like "save." The chart below is the chart that matters. American Idol season is over, and the world has voted. The US currency continues to lose its credibility.

There are two TREND lines that matter in the chart below. The intermediate-term TREND line that broke in late April ($85.29) and the long-term TREND line that broke last week ($81.51). It's the latter TREND line that has the hair standing up on my back - Washington ignoring the alarm bell just makes thing worse. If Bush was willfully blind, Obama is apparently willfully deaf.

Is the brain-trust of Wall Street/Washington paid to be willfully blind and deaf? You tell me. The compensation structure of the current system will give you the bipartisan answer. Thankfully, as of yesterday's Opinion piece in the Financial Times by Stanford professor John Taylor, titled "Exploding debt threatens America", I'm not the Lone Survivor of sight and sound.

With regards to the groupthink associated with the Obama one liner of "we inherited this mess", Taylor poses an interesting question: "The debt was 41 per cent of GDP at the end of 1988, President Ronald Reagan's last year in office, the same as at the end of 2008, President George W. Bush's last year in office. If one thinks policies from Reagan to Bush were mistakes does it make any sense to double down on those mistakes, as with the 80 per cent debt-to-GDP level projected when Mr Obama leaves office?"

This chart isn't about being political. The American Financial system is becoming as political as politics get. The world is watching this real-time, and voting with their wallet.

Keith R. McCullough

Chief Executive Officer