TODAY’S S&P 500 SET-UP – August 1, 2013

As we look at today's setup for the S&P 500, the range is 17 points or 0.22% downside to 1682 and 0.79% upside to 1699.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.30 from 2.27

- VIX closed at 13.45 1 day percent change of 0.45%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: Bank of England rate decision; est. 0.5% (prior 0.5%)

- 7:30am: Challenger Job Cuts Y/y, July (prior 4.8%)

- 7:30am: RBC Consumer Outlook Index, Aug. (prior 50.7)

- 7:45am: ECB announces interest rates; est. 0.5% (prior 0.5%)

- 8:30am: ECB’s Draghi holds news conference

- 8:30am: Init Jobless Claims, July 27, est. 345k (prior 343k)

- 8:58am: Markit US PMI Final, July, est. 53.2

- 9:45am: Bloomberg Consumer Comfort, July 28 (prior -27.3)

- 10am: Construction Spend M/m, June, est. 0.4% (prior 0.5%)

- 10am: ISM Manufacturing, July, est. 52 (prior 50.9)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 5pm: Total Vehicle Sales, July, est. 15.8m (prior 15.89m)

GOVERNMENT:

- House Energy and Commerce Cmte hears from Medicare and Medicaid Services Administrator Marilyn Tavenner on Affordable Care Act implementation

- 8:30am: Energy Dept’s Bioenergy Technologies Office, Advanced Biofuels USA hold conf on bioindustry role in American energy

- 9am: SEC Commissioner Troy Paredes discusses finl regulation at Chamber of Commerce’s Center for Capital Markets Competitiveness event

- 9:30am: Senate Energy and Natural Resources Cmte hearing on the political status of Puerto Rico

- 10am: House Armed Services Cmte hearing on “Initial Conclusions Formed by the Defense Strategic Choices and Management Review”

- 1:30pm: API briefing on oil, natgas industry jobs, economic analysis by PricewaterhouseCoopers

WHAT TO WATCH

- U.S. trade agency issues ruling on Samsung import limit

- Tenet, Health Management accused of paying kickbacks to clinic

- Macy’s makes final bid to block Martha Stewart goods at rival

- Walgreen investors sue CEO over $80m DEA painkiller fine

- Lloyds prepares to resume dividends as Osborne weighs sale

- Apple’s new iPad mini likely to have Samsung display, WSJ says

- Citigroup ordered to pay $10.8m for soured RBS investment

- Celltrion says reports of stake sale to AstraZeneca inaccurate

- Tourre jurors end first day of deliberations without verdict

- Dish customers blocked as Raycom Media accord expires

- Congress votes to reverse rise in student-loan interest rates

- China pledges to keep growth within “reasonable zone”

- U.K. factory growth strengthens as recovery builds momentum

- Australia to raise tobacco excise to narrow budget shortfall

- July Auto Sales: July SAAR May Be 15.8m

EARNINGS

AM:

- Alliant Techsystems (ATK) 7:01am, $1.92

- AltaGas (ALA CN) 7:45am, C$0.21

- Ameren (AEE) 7:48am, $0.46

- Ansys (ANSS) 7:09am, $0.71

- Apache (APA) 8am, $2.00 - Preview

- Arena Pharmaceuticals (ARNA) 7am, $0.18

- Automatic Data Processing (ADP) 7:30am, $0.57

- Avon Products (AVP) 7:01am, $0.26

- Barrick Gold (ABX CN) 6:31am, $0.56 - Preview

- Becton Dickinson (BDX) 6am, $1.48

- BGC Partners (BGCP) 8am, $0.13

- Bombardier (BBD/B CN) 6am, $0.09

- Cameco (CCO CN) 8:23am, C$0.18

- Cardinal Health (CAH) 7am, $0.77

- Catamaran (CCT CN) 6am, $0.44

- CenterPoint Energy (CNP) 8:15am, $0.26

- Chesapeake Energy (CHK) 7:01am, $0.41 - Preview

- Cigna (CI) 6am, $1.60

- Clorox (CLX) 8:30am, $1.34 - Preview

- CME Group (CME) 7am, $0.90

- Colonial Properties Trust (CLP) 7am, $0.33

- ConocoPhillips (COP) 7am, $1.29 - Preview

- Covidien (COV) 6am, $0.89

- CVR Energy (CVI) 8am, $1.62

- CVR Refining (CVRR) 8am, $1.66

- Dentsply Intl (XRAY) 7am, $0.65

- DirecTV (DTV) 7:30am, $1.34 - Preview

- Dynegy (DYN) 7:30am, $(0.29)

- Enbridge (ENB CN) 7am, C$0.39 - Preview

- Enterprise Products (EPD) 6am, $0.69

- Exxon Mobil (XOM) 8am, $1.89 - Preview

- Fluor (FLR) 9am, $1.01

- Fortis (FTS CN) 7am, C$0.32

- Fortress Investment (FIG) 7am, $0.20

- Genesee & Wyoming (GWR) 6am, $1.11

- Gildan Activewear (GIL CN) 6:31am, $0.94

- Halcon Resources (HK) 7:30am, $0.06

- HCA Holdings (HCA) 7:03am, $0.91

- IGM Financial (IGM CN) 10:30am, C$0.76

- Imperial Oil (IMO CN) 7:55am, C$0.98

- Incyte (INCY) 7am, $0.01

- Iron Mountain (IRM) 6am, $0.31

- ITT (ITT) 7am, $0.45

- Kellogg (K) 8am, $0.98 - Preview

- LKQ (LKQ) 7:30am, $0.25

- Magellan Midstream (MMP) 8am, $0.54

- Marathon Petroleum (MPC) 7:03am, $1.90

- MSCI (MSCI) 7:30am, $0.53

- Mylan (MYL) 7am, $0.67

- New York Times (NYT) 8:30am, $0.13

- NII Holdings (NIHD) 6:30am, $(1.16)

- Nu Skin Enterprises (NUS) 7:30am, $1.20

- Ocwen Financial (OCN) 7:30am, $1.02

- PBF Energy (PBF) 8am, $0.79

- PPL (PPL) 7am, $0.47

- Procter & Gamble (PG) 6:58am, $0.77 - Preview

- Quanta Services (PWR) 6:07am, $0.37

- Quintiles Transnational (Q) Bef-mkt, $0.44 - Preview

- Sally Beauty Holdings (SBH) 7:30am, $0.43

- Scana (SCG) 7:30am, $0.54

- Targa Resources (NGLS) 7am, $0.14

- Teco Energy (TE) 7am, $0.27

- Teradata (TDC) 6:45am, $0.71

- Time Warner Cable (TWC) 6am, $1.65 - Preview

- TMX Group (X CN) 6am, C$0.83

- Vulcan Materials (VMC) 8am, $0.16

- Western Refining (WNR) 6am, $1.20

- WPX Energy (WPX) 7am, $(0.19)

- Xcel Energy (XEL) 7am, $0.39

PM :

- Activision Blizzard (ATVI) 4:05pm, $0.08

- American International Group (AIG) 4pm, $0.86

- Apartment Investment & Mgmt (AIV) 4:05pm, $0.48

- Bill Barrett (BBG) 4:15pm, $(0.01)

- Consolidated Edison (ED) 6:43pm, $0.57

- DCT Industrial Trust (DCT) 4:10pm, $0.11

- Edison International (EIX) 4pm, $0.66

- Extra Space Storage (EXR) 4:05pm, $0.49

- Fairfax Financial Holdings (FFH CN) 5:01pm, $(12.40)

- Federal Realty Investment Trust (FRT) 4:30pm, $1.12

- FleetCor Technologies (FLT) 4:01pm, $0.95

- Home Properties (HME) 4:30pm, $1.09

- Kodiak Oil & Gas (KOG) 4:01pm, $0.13

- Kraft Foods (KRFT) 4pm, $0.67 - Preview

- Leap Wireless (LEAP) 4:05pm, $(1.02)

- LeapFrog Enterprises (LF) 4:01pm, $(0.08)

- LinkedIn (LNKD) 4:05pm, $0.31 - Preview

- MercadoLibre (MELI) 4:01pm, $0.63

- Mohawk Industries (MHK) 4:01pm, $1.66

- MRC Global (MRC) 4:15pm, $0.38

- ON Semiconductor (ONNN) 4:03pm, $0.13

- OpenTable (OPEN) 4:31pm, $0.47

- Osisko Mining (OSK CN) 4:05pm, C$0.05

- PerkinElmer (PKI) 4:05pm, $0.48

- Piedmont Office Realty Trust (PDM) 5:02pm, $0.34

- Public Storage (PSA) 5:14pm, $1.77

- ResMed (RMD) 4:05pm, $0.62

- SBA Communications (SBAC) 4:01pm, $(0.10)

- Southwestern Energy (SWN) 5:15pm, $0.52 - Preview

- Synaptics (SYNA) 4:15pm, $1.30

- Tesoro (TSO) 4:31pm, $1.43 - Preview

- ValueClick (VCLK) 4:05pm, $0.39

- Walter Energy (WLT) 4:01pm, $(0.75)

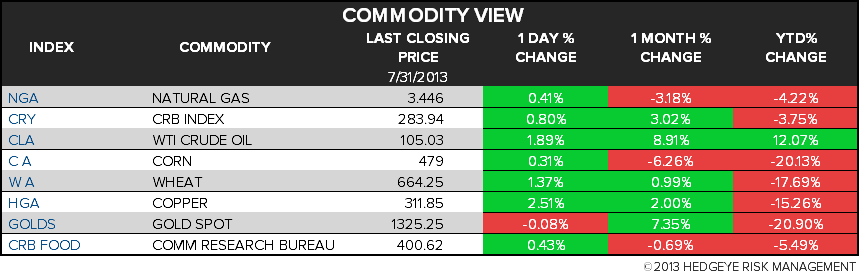

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Japan Purchases First Oregon Wheat Since Discovery of GMO Crop

- p Commodities Market, Industry News »

- Burger Costs Rising With Beef Supply at 21-Year Low: Commodities

- Pan Pacific Sees Copper Surplus at 5-Year High on Slowing China

- Wheat Rises a Fifth Day on Speculation Chinese Demand to Gain

- WTI Rises to One-Week High on Fed Stimulus, China Manufacturing

- China Makes First Investment in South African Wine Industry

- Gold Swings Expand as Jobs Help Gauge Stimulus: Chart of the Day

- Palm Climbs to One-Week High as Malaysian Exports Signal Demand

- Coffee Exports From Indonesia’s Sumatra Surge to Four-Year High

- Barrick Takes $8.7 Billion Writedown, Cuts Dividend on Gold Drop

- Rebar Extends Monthly Gain as China Manufacturing Strengthens

- No Rebound for Uranium Seen as Japan Plants Idle: Energy Markets

- Chile Copper Output Up for Second Month as Strikes Ebb: BI Chart

- COMMODITIES DAYBOOK: U.S. Beef Production Plunges to 21-Year Low

- ANZ Opens 50 Ton Gold Vault in Singapore as Asian Demand Climbs

CURRENCIES

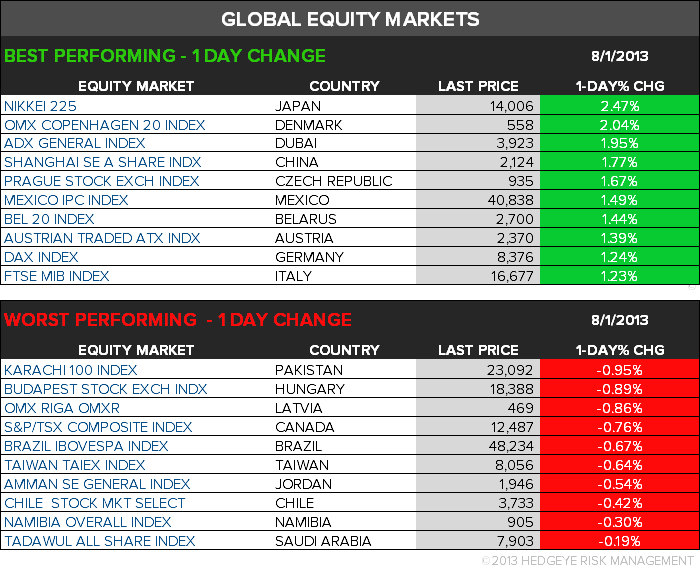

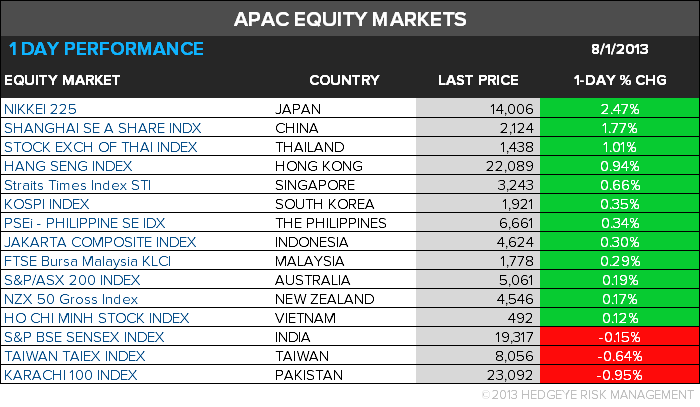

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team