We believe EAT will report disappointing 4Q13 results.

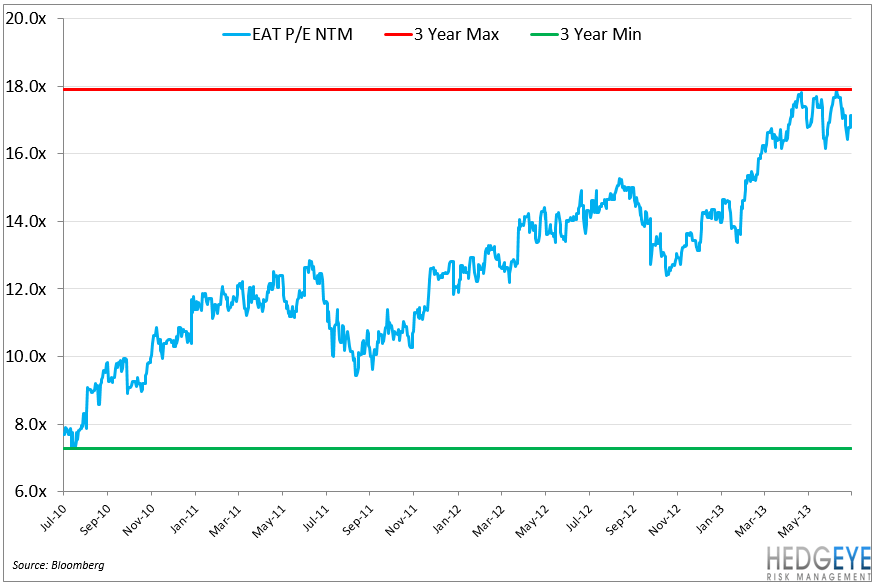

Over the past month, the S&P has risen 5.3% while the Bloomberg Full Service Restaurant Index has declined 2%. During this time, EAT has only declined 1% and sits 6.9% below its all-time high of $41.93. At 7.8x EV/EBITDA, EAT is currently trading below its peer group average of 8.7x. That being said, we believe the whole group, including EAT, could see multiples revised lower in the coming months.

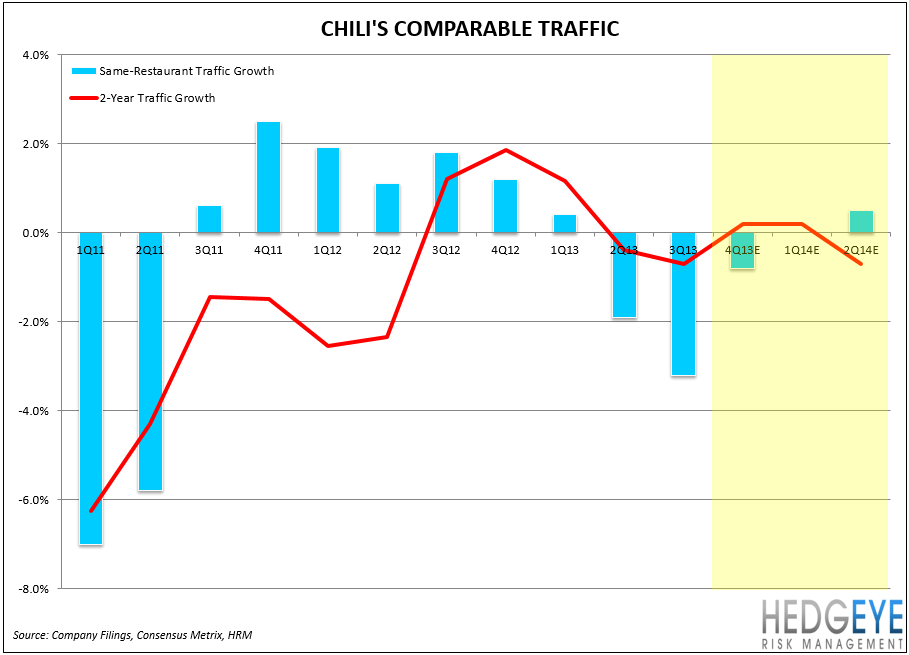

We continue to believe EAT is one of the best managed companies in the restaurant space, but it is not immune to the industry’s softening secular trends. After seven straight quarters of positive traffic growth (3Q11 to 1Q13), Chili’s is looking at its third consecutive quarter of a decline in traffic growth. We believe that the slowdown in traffic trends at Chili’s can be attributed to the confluence of a secular decline in industry trends and aggressive discounting from DRI.

Sales Trends

In 3Q13, EAT reported 20% EPS growth on a 0.6% decline in revenue growth. In 4Q13, street estimates are looking for EPS growth of 23% ($0.74) on revenue growth of 1.2%. Given the reported decline in industry sales trends in June, we believe it will be very difficult for EAT to realize the 180bps sequential acceleration in revenue growth that consensus is looking for in 4Q13.

HEDGEYE – Same-store sales trends at Chili’s are a critical variable in the financial performance of the company. We foresee sales trends at lunch slowing under the pressure of increased discounting from DRI. The company has only beaten revenue estimates in 4 of the last 8 quarters.

Operating Margin Trends

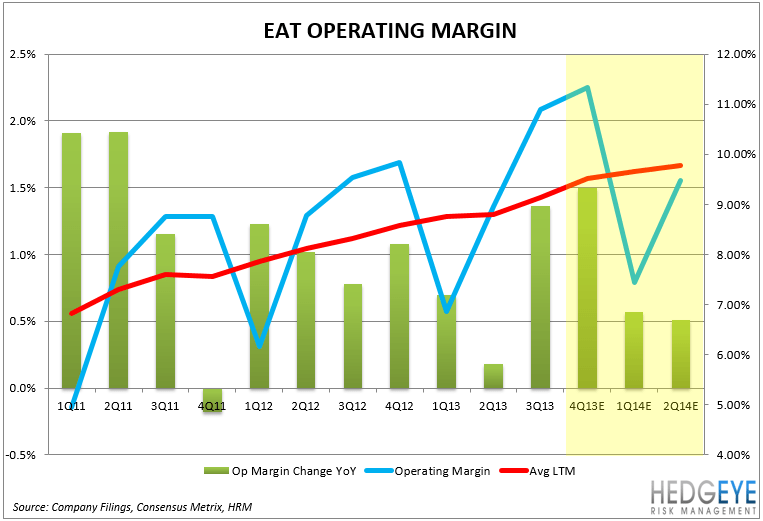

We expect cost of sales to decline 60-70bps year-over-year, driven mainly by favorable mix in part to the 3Q13 introduction of its pizza and flatbread category coupled with some benefit from menu pricing. Since 2Q11, EAT has made significant progress in bringing down labor costs through the implementation of its “Kitchen-of-the-Future” initiatives. However, we suspect that some of this continued benefit from labor deleverage will be partially offset by weak same-store sales trends.

Between other operating expenses and G&A, we don’t believe EAT has enough leverage in the P&L to produce the 150bps year-over-year improvement in operating margin that the street is expecting.

HEDGEYE – Unfortunately, DRI’s aggressive discounting is making life difficult for every player in the casual dining space and particularly for EAT. We don’t expect EAT’s management to respond to the increased promotional environment and this could hurt traffic trends on the margin.

Sentiment

Illustrated in the chart below, 52.4% of analysts rate EAT a Buy, 42.9% rate EAT a Hold, and 4.8 rate EAT a Sell. The sell-side is slowly beginning to come around to our bearish view as a few analysts have downgraded the stock from Buy to Hold in July. Short interest in the stock is currently 11.12% of the float.

HEDGEYE – We believe that EAT’s 4Q13 results will confirm our bearish thesis on the company and the rest of the casual dining industry.

Valuation

At 7.8x EV/EBITDA EAT is trading at a slight discount to its Casual Dining peer group trading at 8.7x EV/EBITDA. Facing slowing traffic trends and significant pressure from DRI’s aggressive discounting, we believe EAT is appropriately valued slightly below its peer group.

HEDGEYE – We believe the whole group is likely to see multiples revised lower in the current quarter.

The company is hosting its earnings call on Friday morning at 10:00am EST. We’ll post on anything incremental after the call.

Howard Penney

Managing Director