TODAY’S S&P 500 SET-UP – July 30, 2013

As we look at today's setup for the S&P 500, the range is 20 points or 0.38% downside to 1679 and 0.81% upside to 1699.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.28 from 2.29

- VIX closed at 13.39 1 day percent change of 5.27%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC retail sales

- 8:55am: Redbook weekly retail sales

- 9am: S&P/Case Shiller Home Prices M/m, May, est. 1.45%

- 9am: S&P/Case Shiller Index, May (prior 152.37)

- 10am: Conference Board Consumer Conf Index, July, est. 81

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2043 sector

- 11:30am: U.S. to sell 4W bills

- 4:30pm: API crude, oil product inventories

GOVERNMENT:

- President Obama travels to Tenn. to speak on U.S. economy

- FOMC begins 2-day closed mtg on interest rates, 9am

- CFTC rules for procedures to establish appropriate minimum block sizes for large notional off-facility swaps and block trades become effective

- Senate Banking Cmte hears from SEC Chairman Mary Jo White, CFTC Chairman Gary Gensler on limiting systemic risk in financial markets, 10am

- Gina McCarthy gives first speech since becoming EPA chief

- Senate confirms James Comey as new FBI director

WHAT TO WATCH

- JPMorgan accused of gaming energy bids, FERC settlement looms

- Barclays to raise GBP5.8b in rights offering

- Pfizer 2Q adj. EPS beat as co. prepares to split units

- Uralkali sees potash price slump after exiting BPC venture

- UBS to buy back Swiss central bank’s fund to boost equity

- Time Warner Cable-CBS talks pass deadline without blackout

- General Growth to sell its stakes in Aliansce for $690m

- Centrica buys Hess’s Energy Marketing business

- Zynga said to lose three top executives after CEO change

- Deutsche Bank 2Q net misses ests. on legal costs

- Alcatel-Lucent beats ests. as Qualcomm to buy stake

- Lockheed said to reach agreement w/Pentagon on 71 more F-35s

- Moore said to hear Canada wireless concerns about Verizon

- Tourre rests defense in SEC case w/out calling any witnesses

EARNINGS:

- Aetna (AET) 6am, $1.40

- Nielsen Holdings (NLSN) 6am, $0.49

- Westlake Chemical (WLK) 6am, $1.98

- Mednax (MD) 6am, $1.36

- Generac Holdings (GNRC) 6am, $0.76

- MDC Holdings (MDC) 6am, $0.58

- Lexicon Pharmaceuticals (LXRX) 6am, $(0.06)

- Harris (HRS) 6:30am, $1.15

- Pitney Bowes (PBI) 6:30am, $0.44

- RR Donnelley & Sons (RRD) 6:30am, $0.41

- Waddell & Reed Financial (WDR) 6:59am, $0.64

- Merck & Co (MRK) 7am, $0.82 - Preview

- Discovery Communications (DISCA) 7am, $0.91

- National Oilwell Varco (NOV) 7am, $1.33

- Thomson Reuters (TRI CN) 7am, $0.45

- Corning (GLW) 7am, $0.31

- Coach (COH) 7am, $0.89 - Preview

- Fidelity National Information Services (FIS) 7am, $0.70

- Rockwell Automation (ROK) 7am, $1.39

- Entergy (ETR) 7am, $1.15

- Cobalt International Energy (CIE) 7am, $(0.15)

- Alliance Data Systems (ADS) 7am, $2.30

- Western Union (WU) 7am, $0.34

- TRW Automotive Holdings (TRW) 7am, $1.69

- Xylem (XYL) 7am, $0.44

- Goodyear Tire & Rubber (GT) 7am, $0.48

- Aegerion Pharmaceuticals (AEGR) 7am, $(0.62)

- Office Depot (ODP) 7am, $(0.10)

- Boyd Gaming (BYD) 7am, $0.00

- Senior Housing Properties Trust (SNH) 7:01am, $0.44

- Affiliated Managers Group (AMG) 7:10am, $2.10

- MeadWestvaco (MWV) 7:15am, $0.28

- Occidental Petroleum (OXY) 7:30am, $1.60

- NextEra Energy (NEE) 7:30am, $1.28

- Cummins (CMI) 7:30am, $1.98

- Waste Management (WM) 7:30am, $0.55

- Public Service Enterprise Group (PEG) 7:30am, $0.45

- Vishay Intertechnology (VSH) 7:30am, $0.22

- JetBlue Airways (JBLU) 7:30am, $0.14

- Arch Coal (ACI) 7:30am, $(0.33) - Preview

- TransAlta (TA CN) 7:44am, $0.18

- U.S. Steel (X) 7:45am, $(0.78)

- HCP (HCP) 8am, $0.74

- George Weston (WN CN) 8am, $1.10

- UDR (UDR) 8am, $0.34

- 3D Systems (DDD) 8am, $0.24

- Amgen (AMGN) 4pm, $1.74 - Preview

- Fiserv (FISV) 4:01pm, $1.44

- Canadian Oil Sands (COS CN) 4:01pm, $0.52

- Kimco Realty (KIM) 4:01pm, $0.33

- Chicago Bridge & Iron (CBI) 4:01pm, $1.01

- Hanesbrands (HBI) 4:01pm, $0.94

- IAC/InterActiveCorp (IACI) 4:01pm, $0.94

- American Capital (ACAS) 4:01pm, $0.24

- Questcor Pharmaceuticals (QCOR) 4:01pm, $1.04

- NCR (NCR) 4:02pm, $0.66

- Covance (CVD) 4:03pm, $0.77

- ONEOK Partners (OKS) 4:05pm, $0.54

- ONEOK (OKE) 4:05pm, $0.28

- Trimble Navigation (TRMB) 4:05pm, $0.37

- Axis Capital Holdings (AXS) 4:05pm, $0.48

- Riverbed Technology (RVBD) 4:05pm, $0.22

- Take-Two Interactive Software (TTWO) 4:05pm, $(0.56)

- InvenSense (INVN) 4:05pm, $0.14

- Symantec (SYMC) 4:07pm, $0.36

- Aflac (AFL) 4:09pm, $1.51

- Verisk Analytics (VRSK) 4:10pm, $0.53

- Genworth Financial (GNW) 4:10pm, $0.29

- Arthur J Gallagher (AJG) 4:10pm, $0.70

- Access Midstream Partners (ACMP) 4:15pm, $0.31

- Fortinet (FTNT) 4:15pm, $0.10

- Oil States International (OIS) 4:16pm, $1.51

- Weatherford International (WFT) 4:38pm, $0.15

- Duke Realty (DRE) 4:45pm, $0.26

- Equity Residential (EQR) 4:58pm, $0.71

- Lundin Mining (LUN CN) 5pm, $0.05

- Boston Properties (BXP) 5:09pm, $1.27

- SM Energy (SM) Aft-mkt, $0.77

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Falls to Three-Week Low as U.S. Economic Growth Seen Slowing

- Gold Loss to Platinum Widening for Best Forecasters: Commodities

- JPMorgan Accused of Gaming Energy Bids as FERC Settlement Looms

- Wheat Rises on Indications of Revived Demand From Japan to Egypt

- Copper Falls as Growth Misses Targets in Most Chinese Provinces

- Einhorn’s Reinsurer Says It Cut Gold Holding Amid Bear Market

- Uralkali Breaks Potash Cartel to Grab Market Share on Price Drop

- Food-Grain Harvest in India Seen at Record on Monsoon Rainfall

- Raw Sugar Climbs to Four-Week High on Demand, Frost; Cocoa Slips

- Crude Inventories Decline a Fifth Week in Survey: Energy Markets

- Rebar Trades Near Three-Week Low as Construction Slows in Summer

- China Steel Stockpiles Seen Nearing 2012 Levels as Output Slows

- China Iron Ore Production Jumps 10.7% in June: BI Chart

- Regulators Face Scrutiny on Banks’ Commodities at Senate Hearing

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

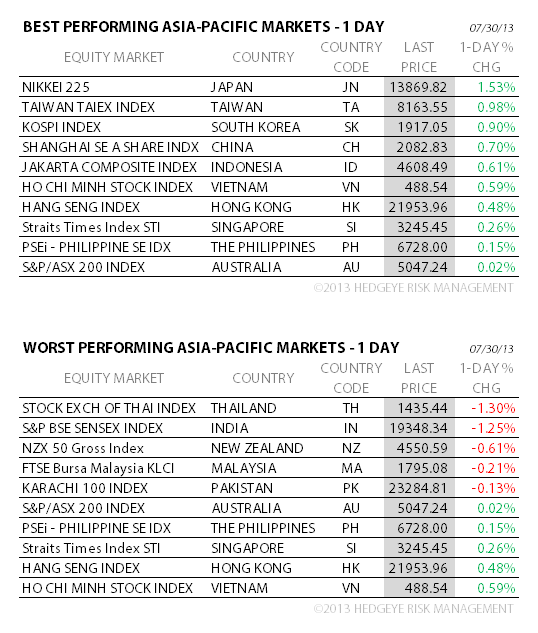

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team