While we’ve had a series of policy driven, compressed economic cycles over the last 4+ years, the reality is that economies are generally reflexive, self-reinforcing in both directions, and not as whimsical as media reporting fettered in mania and recency bias would hope you to believe.

An honored idiom in the Hedgeye Macro Manifesto says that everything that matters in Macro happens on the margin. While data myopia has its place and forecasting inflections in the slope of growth remains the game, its important to contextualize the most recent data within the context of the slope of the TREND.

With FOMC, 2Q GDP, PCE, Home Sales, Confidence, Vehicle Sales, Treasury 3Q debt funding estimates, and Employment all on the docket, there will be a lot of macro tree’s to stare at this week. Ahead of that, below we take a small step back with a quick visual tour of the domestic macro forest (i.e the TREND).

We can certainly identify some prospective growth headwinds, and we’ll gladly change our view as the research and price signals shift but, on balance, the TREND in the data we’re generally concerned with - Labor, Housing, Confidence, Consumption, Credit - remain positive. A summary review of those metrics below.

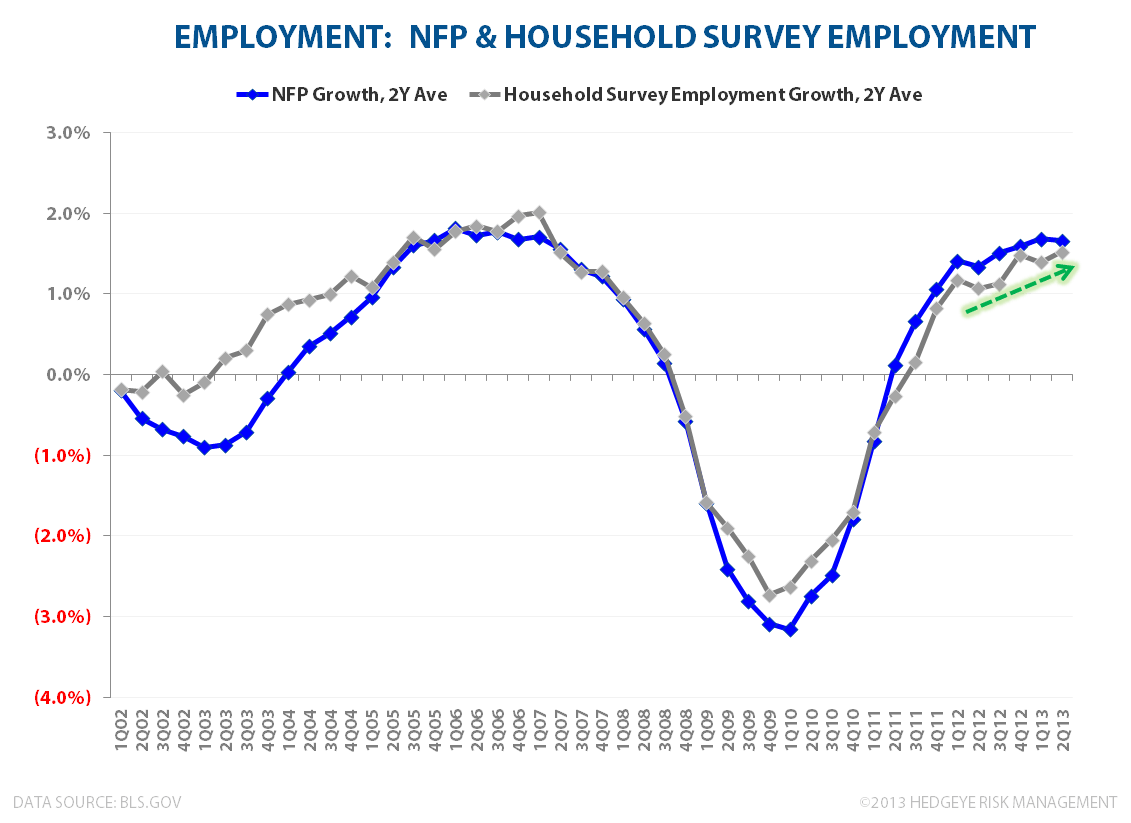

Employment: The Trend in Initial Claims remains one of accelerating improvement while employment growth as measured by the BLS’s Establishment and Household Survey’s both remain positive. The Unemployment rate continues to reflect solid Trend improvement and State & local government employment (~14% of the Workforce) registered positive growth in May for the 1st time since June of 2009.

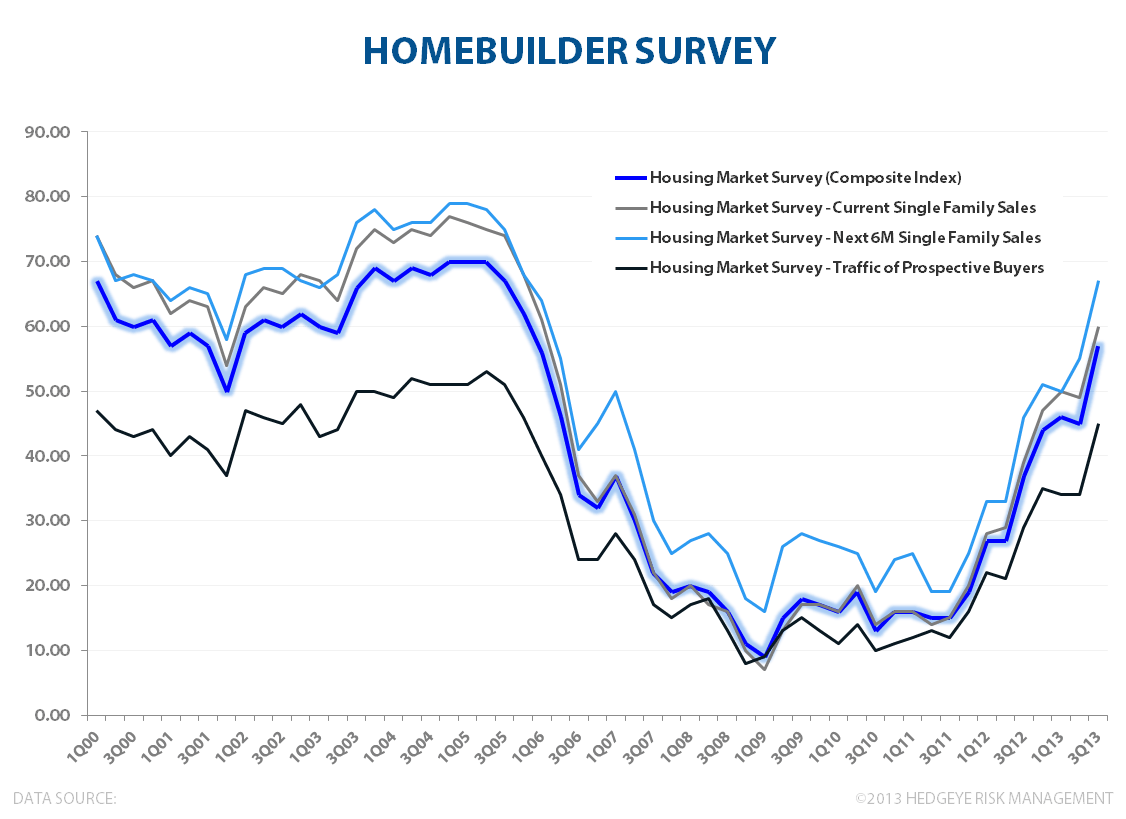

HOUSING: Housing has largely realized the parabolic recovery we forecast back in 4Q and home price appreciation, home builder sentiment and household formation trends all remain strong. From here, its likely the rate of change decelerates a bit as we come up against increasingly steeper pricing comps.

Here, its increasingly important to define the targeted investment duration with respect to housing and to separate the investment conclusion from the broader economic impact. On the investment side, we have been out of the way of housing for the last couple months, but remain bullish on the intermediate/long-term demand dynamics and are looking to buy back long exposures as expectations re-base. From a secular top down perspective, a deceleration in home price growth from a mid-teen’s to mid-upper single digit growth rate will remain an ongoing support to the domestic recovery.

Source: Hedgeye Financials

CONFIDENCE: Confidence readings across the primary surveys continue to make new 5Y highs and are finally beginning to break out of their post recession channel. Historically, correlations between confidence and economic activity have been strong to very strong. We expect Confidence - Econ correlations to re-tighten and measures such as money velocity and new orders to begin to pick-up should the emergent breakout in consumer and business confidence sustain itself.

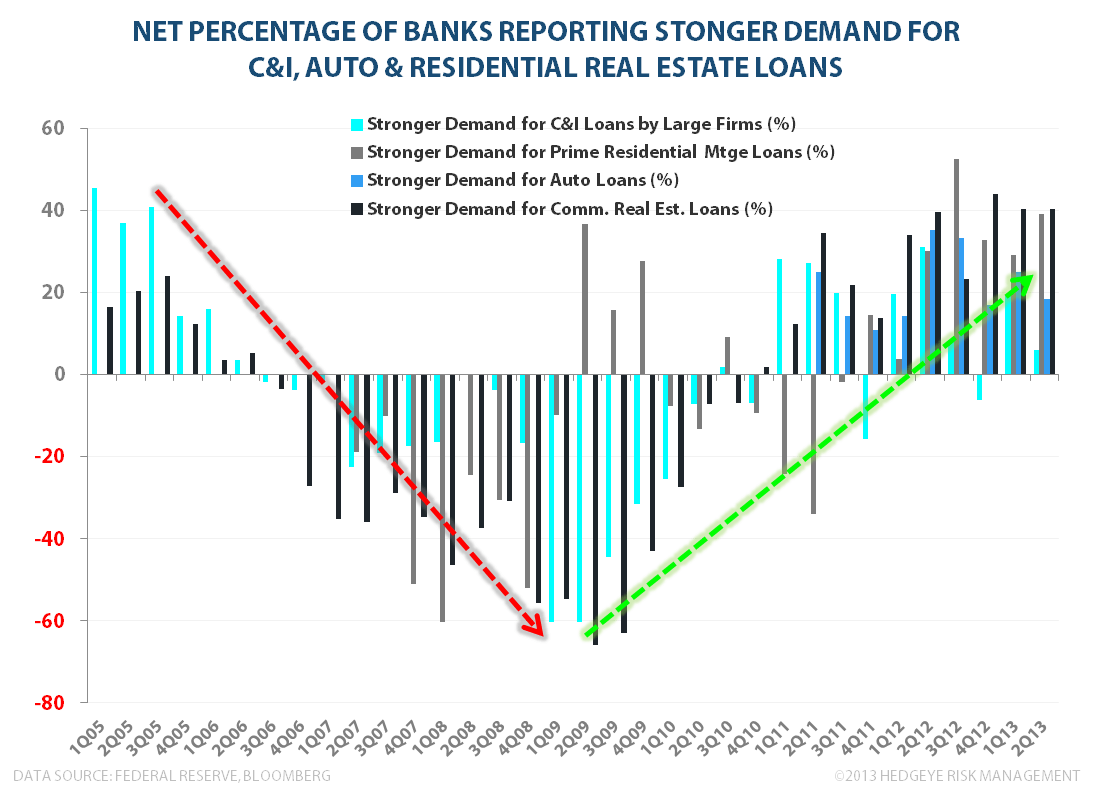

CREDIT: Banks are finally beginning to report loan growth in recent quarters, affirming trends in the FEDs Senior Loan Officer survey which show Commercial & Residential Real Estate loan demand improving and credit standards across commercial and consumer loan categories continuing to ease. We expect positive demand trends to continue alongside ongoing labor market & private sector balance sheet improvement with further easing in standards following pro-cyclically in the wake of improving credit risk and rising demand.

Household net wealth is making new nominal highs alongside housing and financial asset re-flation while Household debt service ratio’s remain at trough levels and total household debt/GDP continues to decline. We remain in a debt sweet spot of sorts for households with the potential for the flow of net new credit to support consumption while debt ratio’s continue to decline concurrently.

DEFICIT SPENDING: The Federal budget deficit has been in retreat as growth/tax receipts have exceeded initial forecasts while stabilizer payments have declined and other one-times (Fannie/Freddie payments to treasury, HARP payments to treasury, GM Sales, etc) have supported treasury inflows. Congressional Debt and Budget talks have (thankfully) been almost non-existent this year as the upside surprise in deficit spending allowed the party’s to remain on mute and/or focus energies elsewhere.

As a reminder, the official suspension of the Debt Ceiling brokered alongside the Fiscal cliff resolution lasted until 5/19/13 with the Treasury currently employing ‘extraordinary measures’ to keep things going. The partisan rhetoric has begun to bubble in the last couple weeks and we expect the Budget and Debt Ceiling acrimony to pick up in earnest in August alongside budget talks. The treasuries ability to keep things going is currently expected to last, at least, until September and as late as November. The treasury will announce its quarterly refunding plans for government operations on Wednesday (7/31).

CONSUMPTION: We’ve seen a strong 3 quarter acceleration in consumer spending through 1Q13 – a streak that will likely end with reported 2Q13 GDP as personal income and spending growth was constrained by a rising saving’s rate, muted wage inflation and negative tax law impacts. Upside in disposable personal income will probably remained constrained over the balance of the fiscal year as ~2% of the workforce sees ~7% reduction in income alongside federal government furloughs and ongoing layoffs.

We would note that retail sales and durable goods (auto’s) have been decent despite the consumption headwinds. Indeed, the realities of the existent fiscal policy drags (sequestration, tax increases, etc) and the fact that the economy is not in full escape velocity mode are well advertised if not fully understood.

Further, the seasonality in the reported data, which is currently a headwind, will reverse come September. So, optically, seasonality will amplify any ongoing, organic improvement in the labor market and broader domestic macro data just as panglossian storytelling about a diminishing fiscal drag and easier comps as we annualize the tax and sequester events will begin to hold greater appeal.

Outside of Financials, 2Q13 earnings haven’t been particuIarly great but that’s not a new phenomenon and valuation-in-isolation is still not a catalyst. Does a multiple turn (or three) matter in the short/intermediate term in an the era of global capital market liberalization and integration, accelerating capital mobility, and a global over-allocation to debt that is facing a negative inflection?

Can expensive get modestly more expensive and cheap cheaper when asset class optionality (you don’t want to be long Commodities, Emerging Markets (Debt, equity, currencies), Yen’s, or most of Europe) continues to contract?

We think so – particularly if the dollar can continue to strengthen, investor's get increasingly comfortable with the implications of #RatesRising and real yields on domestic assets continue to increase.

Big Data week this week. Pay attention to the trees, but don’t get so close to the bark that your returns get enucleated. Keep mind of the forest – at present, the Trend is still your friend.

Christian B. Drake

Senior Analyst