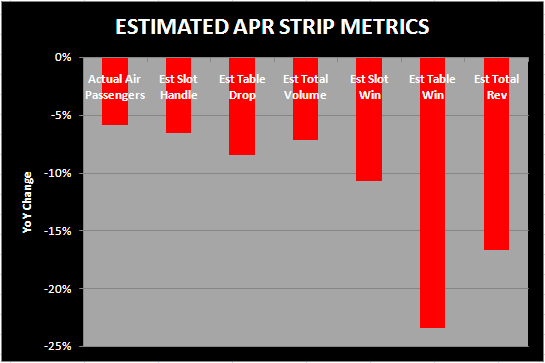

McCarran Airport posted its best month in almost a year with only a 5.9% drop from April of 2008. Combined with automobile traffic, the "strong" air visitation should translate into total visitation falling only around 4%. However, "lucky" play by the casinos last year causes a pretty difficult comparison. We estimate total Strip gaming revenues could fall by a rate in the mid-teens, with 9% of the drop caused by the high hold percentage last year. In April 2008, slot and table hold percentage was 30bps and 230bps above normal. The following table shows our projections for April 2009.

So while the airport data is somewhat encouraging, the actual revenue data will likely look weak. The good news is that the May hold comparisons are much easier. The Strip won't face a difficult hold comparison until September.