This note was originally published at 8am on July 12, 2013 for Hedgeye subscribers.

“Life is not easy for any of us. But what of that? We must have perseverance and above all confidence in ourselves. We must believe that we are gifted for something and that this thing must be attained.”

-Marie Curie

For those that haven’t been following the news reports from Alberta over the past month, the province and in particular its largest city Calgary, have been devastated by floods. I’ve been up in Calgary, Alberta over the last couple of days meeting with clients and companies and the perseverance to rebuild and recover has been nothing short of amazing.

The most significant tourist and cultural event in Calgary every year is the Calgary Stampede. It is a combination of an outdoor fair and championship rodeo, and attracts many hundreds of thousands of visitors. Fittingly, the slogan of this year’s Stampede is “Come Hell or High Water”, which is an acknowledgement to what the city has gone through to begin the recovery from devastating flooding.

Once a century floods are what we in the risk management business call tail risk events. They are low probability events that occur rarely but have an outsized relative impact. The reality of tail risks, or black swans as Nassim Taleb calls them, is that they actually occur much more often than normally distributed risk model would project.

Back to the Global Macro grind . . .

Yesterday we hosted a call with George Friedman, the CEO and founder of Stratfor, a veritable private CIA. With an army of global contacts and human intelligence collectors, they are rightfully considered among the best and most accurate assessors of global geo-political risks. As a result, their clients include major government organizations, corporations and global asset allocators.

One of the key ideas that Friedman raised on his call was that despite the recent complacency in European equity and debt markets, things may not end well in Europe. From his perspective, which we would agree with, the key political issue in Europe is that the grand experiment of the Euro has really only benefitted Germany. The value of the Euro has supported the 40%+ of exports that drive German GDP, but has failed the rest of Europe. Friedman thinks we may be in the early days of mass popular unrest in Europe across economically disadvantaged European nations outside of Germany.

Next week we will be releasing our quarterly themes, which is how we quantify the most important factors that are, and will be, driving markets and asset returns over the next couple of quarters. Our Q2 themes were growth accelerating, strong dollar, and emerging outflows. These largely played out in spades, particularly emerging market outflows, the extent of which surprised many market participants in Q2. We added the etf EEM, which is a proxy for the emerging markets equities, as a short idea to our Best Ideas product on April 23rd. Since then the EEM is down more than 10%.

On Monday at 1pm eastern we will be hosting our Q3 Themes call, and while I don’t want to want to steal all of the thunder of that call, our Q3 Themes are as follows:

1. #DebtDeflation – This theme analyzes the massive build up of debt globally and then looks at debt by sector to assess the outlook over the coming months. Broadly speaking, you don’t want to be long bonds in the TREND duration. Even if gentlemen prefer bonds, we don’t.

2. #AsianContagion – Our Senior Asia Analyst Darius “Sunny D” Dale has done an outstanding job parsing through the Asian economies over the last eighteen months. This theme primarily looks at the intermediate impact of Japan and China across Asian economies more broadly. By and large, as Chinese economic growth goes, so goes growth across Asia.

3. #RatesRising – This theme has been and will likely continue to have the most meaningful impact on U.S. markets as we’ve seen over the past six weeks with rates breaking out to the upside and devastating the bond markets.

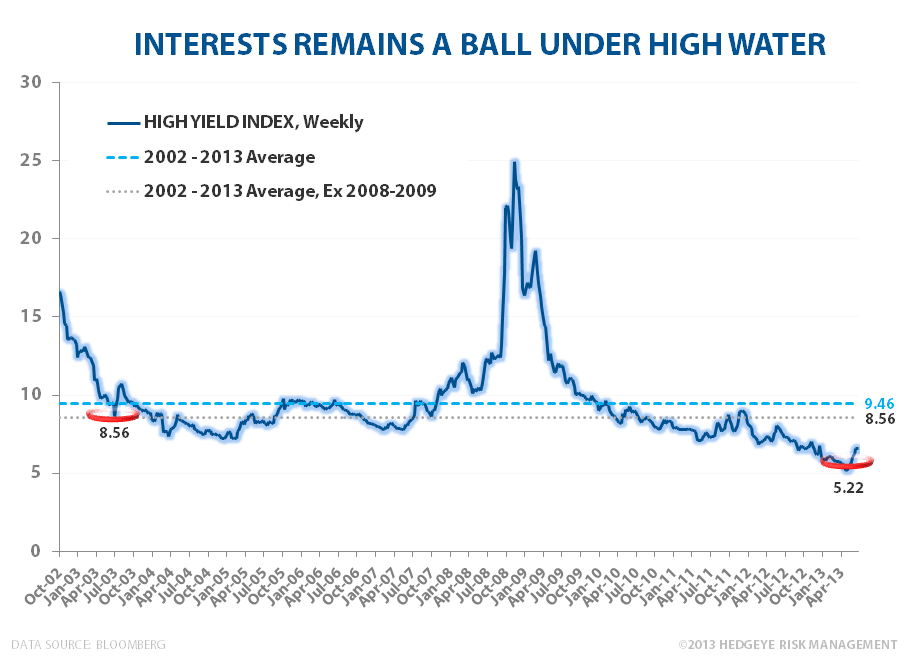

In the Chart of the Day, we’ve borrowed a chart from the Q3 Themes presentation of the high yield index and the potential impact of a reversion to the mean in bonds. As the chart shows, high yield is well below its 10-year average yield of 9.6%. Even if we exclude the anomalous period of 2008 – 2009, in which rates spiked, that average is at 8.6% and well above current levels.

Our research shows that rates reverting to more normal levels won’t actually impede growth, and thus equity market returns. In fact, the best U.S. economic growth rates often occur when the 10-year yield is in the 4 – 6% range. The bond and gold markets, of course, fare much, much worse in a rising rate environment.

In particular, gold has surprised people to the downside this year. Many gold bugs have argued to us that with the recent correction in gold, now is no time to sell. In reality, the facts tell a different story. Gold will continue to underperform in an environment of rising rates and a strong dollar.

Our correlation analysis tells us that the other key factor driving gold is the size of the Federal Reserve balance sheet. In fact, the correlation is over 0.90 on an r-squared basis (so very high). To the extent that the rate of change in the Federal Reserve balance slows, or god forbid declines, it could well be the death knell for gold and gold bugs.

We hope you can join us for our theme call on Monday.

Our immediate-term Risk Ranges are now as follows:

UST 10yr 2.42-2.77%

SPX 1634-1681

VIX 13.15-15.92

USD 82.52-83.93

Oil 105.84-110.73

Gold 1210-1312

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research