Hershey’s Q2 performance shows it is running on all cylinders. HSY is lapping 2012, a year in which it took price to offset inflated input costs; it’s now seeing significant volume gains, up +6.6% versus the prior-year quarter, lower input costs, and solid market share gains in the U.S. in every channel that it competes in (including mints and gums that are typically weak). We expect this strong momentum to continue in 2H, especially given the strong merchandizing around Halloween and the holidays.

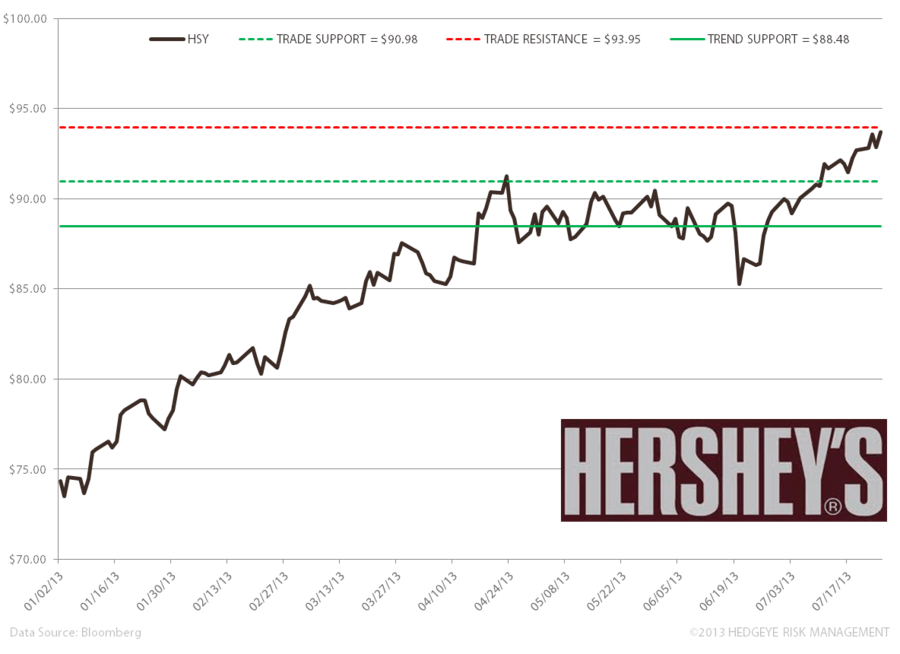

Our quantitative set-up shows HSY trading near its immediate term TRADE resistance level of $93.95. We’re waiting and watching to see if it can break through this level; if it can we like that it’s firmly anchored by its support lines (the two green lines), over the TRADE and TREND durations.

What we liked:

- Q2 EPS beat consensus ($0.72 vs $0.71), up 9.1% versus the prior-year quarter

- Revenue in line with consensus at $1.51B, or 6.7% versus the prior-year quarter

- Volume rose 6.6% (including 1% from Brookside and +0.1 FX benefit)

- GM up 290bps in the quarter on lower commodity costs, profitable sales mix, and cost savings

- Input cost deflation of $29MM was better than original estimates

- Momentum in U.S. and key international markets

- In the US, with the exception of gum, sales increased at the high end of the historical growth rate

- Gained market share in the U.S. in every channel that it competes in., and overall took a 1.3% market share gain in chocolate

- Strong performance from Brookside and expected to contribute 1pt of growth in 2013

- International - China, Mexico, and Brazil solid performance

- International sales (excluding Canada) up 8% in the quarter. Expects international to accelerate over 2H and FY sales up 15-20%

- Q2 interest expense of $21.1MM, declined vs $24.3MM last year

- In 2013 expects interest expense to be $90-95MM and FY adjusted tax rate to be the same as last year [35.7% tax rate in Q2 (in-line with expectations) vs 32% last year]

- Expects FY advertising up 20%. Specifically for International, advertising up 45-50%

Guidance FY: Net Sales up 7% (including the impact of FX); EPS $3.68-3.71 (up 14% year-over-year vs previous 12% guidance); GM up 220-230bps (vs prior estimate of 190-210bps, due to improved sales mix and higher productivity, and sees no change due to input cost inflation).

Matthew Hedrick

Senior Analyst