Summary

CAT reported a disappointing quarter and again lowered guidance. Earnings summaries abound and we’ll keep our comments to just three key topics:

- CAT On the Roof: Guidance is still too high for 2013 and management is still letting us down easy.

- Backlog Decline Matters, Too: The drop in backlog more than offset the 2Q dealer inventory liquidation excuse. When dealer inventories and backlog changes are stripped out, there is nothing particularly interesting about 2Q revenue (i.e. it reflects underlying demand).

- Pricing Down: CAT has often cited 2009 pricing strength as a reason not to worry about Resource Industries. Pricing was down in 2Q and the incremental mining capex declines in 2014 are likely to accelerate pricing pressure. We see risks to oil & gas capital spending in Power Systems, where pricing held in 2Q.

If you are interested in other items, like the growth in receivables with reserve release, lack of transparency, or the impairment charges/restructuring that we expect to be announced in the next month or so, feel free to ping us. We have been negative on CAT for over a year and our thesis appears to be playing out well.

They Can’t Do $6.50, Either: To hit guidance, CAT’s margins in 2H would need to improve ~30% vs. 1H with NEGATIVE MIX and NEGATIVE PRICING in Construction Industries and Resource Industries. Sure, that might happen – and 795F Trucks might fly. As we have written repeatedly – CAT is letting us down easy (gradually) and we have a tough time getting to $6.00 in 2013 EPS. This is just a rough sketch of guidance - not what we expect, which we published here:

Guidance also excludes whatever charges the company takes when it announces further cost reductions in the next month or so. On the topic of a potential BUCY impairment, Bradley Halverson stated “we certainly wouldn’t be using a cyclical low straight-line going forward,” which we assume was meant to imply that these 2Q results are cyclical low results. That is odd, because the survey CAT referenced suggested that mining capex is not at a cyclical low – it is going 20% lower next year. Expect impairment charges in coming quarters. (We would bet that a BUCY impairment charge comes with a CEO severance charge, too.)

We factor in share repurchases in the table above. However, on the call management said that “Repurchasing stock in a downturn has been a key part of our cash deployment strategy.” As we will see discuss below, there hasn’t been much of a downturn yet. They have been repurchasing cyclically inflated shares, in our view.

Backlogs vs. Dealer Inventories – This Is Normal: CAT said revenues in the quarter were negatively impacted vs. “end-user demand” by the decline in dealer inventories. We are all supposed to back that out and expect an acceleration as soon as dealer destocking is finished. However, revenues were puffed-up vs. “end-user demand” by the decline in backlog (i.e. revenues recognized in this quarter from end-user demand in prior periods). Management doesn’t mention the draw on backlogs, but it undermines the dealer inventory drawdown excuse for the 2Q 2013 miss.

When adjusted for both the change in dealer inventories and the draw on backlog, 2Q results do not look nearly as weak. They actually look fairly normal – even sequentially better. We think this is a better metric for evaluating normalized results. Second quarter results are not depressed so much as prior results were inflated. With most of the mining down-cycle still ahead, 2Q results do not appear to be abnormally low, with a spring back just around the corner.

Importantly, the favorable back half guidance does not mark the bottom – it marks another pending guidance cut, as previously noted. To hit the current revenue guidance, management will need to draw heavily on its order backlog (the effect of which we left at zero in the table). CAT would need to draw backlog down by $1-$1.5 billion in each of the next two quarters to have a shot at hitting the new revenue guidance, in our view. Leaving 2013 with a drained backlog would likely reset 2014 expectations much lower.

Some Additional Notes on Dealer Inventory Excuse:

- First, 2013 is not a bad year for the mining industry – that is delusional. 2002 probably was, when many mining companies were suffering heavy losses. Mining can get really ugly.

- Second, one should ask why management allowed dealers to get stuffed with customized mining inventory and why they aren’t being more transparent on cancellations (A $19.3 billion order backlog and excess CAT inventory is an oddly tough position to get into).

- Third, the comparison of dealer deliveries to end-user demand is misleading, in our view. Comments in the release like “would have needed to increase more than 50 percent to match what dealers were delivering to end users” mismatch the timing of that demand. Deliveries are a function of demand when orders were placed, which might be quite a long time ago. Aggregate dealer orders would be useful, but those are not provided.

- Finally, from what we can see of dealer inventories (Finning, Toromont, other public dealers) they don’t look low at all. We’ll see where they come out at 2Q end.

Pricing Down

Resource Industry Pricing Weakness: A major leg of the “don’t worry, be happy” view of Resource Industries is that pricing actually increased slightly in the 2009 downturn. It may have only been a ~1% decline in 2Q, but it is something they implied would not happen. This industry has too much capacity and we believe that pricing will get much worse as volumes drop into 2014. It is hard to model stable margins with price declines, excess inventory and overcapacity (and a lack of disclosure on aftermarket vs. new equipment).

On Mining Equipment - “Yes, I mean, if I go back to the end of the first quarter when we adjusted the guidance for the year, at that point in time, we talked about the price realization for the year being positive about 1%. That's not much of a change from what we were thinking from January. It's been tight, but the idea that there is giant discounting or something like that going on is just not the case. Even in 2009 we had a 3% price increase. I mean, so it's not as sensitive, I think, as most people think either going up or going down.” - Michael DeWalt 6/5/2013 i.e. recently

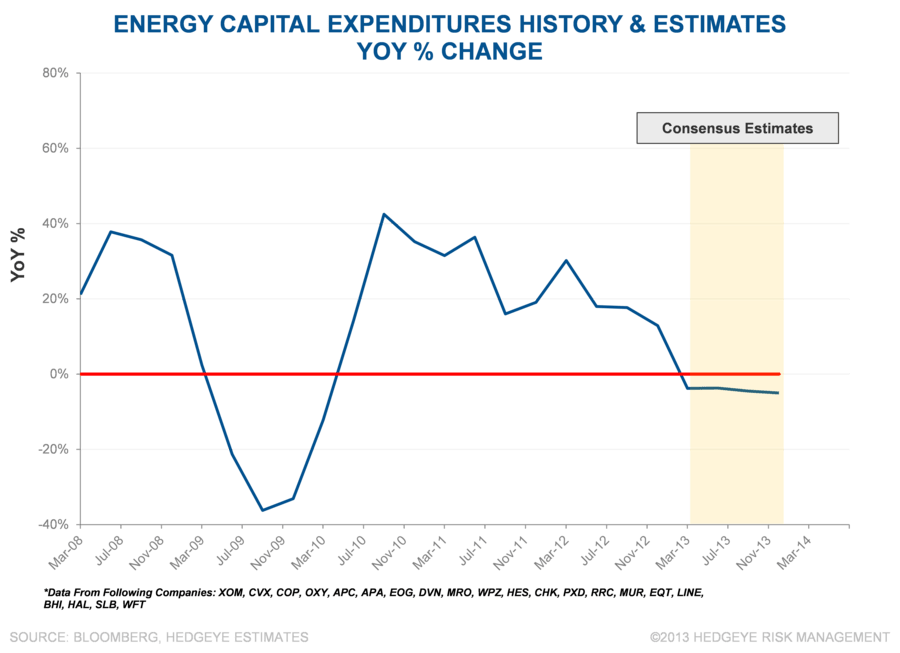

Power Systems Next? Oil & gas capital spending should follow a similar pattern as mining’s if oil & gas prices remain stagnant.

Conclusion: The decline in resources-related capital spending is a multi-year return to normal levels, not a decline from them. CAT finally acknowledged that mining capex (a portion of resources-related capital spending) isn’t rebounding in 2014. We don’t think it rebounds for – well- decades. We also think that oil & gas related capital spending could be the next shoe to drop for CAT.