Slack Sails

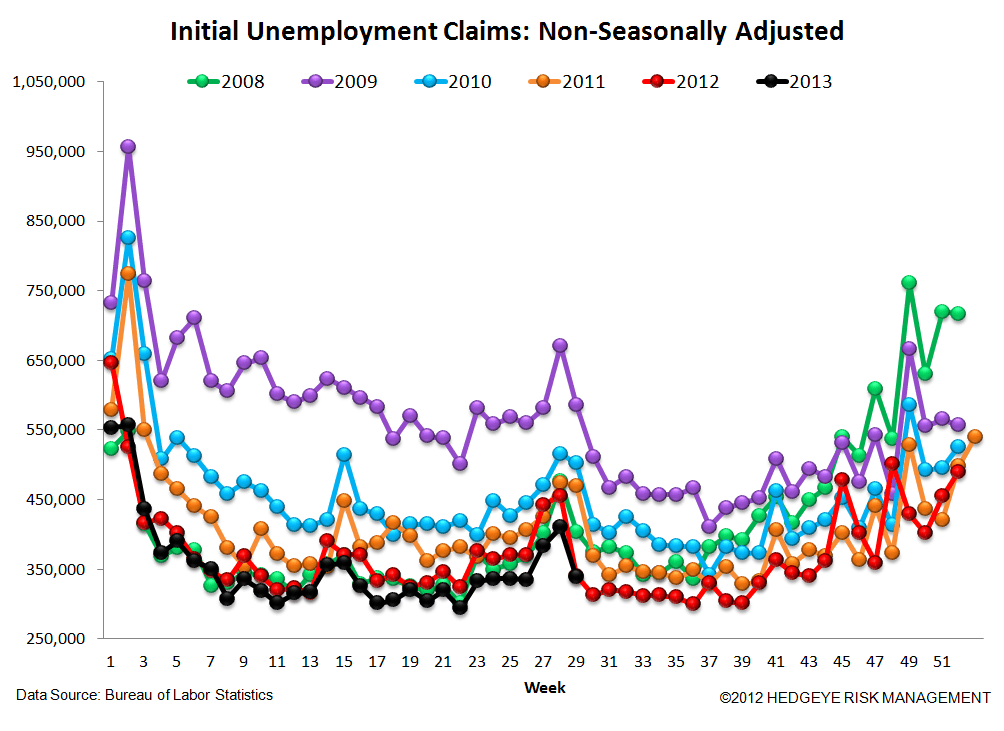

This past week, rolling NSA initial claims were 8.8% lower than the prior year. This marks a decelerating rate of improvement vs the prior week, when rolling NSA claims were better by 10.6%. On a single week basis, NSA claims were 0.8% lower than the previous year, a sharp deceleration vs the prior 9 prints of: -9.9%, -13.3%, -9.4%, -9.2%, -7.7%, -11.7%, -9.4%, -7.6% and -8.0%.

A possible explanation is that we're eclipsing the auto plant closings, which create significant NSA volatility. Recall that this year, due to heavy demand, there were far fewer auto plant shutdowns than in the corresponding periods last year. That said, the auto dynamic is a two-week phenonemon, so it wouldn't explain the deviation from the trend we've been seeing the last 9 weeks.

Bear in mind that in less than six weeks we'll shift out of the seasonally-adjusted data headwind period into the data tailwind period, which will last six months from September through February, 2014.

The Data

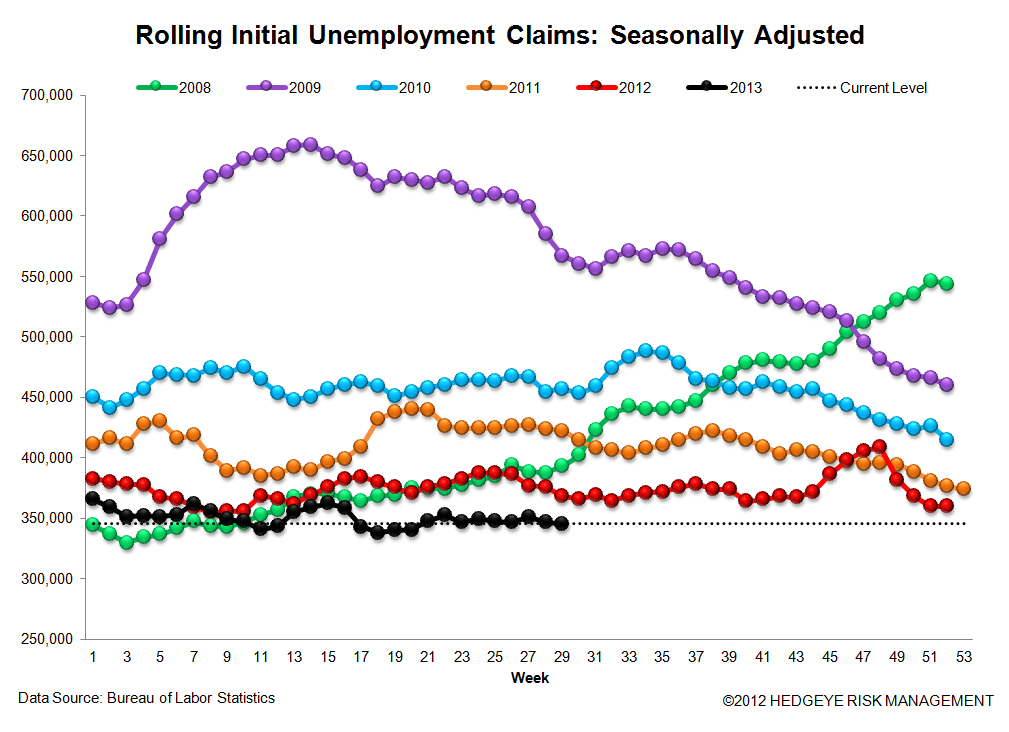

Prior to revision, initial jobless claims rose 9k to 343k from 334k WoW, as the prior week's number was revised up by 2k to 336k.

The headline (unrevised) number shows claims were higher by 7k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -1.25k WoW to 345.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -8.8% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -10.6%

Yield Spreads

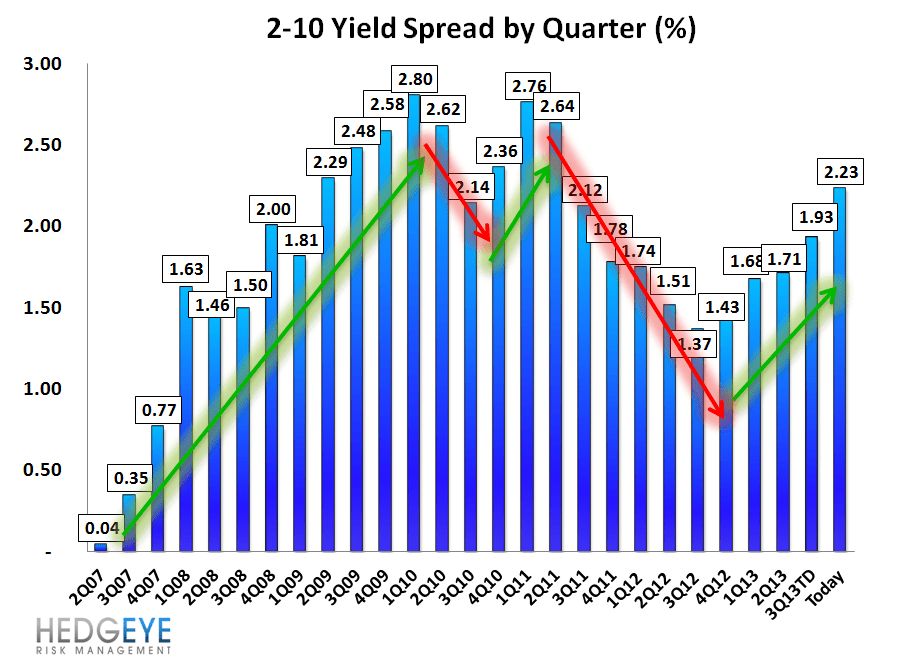

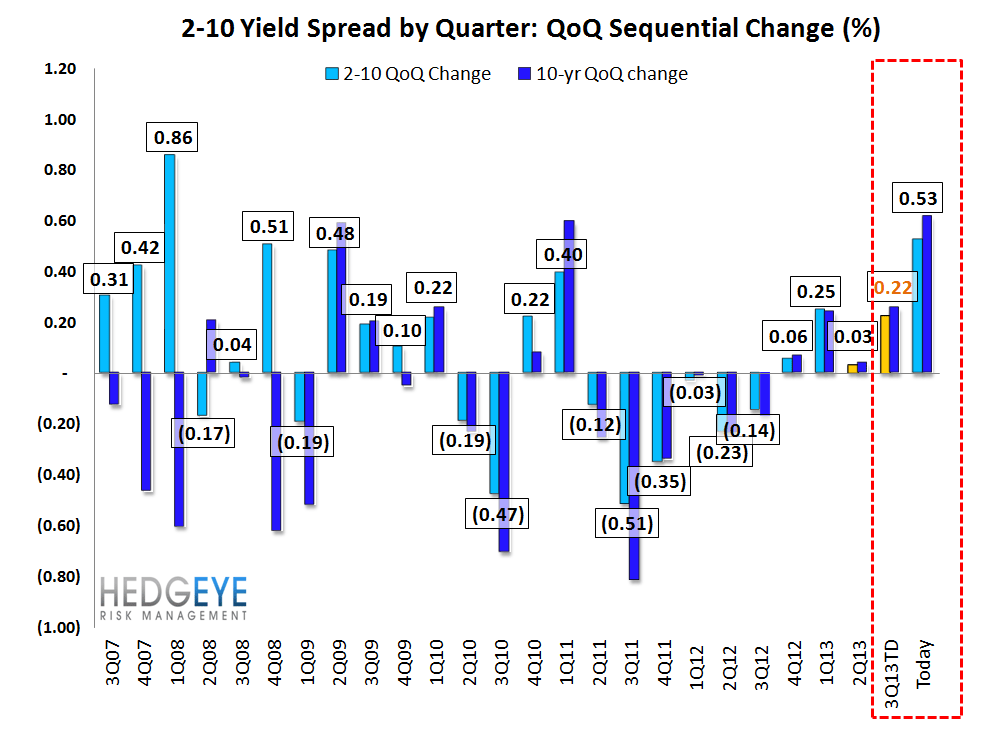

The 2-10 spread rose 4 basis points WoW to 223 bps. 3Q13TD, the 2-10 spread is averaging 193 bps, which is higher by 22 bps relative to 2Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT