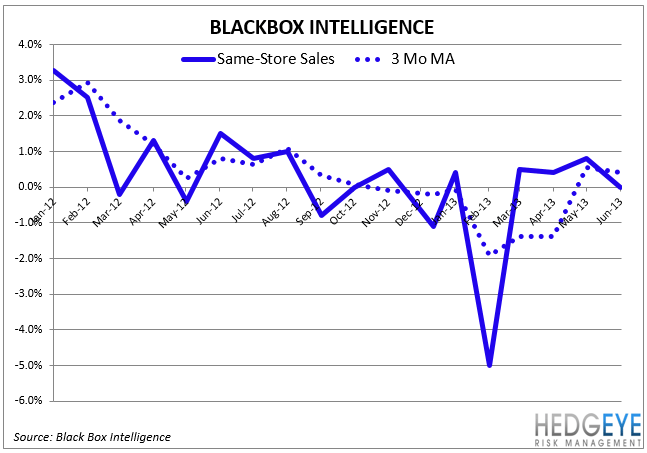

We suspect that many casual dining stocks will face a long, hot summer.

While we reported on the tough June sales numbers in our “Casual Dining Double Dip” note two weeks ago, the results from both CAKE and PNRA are adding some perspective around the reality that the casual dining space is in a tough spot.

RRGB – Remains on the Hedgeye Best Ideas list as a SHORT.

The notion that RRGB is going to significantly outpace the rest of the casual dining space and show a significant improvement in traffic seems far-fetched. RRGB is accelerating spending on programs that we believe will not drive the desired traffic and will ultimately result in an earnings shortfall.

While our original thesis suggested that the big miss could come in 3Q13, the current industry trends suggest that 2Q13 will likely come in short of expectations. At the very least, we foresee guidance for the balance of 2013 being reduced.

EAT – Chili’s is not immune to the industry slowdown.

Similar to RRGB, we suspect that EAT will also fall victim to a subpar summer. We like the long-term vision that EAT’s management team laid out at a recent analyst meeting, but…

Unfortunately, over the intermediate-term TREND, the company faces numerous issues. Chili’s is not only part of an industry that is in secular decline, but its largest competitor (DRI) is desperate for increased traffic and will use discounting as its weapon of choice.

It is difficult for us to see how EAT will be able to report numbers that the street will be happy with. We will be publishing an earnings preview on EAT to further outline what we believe the recent quarter may look like.

Other names in the basket of shorts should include TXRH, DRI, and BLMN.

Howard Penney

Managing Director