This note was originally published July 11, 2013 at 14:51 in Restaurants

Conclusion

Despite the significant volatility the company has faced since December 2012, YUM’s long-term growth story remains intact. Yesterday’s earnings release suggests that the fallout from the chicken supply scandal and Avian flu issues are abating.

Though we will wait for further confirmation on the near-term duration, we remain confident that the long-term upside for YUM shares represents an attractive opportunity for investors willing to look past the near-term issues. The talk of the earnings call today quickly transitioned away from the poor results in China and toward the timing of the expected recovery in sales and margins.

2Q13 Recap

The stock traded sideways as expected. YUM reported 2Q13 EPS of $0.56 (-16% YoY) vs. Street consensus of $0.54. During the second quarter, YUM demonstrated impressive COGS and labor controls. The company maintained its guidance for the balance of 2013, including a 4Q turnaround in China same-store sales trends and a mid-single digit decline in 2013 EPS. Importantly, trends in China continue to improve with June same-store sales down only 10% after coming in down 20% in May.

Other 2Q Highlights

- The effective tax rate, prior to one-time items, decreased from 23.9% to 22.1%. This decrease positively impacted EPS results by 2%.

- Same-store sales grew 1% at YRI and 1% in the U.S.

- Both YRI and the U.S. had 80bps of restaurant margin expansion.

- Operating profit declined 63% in China, while it increased 12% and 4% in the YRI and U.S. divisions, respectively.

- China restaurant level margins fell 500bps in the quarter to 10.6%.

- Total international development included 315 new restaurants, with 76% of this development occurring in emerging markets.

China

The largest short-term risk to the YUM story comes from the built in expectations that China will turn the corner in 4Q13. China’s June sales trend was only down 10%, indicating that sales are beginning to recover and moving in the direction of current expectations. With Pizza Hut’s June same-store sales coming in at 6%, it is clear that the brand continues to build momentum. Although the KFC numbers leave much to be desired, the comps appear to have bottomed out earlier this quarter. Same-store sales have improved over the course of the quarter, moving from down 26% in April to down 13% in June. We believe that China is on track for flat to positive same-store sales trends coming out of 3Q13 and positive trends early in 4Q13.

Rest of the World

The YRI and U.S. segments of the business continue to be solid performers and contribute to YUM’s growth profile.

YUM’s YRI Division reported 1% same-store sales growth, led by 5% same-store sales growth in emerging markets. This performance was somewhat offset by weakness in the developed regions where same-store sales fell 1%.

- Emerging markets system sales grew 12%, driven by 8% unit growth and 5% same-store sales growth.

- Developed markets system sales grew 1%, driven by 1% unit growth; this number was partially offset by a 1% decline in same-store sales due to weakness in Japan and the UK.

- Restaurant margin increased 0.8% and operating profit grew 12% in the region.

- YRI is on track for a record amount of openings this year and continues to benefit from recent asset sales.

- Opened 205 new units in 50 countries, including 129 new units in emerging markets.

YUM’s U.S. Division reported 1% same-store sales growth, led by 2% and 3% same-store sales growth at Taco Bell and KFC, respectively. Taco Bell continues to be one of the strongest brands in the QSR segment. The brand was able to increase same-store sales despite facing a 13% comparison from last year. Same-store sales fell 2% at Pizza Hut in the second quarter.

- USA same-store sales increased 1%.

- Taco Bell same-store sales increased 2%.

- KFC same-store sales increased 3%.

- Pizza Hut same-store sales decreased 2%.

- Restaurant Margin improved 0.8%.

- Operating profit increased 4%.

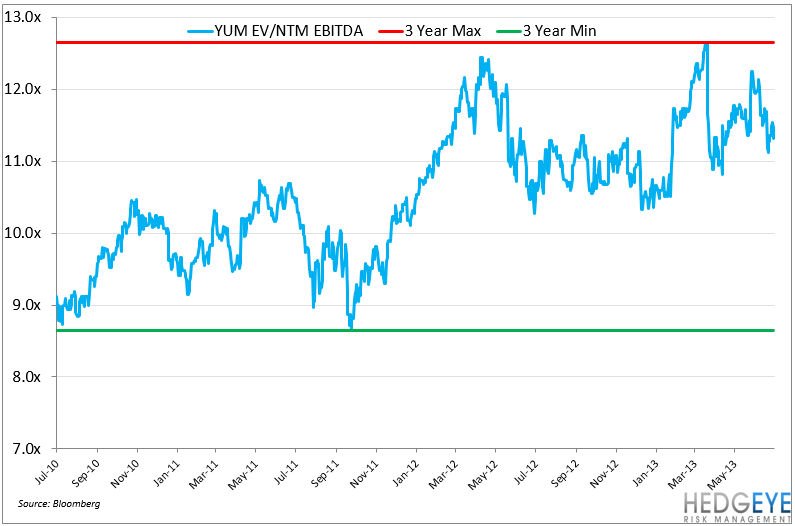

Valuation

Similar to the rest of the restaurant industry, YUM’s valuation appears stretched. We intend to issue a report card on YUM’s road to recovery as the company continues to report monthly same-store sales trends in China. YUM’s long-term development plans in China remain intact, particularly as the company begins to focus on establishing Pizza Hut locations in lower tier cities. We believe that the Street will soon shift its focus away from the recent negative results in China and will begin to focus on 2014 and the timing of a margin recovery.

Howard Penney

Managing Director