PNRA remains on the Hedgeye best ideas list as a SHORT.

Overview

PNRA has now missed expectations for the second straight quarter.

In 2Q13 PNRA reported 16% EPS growth on 11% sales growth, which missed consensus by $0.03 and 2%, respectively. In addition, the 3.5% increase in same-store sales missed the consensus expectation of a 4.5% increase. Traffic trends declined 0.5% in 2Q, making it the third straight quarter of traffic declines.

Panera's Traffic Problem

As we mentioned in early April, PNRA’s position as a healthy QSR option that is relatively free of competitors is gradually changing. An increased number of casual dining chains are now offering lower price points and other QSR chains are upgrading their menus. These menu upgrades include items that are marketed competitively as healthy eating options and are cheaper than PNRA’s core offerings. As a consequence, this secular trend is manifesting itself in the components of comparable sales growth as PNRA traffic trends have shown weakness lately.

As the chart below illustrates, PNRA’s traffic trends have been declining for the past three quarters. In 1Q13, management attempted to attribute the decline in traffic to poor weather. Given the current trends and the lowered sales outlook for the balance of the year, our short thesis appears to be playing out well.

In today’s press release, management offered up the following initiatives to help solve the company’s current issues:

“We now believe that to consistently operate at the very high sales volumes we are generating and to prepare for additional sales from our initiatives to expand access to Panera and utilize marketing, we must improve our peak hour throughput. While results in the next few quarters may be choppy as we invest in both sales-building initiatives and operational capabilities, we believe that our efforts will ultimately enable us to deliver an enhanced customer experience, grow sales and expand earnings.”

While management does not share our view on the competition, we also believe that some of the issues the company faces are self-inflicted.

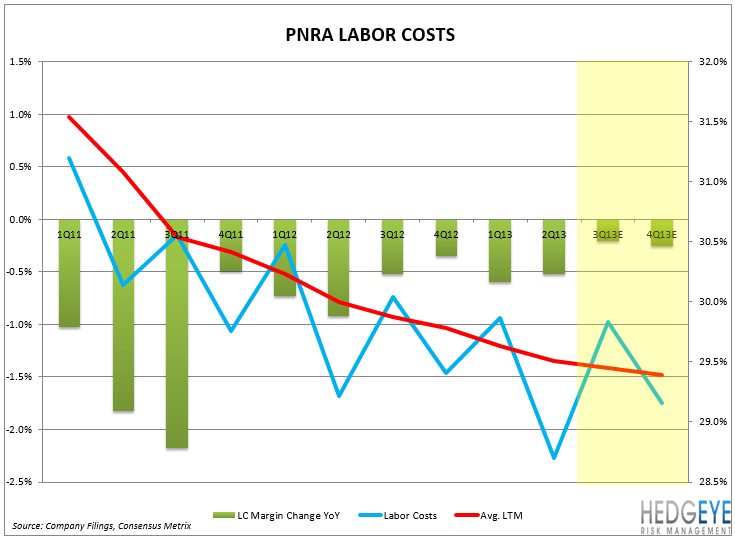

Labor Cost Trends

Shown in the chart below, PNRA has seen a year-over-year decline in labor costs for 12 of the last 13 quarters. This is a trend that is unsustainable and will likely lead to customer service related issues in the future. We believe that this trend will need to be reversed in order to fix any peak hour throughput issues.

The company is hosting its earnings call tomorrow morning at 8:30am ET. We’ll post on anything incremental after the call.

Howard Penney

Managing Director